Pipeline Integrity Management Market Size 2026-2030

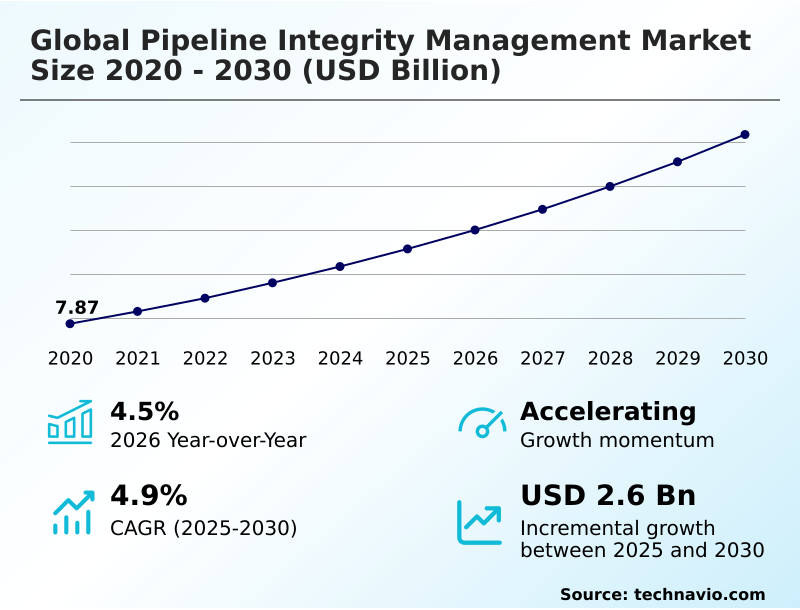

The pipeline integrity management market size is valued to increase by USD 2.60 billion, at a CAGR of 4.9% from 2025 to 2030. Stringent regulatory requirements associated with pipeline integrity management will drive the pipeline integrity management market.

Major Market Trends & Insights

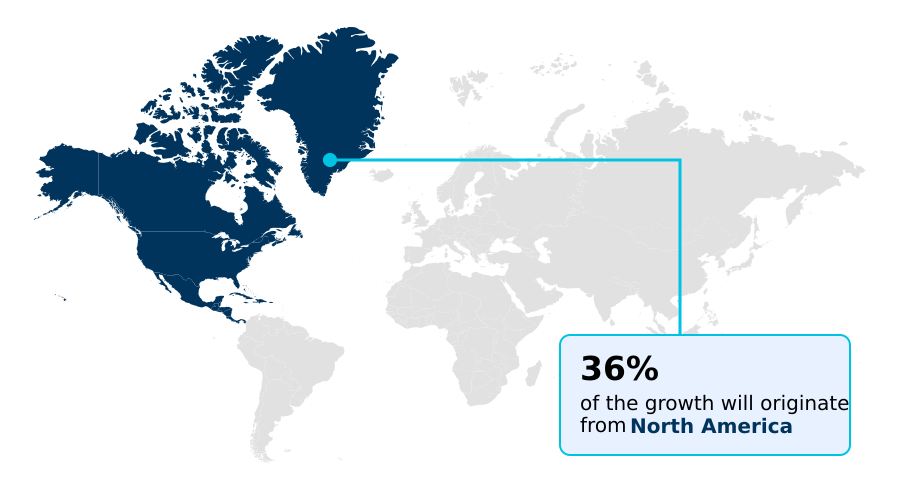

- North America dominated the market and accounted for a 35.8% growth during the forecast period.

