Europe Power Tools Market Size 2026-2030

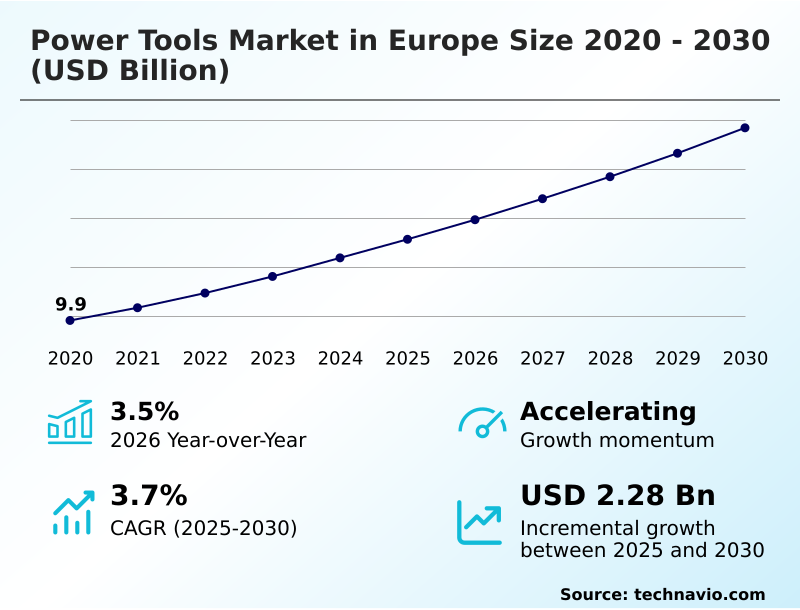

The europe power tools market size is valued to increase by USD 2.28 billion, at a CAGR of 3.7% from 2025 to 2030. Expansion of professional construction and infrastructure sector will drive the europe power tools market.

