Photoelectric Sensors Market Size 2025-2029

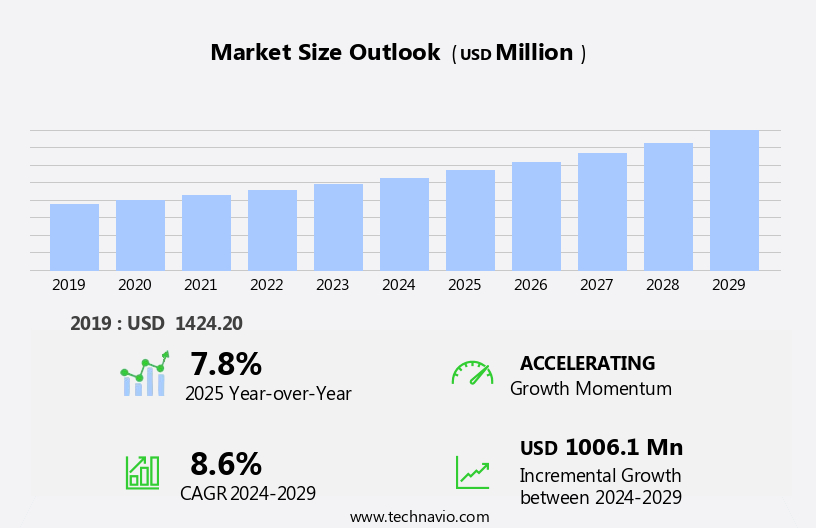

The photoelectric sensors market size is forecast to increase by USD 1.01 billion, at a CAGR of 8.6% between 2024 and 2029.

- The market is witnessing significant growth, driven by the increasing adoption of Industry 4.0 practices and automation across various industries. This trend is leading to an escalating demand for advanced sensor technologies, including photoelectric sensors, to optimize manufacturing processes and enhance production efficiency. Another key driver is the integration of Light Detection and Ranging (LiDAR) technology within photoelectric sensors, enabling them to offer superior sensing capabilities and versatility. However, cost constraints remain a significant challenge for the market, as advanced photoelectric sensor technologies can be expensive.

- Companies must address these challenges by focusing on cost reduction strategies, such as optimizing production processes, improving efficiency, and exploring partnerships and collaborations to share development costs and risks. To capitalize on the market opportunities and navigate challenges effectively, businesses should stay informed of technological advancements, market trends, and customer needs, and invest in research and development to create innovative, cost-effective solutions.

What will be the Size of the Photoelectric Sensors Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market continues to evolve, driven by the diverse applications across various sectors. Proximity sensors, a key segment, find extensive use in process control, object detection, and presence detection. Fiber optic sensors and digital sensors cater to high-precision requirements, while long-range sensors enable speed measurement and machine vision applications. PLC integration and SCADA integration are crucial for industrial automation. Sensor calibration remains a critical aspect, ensuring sensor repeatability and accuracy. Ultrasonic sensors and laser sensors offer reliable level sensing, while sensor networks facilitate data processing and environmental monitoring. Motion detection is a growing application, particularly in building automation and quality control.

Innovations in sensor technology include smart sensors, which offer self-diagnostics and self-calibration. Sensor housings and sensor wiring solutions ensure durability and ease of installation. Signal conditioning and noise reduction are essential for maintaining signal integrity. Food & beverage processing relies on photoelectric sensors for various applications, from level sensing to presence detection. Infrared sensors and capacitive sensors are commonly used for food detection and temperature monitoring. Ethernet/IP and other communication protocols facilitate seamless integration into automation systems. The market's continuous dynamism is reflected in the ongoing development of advanced sensor technologies, such as high-speed sensors and sensor fusion, which combine data from multiple sensors to enhance performance.

Sensor maintenance and sensor cleaning are essential for ensuring sensor longevity and optimal functionality. Power supply solutions cater to the varying power requirements of different sensor types. In summary, the market is characterized by its continuous evolution, driven by the diverse applications across various sectors. The market's dynamism is reflected in the ongoing development of advanced sensor technologies, communication protocols, and integration solutions.

How is this Photoelectric Sensors Industry segmented?