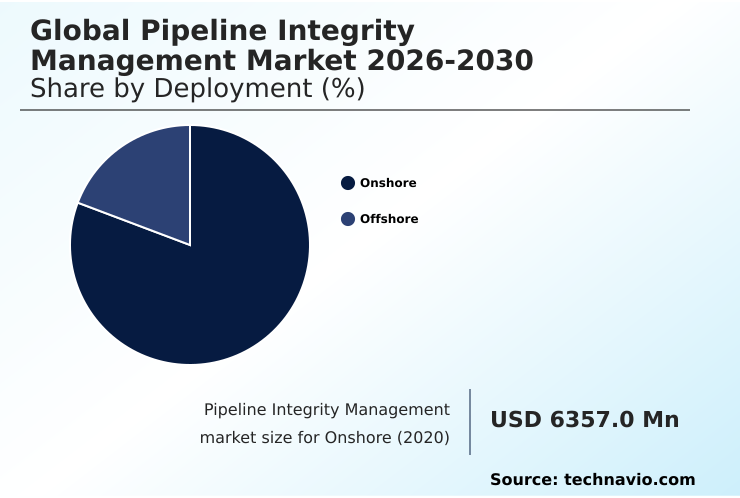

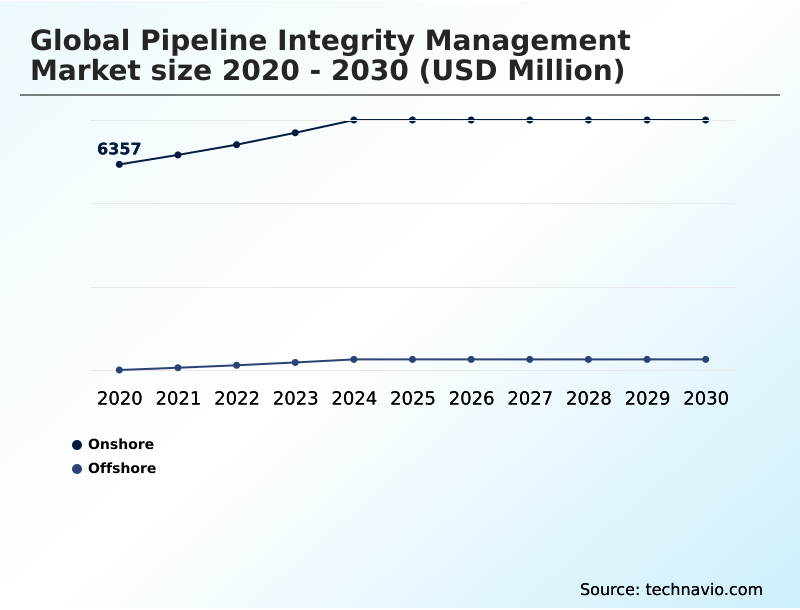

- By Deployment - Onshore segment was valued at in 2024

- By Service - Inspection service segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 4.30 billion

- Market Future Opportunities: USD 2.60 billion

- CAGR from 2025 to 2030 : 4.9%

Market Summary

- The pipeline integrity management market is fundamentally shaped by the need to ensure the safety and reliability of critical energy infrastructure. A primary driver is stringent regulatory compliance management, which compels operators to invest in advanced technologies for risk mitigation.

- Key trends revolve around digitalization, where digital twin technology and sophisticated pipeline data analytics are transforming reactive maintenance into proactive strategies. For instance, an operator of an aging network can leverage predictive maintenance models derived from ongoing corrosion monitoring and pipeline strain monitoring to optimize capital expenditure.

- By employing risk-based inspection (RBI), the firm can prioritize which segments require immediate intervention, such as hydrostatic testing or material property verification, thereby enhancing safety while managing costs effectively. However, the industry grapples with the persistent challenge of stress corrosion cracking (SCC) and the complexities of inspecting assets with unpiggable pipeline solutions.

- This dynamic landscape fosters continuous innovation in non-destructive testing (NDT) and leak detection systems to maintain operational resilience.

What will be the Size of the Pipeline Integrity Management Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Pipeline Integrity Management Market Segmented?

The pipeline integrity management industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- Onshore

- Offshore

- Service

- Inspection service

- Cleaning service

- Others

- Type

- Crude oil

- Natural gas

- Refined products

- LNG

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Deployment Insights

The onshore segment is estimated to witness significant growth during the forecast period.

The onshore segment of the pipeline integrity management market encompasses terrestrial networks where comprehensive asset integrity management is essential. Operators utilize techniques such as inline inspection (ILI) and cathodic protection systems to mitigate threats like corrosion and third-party damage.

The deployment of advanced non-destructive testing (NDT) has improved flaw detection rates by over 15% in onshore settings.

Continuous corrosion monitoring and routine pipeline pigging are standard, supported by ultrasonic testing (UT) and magnetic flux leakage (MFL) for precise defect characterization.

Innovations in smart pig technology and pipeline coating inspection are crucial for maintaining structural integrity and regulatory compliance across these extensive and accessible networks, which form the backbone of continental energy transport.

The Onshore segment was valued at in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Pipeline Integrity Management Market Demand is Rising in North America Get Free Sample

The geographic landscape of the pipeline integrity management market is diverse, with regional priorities shaped by infrastructure age, environmental conditions, and regulatory frameworks.

In North America, geohazard assessment for landslides and seismic activity is critical, accounting for over 15% of integrity budgets in certain high-risk corridors. Here, the integration of GIS for pipeline management is standard practice.