Major Market Trends & Insights

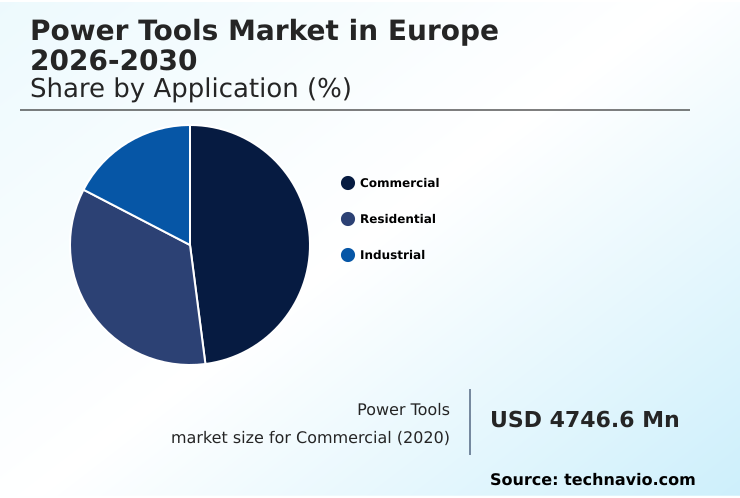

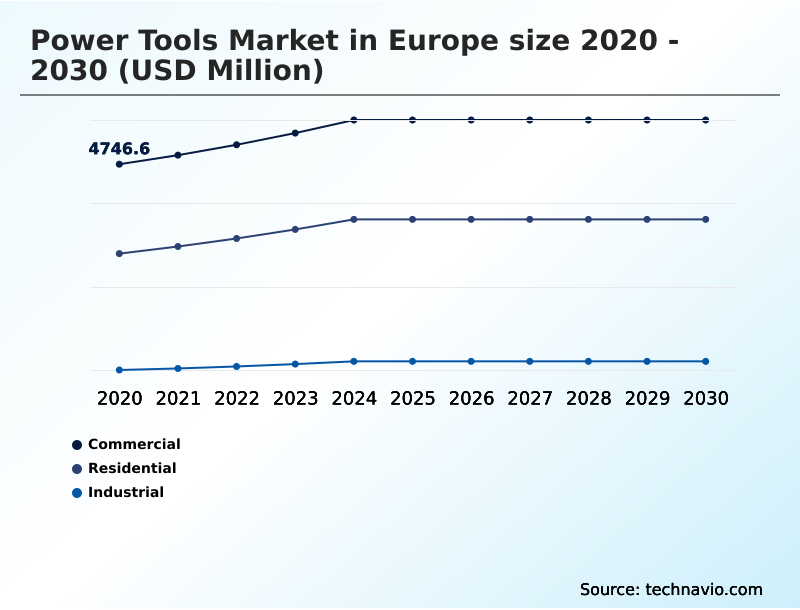

- By Application - Commercial segment was valued at USD 5.40 billion in 2024

- By Technology - Electric segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.94 billion

- Market Future Opportunities: USD 2.28 billion

- CAGR from 2025 to 2030 : 3.7%

Market Summary

- The power tools market in Europe is undergoing a significant transformation, driven by technological advancements and evolving end-user requirements. The shift away from traditional corded equipment toward high-performance cordless systems, powered by advanced lithium-ion battery technology and efficient brushless motor systems, is a defining characteristic.

- This transition enhances jobsite productivity metrics and safety across professional construction equipment and industrial maintenance tools. Concurrently, a growing DIY culture fuels demand for user-friendly residential renovation tools. A key business scenario involves construction firms leveraging software-defined tooling ecosystems with smart tool connectivity for digital asset management.

- This allows for real-time performance monitoring and predictive analytics for tools, optimizing inventory and reducing downtime. However, this progress is tempered by challenges such as reliance on imported semiconductor chips and navigating complex REACH directives compliance. The market's future hinges on balancing innovation in areas like eco-design manufacturing processes with the need for resilient supply chains.

What will be the Size of the Europe Power Tools Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Europe Power Tools Market Segmented?

The europe power tools industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Commercial

- Residential

- Industrial

- Technology

- Electric

- Pneumatic

- Engine-driven

- Type

- Drilling and fastening tools

- Cutting tools

- Grinding and polishing tools

- Others

- Geography

- Europe

- Germany

- France

- UK

- Europe

By Application Insights

The commercial segment is estimated to witness significant growth during the forecast period.

The commercial segment is defined by professional activities where equipment must deliver uncompromising performance and durability. Demand is driven by organizations in construction and infrastructure development requiring high-throughput, precision-engineered tooling.

Purchasing decisions prioritize total cost of ownership calculation and jobsite productivity metrics over initial price, with a focus on tools featuring advanced electric motors and robust pneumatic fastening systems.

The adoption of high-performance cordless systems has been shown to improve labor efficiency by up to 15%.

This segment's reliance on industrial-grade drilling and heavy-duty landscaping tools makes it a critical driver of innovation, particularly in sustainable material engineering and professional construction equipment designed for maximum uptime.

The Commercial segment was valued at USD 5.40 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- End-user decisions in the market are increasingly complex, weighing the cordless vs corded power tool performance for specific tasks. The brushless motor impact on tool lifespan is a key consideration for professionals calculating the cost of ownership for professional power tools.

- Similarly, lithium-ion battery runtimes for professional use are scrutinized, with advancements in high-voltage cordless technology pushing the boundaries of what is possible. The impact of IoT on power tool asset management is transforming operations, as predictive maintenance for industrial power tools becomes a reality. This shift allows for optimizing jobsite efficiency with connected tools.

- On the human-centric side, the ergonomic design benefits in construction tools are paramount, as is understanding how to reduce hand-arm vibration in power tools. The need for dust extraction systems for OSHA compliance highlights a growing focus on safety. Businesses must also understand how circular economy affects tool manufacturing and the sustainable materials in power tool construction.

- The debate over pneumatic vs electric fastening system efficiency continues, but smart tool features are a clear advantage. The best power tools for heavy-duty industrial applications now often feature brand-agnostic battery platform ecosystems, offering greater flexibility.

- Ultimately, selecting power tool solutions for infrastructure projects or even deciding how to choose tools for residential DIY projects requires a holistic evaluation of these evolving technological and sustainability factors. For instance, new connected systems show more than double the operational accuracy in high-volume assembly tasks compared to non-connected predecessors.