The photoelectric sensors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

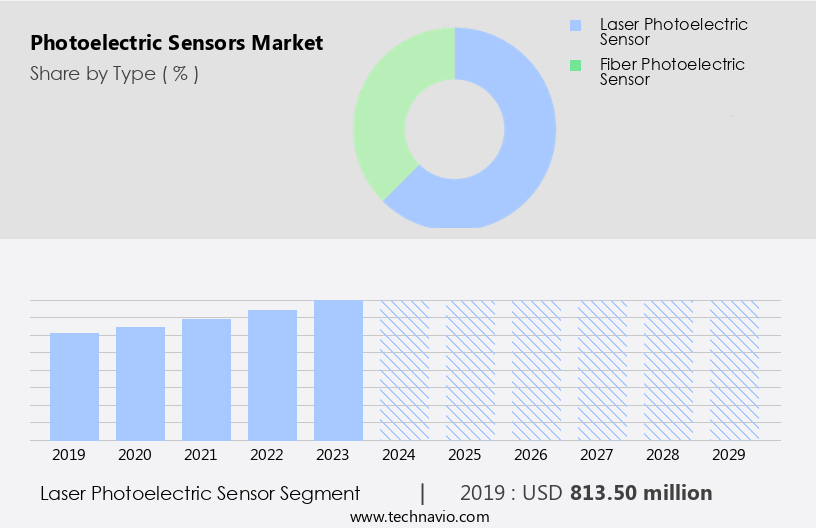

- Laser photoelectric sensor

- Fiber photoelectric sensor

- End-user

- Automotive

- Consumer electronics

- Building automation

- Others

- Product

- Retroreflective

- Diffuse

- Through-beam

- Application

- Object detection

- Positioning

- Safety and security

- Counting

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

The laser photoelectric sensor segment is estimated to witness significant growth during the forecast period.

The photoelectric sensor market encompasses various types of sensors, including ip67 rated, digital, fiber optic, long-range, and short-range sensors. These sensors cater to diverse applications such as presence detection, process control, object detection, position measurement, and quality control in industries like manufacturing, automation, and robotics. Laser photoelectric sensors, in particular, are gaining popularity due to their high precision and reliability. Utilizing laser technology, these sensors offer focused and constant beams for accurate detection and measurement. They are increasingly adopted for tasks requiring great efficiency and precision, such as identifying and positioning objects in manufacturing lines for seamless automation and quality control.

Other advanced features include EMI/RFI shielding, PLC integration, and SCADA integration. Environmental monitoring applications also benefit from photoelectric sensors' ability to detect motion, measure speed, and level sensing. Machine vision, data processing, and signal conditioning further enhance their functionality. Sensor networks, sensor calibration, and sensor maintenance ensure consistent performance and longevity. Food & beverage processing industries also leverage photoelectric sensors for their hygienic design and ease of cleaning. Power supply and sensor accuracy are essential considerations for optimal sensor performance. In conclusion, the photoelectric sensor market is evolving with advancements in technology, offering versatile solutions for various industries and applications.

The Laser photoelectric sensor segment was valued at USD 813.50 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

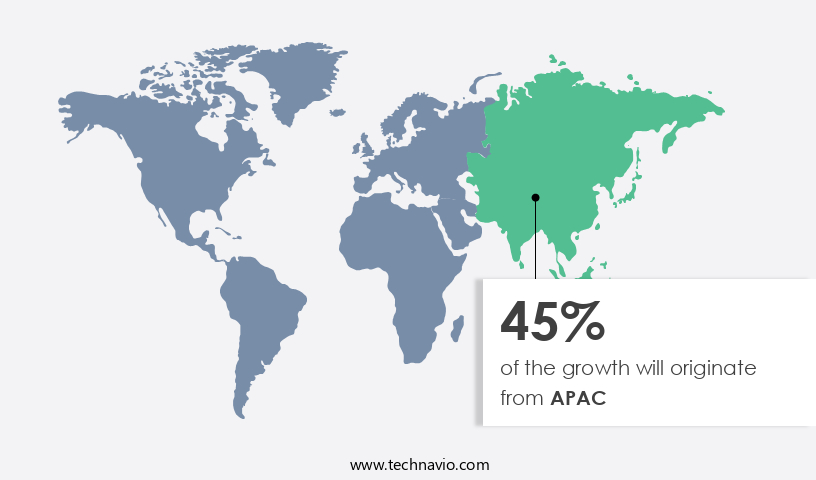

APAC is estimated to contribute 45% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in APAC is experiencing significant growth due to the increasing industrialization and automation in various sectors. The demand for smart manufacturing is driving the adoption of these sensors, particularly in industries such as automotive, electronics, and manufacturing. Severe industrial safety standards also necessitate the use of photoelectric sensors for process control, object detection, and quality control. In addition, the e-commerce sector's expansion and the need for efficient material handling in logistics and storage are increasing the demand for these sensors. Moreover, infrastructure construction and smart city projects are accelerating the use of photoelectric sensors in building automation applications.