Across expansive territories in the Middle East and APAC, satellite-based pipeline surveillance provides cost-effective pipeline right-of-way monitoring, offering surveillance coverage for over 99% of remote routes.

In Europe's North Sea, subsea pipeline inspection robotics and advanced direct current voltage gradient (DCVG) surveys are essential for offshore assets.

Meanwhile, drone-based inspection is gaining traction globally for its ability to conduct rapid visual assessments and support hydrostatic testing logistics.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global pipeline integrity management market is evolving beyond conventional inspection to embrace a holistic, data-driven framework. A key focus is on managing aging pipeline infrastructure, where the cost of pipeline integrity failure necessitates proactive strategies. Operators are enhancing pipeline safety standards through rigorous pipeline integrity audit procedures and advanced risk assessment models for pipelines.

- For assets previously deemed hard to assess, new NDT methods for unpiggable pipelines are becoming critical. Technologies such as ultrasonic testing for pipeline welds and advanced pipeline crack detection technologies improve defect identification. Concurrently, the use of durable pipeline corrosion prevention coatings and addressing issues like hydrogen embrittlement in pipelines are vital for extending asset life.

- The integration of real-time pipeline monitoring solutions and satellite monitoring for pipeline threats helps in early threat identification and third-party damage risk mitigation.

- This digital transformation is powered by AI in pipeline anomaly detection and specialized software for pipeline integrity data, with the use of a digital twin for pipeline operations improving threat response times by more than double compared to traditional methods.

- Innovations in subsea pipeline inspection robotics and a focus on regulatory compliance for gas pipelines further define the sector's trajectory toward safer, more reliable energy transport.

What are the key market drivers leading to the rise in the adoption of Pipeline Integrity Management Industry?

- Stringent regulatory requirements associated with pipeline integrity management are a key driver for the market's growth.

- Stringent regulations and a heightened focus on safety are primary drivers compelling investment in advanced integrity solutions.

- The enforcement of rigorous regulatory compliance management frameworks, particularly for onshore pipeline safety, has led to a more than 25% increase in spending on certified leak detection systems in high-consequence areas.

- The adoption of a formal integrity management program (IMP) is now standard practice, with risk-based inspection (RBI) methodologies helping to decrease significant incidents by over 40% through targeted interventions.

- This proactive approach is central to effective asset integrity management and includes comprehensive environmental risk assessment and strategies for third-party damage prevention.

- Adherence to evolving pipeline safety standards not only ensures operational continuity but also reinforces public trust and environmental stewardship, solidifying compliance as a catalyst for technological innovation.

What are the market trends shaping the Pipeline Integrity Management Industry?

- The adoption of artificial intelligence and digital technologies is an emerging trend, reshaping pipeline integrity management by enhancing data analysis and predictive capabilities.

- Key market trends are centered on digitalization and automation, which are revolutionizing how pipeline operators manage assets. The implementation of digital twin technology allows for virtual simulations that have improved failure prediction accuracy by over 20%.

- Concurrently, the use of AI in pipeline anomaly detection is streamlining workflows, with some firms reporting a 15% reduction in false-positive alerts from inline inspection data. This shift supports advanced predictive maintenance models and comprehensive pipeline lifecycle management.

- Other significant trends include the expansion of remote pipeline monitoring and the deployment of real-time monitoring systems, which enhance visibility into asset conditions. Furthermore, automated defect recognition systems are becoming integral to processing the vast amounts of data generated, increasing both the speed and reliability of integrity assessments.

What challenges does the Pipeline Integrity Management Industry face during its growth?

- The challenge of aging infrastructure significantly affects the growth and operational dynamics of the industry.

- The primary challenge facing the market is the complexity of managing aging pipeline infrastructure, which is highly susceptible to degradation mechanisms like stress corrosion cracking (SCC). These older assets see a 30% higher incidence of integrity threats compared to newer lines. Addressing this requires significant investment in advanced pipeline repair technologies and comprehensive fitness-for-service (FFS) assessment.

- The transition to new energy sources introduces further complexity, with hydrogen pipeline compatibility and the integrity of carbon capture pipelines demanding new material and operational considerations. Moreover, providing unpiggable pipeline solutions for complex network segments remains a technical hurdle, although such solutions now cover 15% more of the network than a decade ago.

- Finally, ensuring subsea pipeline integrity and conducting detailed pipeline failure analysis present ongoing operational and financial challenges.

Exclusive Technavio Analysis on Customer Landscape

The pipeline integrity management market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the pipeline integrity management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Pipeline Integrity Management Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, pipeline integrity management market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aker Solutions ASA - Delivers engineering assessments and life cycle evaluations for subsea and onshore pipeline systems, ensuring safe operations through risk modeling and predictive maintenance for enhanced asset reliability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aker Solutions ASA

- Audubon Companies LLC

- Azuria Corp.

- Baker Hughes Co.

- Brand Industrial Services Inc.

- Bureau Veritas SA

- Dexon Technology PLC

- Emerson Electric Co.

- Fluor Corp.

- General Electric Co.

- Halliburton Co.

- Intertek Group Plc

- Pembina Pipeline Corp.

- ROSEN Swiss AG

- SGS SA

- T.D. Williamson Inc.

- TechnipFMC plc

- TUV Rheinland Group

- TWI Ltd.

- Yokogawa Electric Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Pipeline integrity management market

- In August 2024, the Pipeline and Hazardous Materials Safety Administration released a congressional report highlighting the challenges and detection gaps in applying current sensor technologies to nonmetallic plastic distribution pipes.

- In October 2024, Enbridge announced a collaboration with Microsoft to deploy AI and intelligent automation for enhancing pipeline integrity, aiming to proactively identify maintenance needs and improve leak prevention measures.

- In January 2025, the Pipeline and Hazardous Materials Safety Administration issued a final rule on gas pipeline leak detection and repair, establishing new protocols and performance standards for advanced detection systems to reduce methane emissions.

- In January 2025, DarkVision Technologies launched its Kraken in-line inspection platform, which uses advanced acoustic imaging to provide high-resolution internal views of pipelines for identifying subtle defects.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Pipeline Integrity Management Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.9% |

| Market growth 2026-2030 | USD 2600.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.5% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Russia, Germany, UK, France, Italy, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The pipeline integrity management market is defined by a critical shift from reactive repairs to proactive, intelligence-led strategies. A comprehensive asset integrity management program, incorporating systematic risk-based inspection (RBI) and fitness-for-service (FFS) assessment, has demonstrated the capacity to reduce unscheduled downtime by up to 25%.

- This evolution is driven by advanced technologies, including inline inspection (ILI) with magnetic flux leakage (MFL) and ultrasonic testing (UT) for precise anomaly detection. Innovations in non-destructive testing (NDT) and pipeline pigging are addressing challenges like stress corrosion cracking (SCC).

- Operators are deploying robust cathodic protection systems, conducting pipeline coating inspection, and using direct current voltage gradient (DCVG) surveys to combat corrosion. Furthermore, acoustic emission monitoring and pipeline strain monitoring provide real-time insights, complemented by sophisticated pipeline data analytics and digital twin technology.

- Adherence to stringent regulatory compliance management is pushing the adoption of superior leak detection systems, while material property verification and hydrostatic testing ensure structural soundness.

What are the Key Data Covered in this Pipeline Integrity Management Market Research and Growth Report?

-

What is the expected growth of the Pipeline Integrity Management Market between 2026 and 2030?

-

USD 2.60 billion, at a CAGR of 4.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Onshore, and Offshore), Service (Inspection service, Cleaning service, and Others), Type (Crude oil, Natural gas, Refined products, and LNG) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Stringent regulatory requirements associated with pipeline integrity management, Aging infrastructure

-

-

Who are the major players in the Pipeline Integrity Management Market?

-

Aker Solutions ASA, Audubon Companies LLC, Azuria Corp., Baker Hughes Co., Brand Industrial Services Inc., Bureau Veritas SA, Dexon Technology PLC, Emerson Electric Co., Fluor Corp., General Electric Co., Halliburton Co., Intertek Group Plc, Pembina Pipeline Corp., ROSEN Swiss AG, SGS SA, T.D. Williamson Inc., TechnipFMC plc, TUV Rheinland Group, TWI Ltd. and Yokogawa Electric Corp.

-

Market Research Insights

- Market dynamics are increasingly influenced by technological integration, where advanced pipeline integrity software and smart pig technology enhance operational efficiency. The adoption of remote pipeline monitoring has reduced manual inspection needs, with some operators reporting travel cost reductions of over 30% in inaccessible areas.

- Similarly, the use of drone-based inspection has accelerated survey timelines by up to 50% compared to traditional ground crews. In demanding environments, ensuring subsea pipeline integrity benefits from specialized robotics and real-time data feeds.

- This shift toward automated and data-centric approaches, including solutions for previously unpiggable pipeline sections, allows for more accurate lifecycle management and better-informed maintenance decisions, directly impacting asset reliability and safety performance.

We can help! Our analysts can customize this pipeline integrity management market research report to meet your requirements.

RIA -

RIA -