These sensors come in various forms, including fiber optic, digital, long-range, and high-speed, catering to diverse industry requirements. They offer features such as EMI/RFI shielding, sensor linearity, digital output, and level sensing, among others. Photoelectric sensors are also integrated with technologies like machine vision, SCADA, and PLC for seamless data processing and industrial automation. The market is witnessing the emergence of advanced sensors, such as smart sensors, ultrasonic sensors, and sensor networks, which offer enhanced capabilities for environmental monitoring and motion detection. Sensor maintenance, cleaning, and calibration are crucial aspects of ensuring their longevity and accuracy. The market in APAC is poised for continued expansion, driven by the food & beverage industry's growing automation needs and the increasing focus on sensor resolution, repeatability, and lifespan.

Power supply and signal conditioning are essential considerations for optimizing sensor performance.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

In the dynamic and innovative technology landscape, the market continues to gain momentum, fueled by advancements in automation, industrial IoT, and machine vision applications. This market encompasses a diverse range of photoelectric sensors, including infrared, phototransistor, and CCD sensors, each offering unique advantages in terms of sensitivity, response time, and versatility. Integration with various communication protocols such as CAN, Ethernet, and Modbus, as well as rugged designs for harsh environments, further broadens their applicability. Key players in this market focus on R&D to deliver high-performance, cost-effective solutions for industries like automotive, manufacturing, and healthcare, ensuring continued growth and evolution.

What are the key market drivers leading to the rise in the adoption of Photoelectric Sensors Industry?

- The integration of Industry 4.0 practices and automation technologies is the primary catalyst fueling market growth.

- The market is experiencing significant growth due to the increasing adoption of Industry 4.0 and industrial automation. With the integration of digital technologies into manufacturing processes, there is a shift towards smart and networked industrial systems. Photoelectric sensors, which use light-based technology to detect the presence, absence, and distance of objects, are essential components in providing precise and efficient item detection in automated procedures. As enterprises embrace smart manufacturing processes, there is a growing demand for real-time data collection and precise control in automated systems. Photoelectric sensors offer signal isolation, SCADA integration, and digital output, making them ideal for level sensing applications in various industries.

- These sensors come in various types, including infrared, inductive, capacitive, and thru-beam, catering to diverse industrial needs. Moreover, advanced features such as noise reduction, Ethernet/IP connectivity, and high-precision capabilities enhance the functionality and reliability of photoelectric sensors. These sensors are widely used in various industries, including automotive, food and beverage, pharmaceuticals, and semiconductors, to ensure efficient and accurate production processes. Overall, the market for photoelectric sensors is expected to continue its growth trajectory due to the increasing demand for automation and smart manufacturing processes.

What are the market trends shaping the Photoelectric Sensors Industry?

- The integration of LiDAR technology into photoelectric sensors is an emerging market trend. LiDAR, or Light Detection and Ranging, enhances the capabilities of photoelectric sensors by adding distance measurement and 3D point cloud data acquisition. This fusion of technologies offers significant advantages in various industries, including autonomous vehicles, surveying, and industrial automation.

- The integration of LiDAR technology into photoelectric sensors represents a pivotal advancement in the global photoelectric sensor market. LiDAR sensors, which use laser beams to measure distances with high precision, enhance standard photoelectric sensors' capabilities for object detection and distance measurement. This technology generates precise 3D maps of the environment, enabling superior accuracy in detecting object shapes, sizes, and positions. In industrial automation, LiDAR-equipped photoelectric sensors optimize object detection and localization, leading to increased efficiency and safety. This trend is instrumental in the development of advanced driver-assistance systems (ADAS) and self-driving cars, where precise distance measurement is crucial for collision avoidance and navigation.

- Sensor calibration, sensor networks, sensor repeatability, sensor resolution, sensor lifespan, power supply, sensor accuracy, motion detection, and sensor wiring are essential factors influencing the market's growth. Ultrasonic sensors and laser sensors are other prominent technologies in the photoelectric sensor market, catering to various industries, including food & beverage.

What challenges does the Photoelectric Sensors Industry face during its growth?

- The implementation of advanced photoelectric sensor technologies in the industry faces significant cost constraints, posing a substantial challenge to growth.

- Photoelectric sensors play a significant role in various industries for presence detection, process control, object detection, speed measurement, position measurement, and quality control. Advanced photoelectric sensors, including IP67 rated, fiber optic, digital, long-range, and analog sensors, offer enhanced features and capabilities. However, the high cost of producing and developing these sensors poses a challenge to their widespread adoption, particularly in price-sensitive businesses. This cost barrier may hinder the adoption of advanced sensors in industries where cost efficiency is crucial, such as manufacturing, shipping, and consumer electronics. Companies in these industries may be reluctant to invest in these technologies despite their superior performance due to concerns about the return on investment and the potential impact on their overall cost structures.

- EMI/RFI shielding and short-range sensors are also essential considerations for specific applications. The market dynamics of photoelectric sensors necessitate a balance between cost and performance to cater to diverse industry requirements.

Exclusive Customer Landscape

The photoelectric sensors market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the photoelectric sensors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, photoelectric sensors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Autonics Corporation - Photoelectric sensors, including BUP series, BJX series, BRQ series, BJP series, BJR series, BTF series, BTS series, BJ series, BY series, and BYD series, are integral components of our advanced technology offerings. These sensors, known for their precision and reliability, enhance machine performance and efficiency. By utilizing cutting-edge photoelectric technology, we deliver superior solutions to various industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Autonics Corporation

- Balluff GmbH

- Banner Engineering Corp

- Baumer Group

- Carlo Gavazzi Holding AG

- Eaton Corporation PLC

- Hans Turck GmbH & Co. KG

- IFM Electronic GmbH

- Keyence Corporation

- Leuze Electronic GmbH + Co. KG

- Omron Corporation

- Panasonic Corporation

- Pepperl+Fuchs SE

- Rockwell Automation Inc.

- Schneider Electric SE

- SICK AG

- Takex Limited

- Telemecanique Sensors

- Wenglor Sensoric GmbH

- Yamatake Corporation

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Photoelectric Sensors Market

- In January 2024, Keyence Corporation, a leading manufacturer of industrial automation solutions, launched its new photoelectric sensor series, the BL Series, featuring advanced technologies such as high-speed response and high-sensitivity for various applications (Keyence Corporation Press Release).

- In March 2024, Sensirion AG, a Swiss sensor manufacturer, and ifm electronic GmbH, a German automation solutions provider, announced a strategic partnership to develop and market combined photoelectric sensor and condition monitoring systems for industrial applications (ifm electronic GmbH Press Release).

- In May 2024, OMRON Corporation, a global leader in industrial automation and sensing solutions, completed the acquisition of Adept Technology, Inc., a US-based provider of collaborative robots and autonomous mobile robots, expanding its robotics business and enhancing its photoelectric sensor offerings (OMRON Corporation Press Release).

- In April 2025, the European Union's REACH regulation introduced new guidelines for the classification, labeling, and safe use of photoelectric sensors and other industrial sensors, ensuring stricter compliance with environmental, health, and safety standards (European Chemicals Agency Press Release).

Research Analyst Overview

- The market is experiencing significant growth, driven by the integration of advanced technologies such as deep learning and machine learning for pattern recognition and image processing. Human-machine interfaces (HMI) are becoming more prevalent, enabling real-time monitoring and improved efficiency in various industries. Big data and data analytics are playing a crucial role in process optimization, leading to increased productivity and cost reduction. IoT integration and wireless communication enable remote monitoring and reduced downtime, while safety sensors ensure enhanced safety in manufacturing processes. Edge computing and cloud computing are transforming the industry by enabling real-time data processing and analysis, leading to improved quality and system integration.

- Three-dimensional vision and artificial intelligence are also gaining traction, offering new possibilities for automation and safety. Supply chain management is being revolutionized through the use of photoelectric sensors, leading to streamlined operations and optimized workflows. Overall, the market is witnessing a shift towards more intelligent, connected, and efficient solutions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Photoelectric Sensors Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

226 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.6% |

|

Market growth 2025-2029 |

USD 1006.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.8 |

|

Key countries |

US, China, Germany, Japan, UK, France, India, South Korea, Italy, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Photoelectric Sensors Market Research and Growth Report?

- CAGR of the Photoelectric Sensors industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the photoelectric sensors market growth of industry companies

We can help! Our analysts can customize this photoelectric sensors market research report to meet your requirements.

RIA -

RIA -