What are the key market drivers leading to the rise in the adoption of Europe Power Tools Industry?

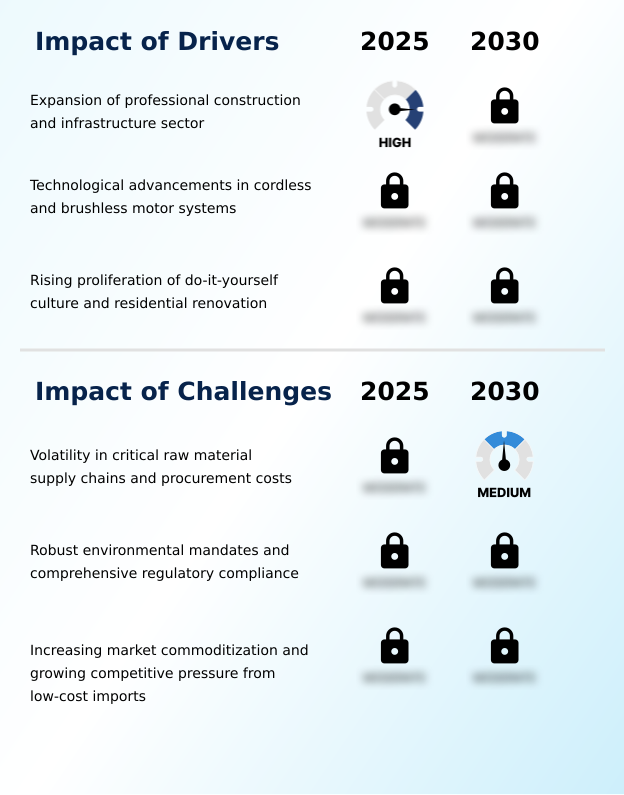

- The key market driver is the expansion of the professional construction and infrastructure sector.

- Market growth is propelled by a convergence of construction sector expansion, technological leaps, and changing consumer behavior. The resurgence in professional construction and infrastructure projects creates sustained demand for reliable equipment.

- Simultaneously, rapid advancements in battery-operated alternatives, particularly high-performance cordless systems featuring brushless motors, are revolutionizing jobsite efficiency. These cordless platforms can increase worker productivity by up to 20% by eliminating time spent managing cables.

- The expanding DIY culture, supported by the availability of accessible residential renovation tools and online resources, provides a resilient and growing secondary market. This consumer-led demand complements the professional sector, ensuring broad-based momentum across the industry.

What are the market trends shaping the Europe Power Tools Industry?

- The integration of artificial intelligence and the Internet of Things is an emerging market trend. This is primarily focused on enhancing asset management capabilities for high-performance equipment.

- Key trends are reshaping the market, moving beyond raw power to intelligent, sustainable solutions. The integration of AI and IoT enables sophisticated digital asset management, where software-defined tooling ecosystems provide real-time data. This connectivity facilitates predictive maintenance, with some users reporting a 25% reduction in unplanned equipment downtime.

- Concurrently, a strategic alignment with circular economy principles is driving the adoption of tool-as-a-service models and designs emphasizing repairability. Furthermore, the heightened focus on user health is leading to innovations in lightweight tool architecture and advanced ergonomic tool design. Tools equipped with superior vibration control can reduce operator fatigue by over 15%, enhancing both safety and productivity during prolonged use.

What challenges does the Europe Power Tools Industry face during its growth?

- A key challenge affecting industry growth is the volatility in critical raw material supply chains and associated procurement costs.

- The market faces significant headwinds from supply chain instability and rigorous regulatory frameworks. Pervasive volatility in the sourcing of critical raw materials, including high-grade steel components, and electronic parts like battery management systems has led to procurement cost increases of up to 30% for certain inputs. This places pressure on pricing strategies.

- Simultaneously, navigating an increasingly complex landscape of environmental mandates, such as the Restriction of Hazardous Substances (RoHS), requires substantial investment in R&D and compliance, which can extend product development cycles by 15-20%. These factors, coupled with market commoditization from low-cost imports, create a challenging operational environment requiring sophisticated strategic planning.

Exclusive Technavio Analysis on Customer Landscape

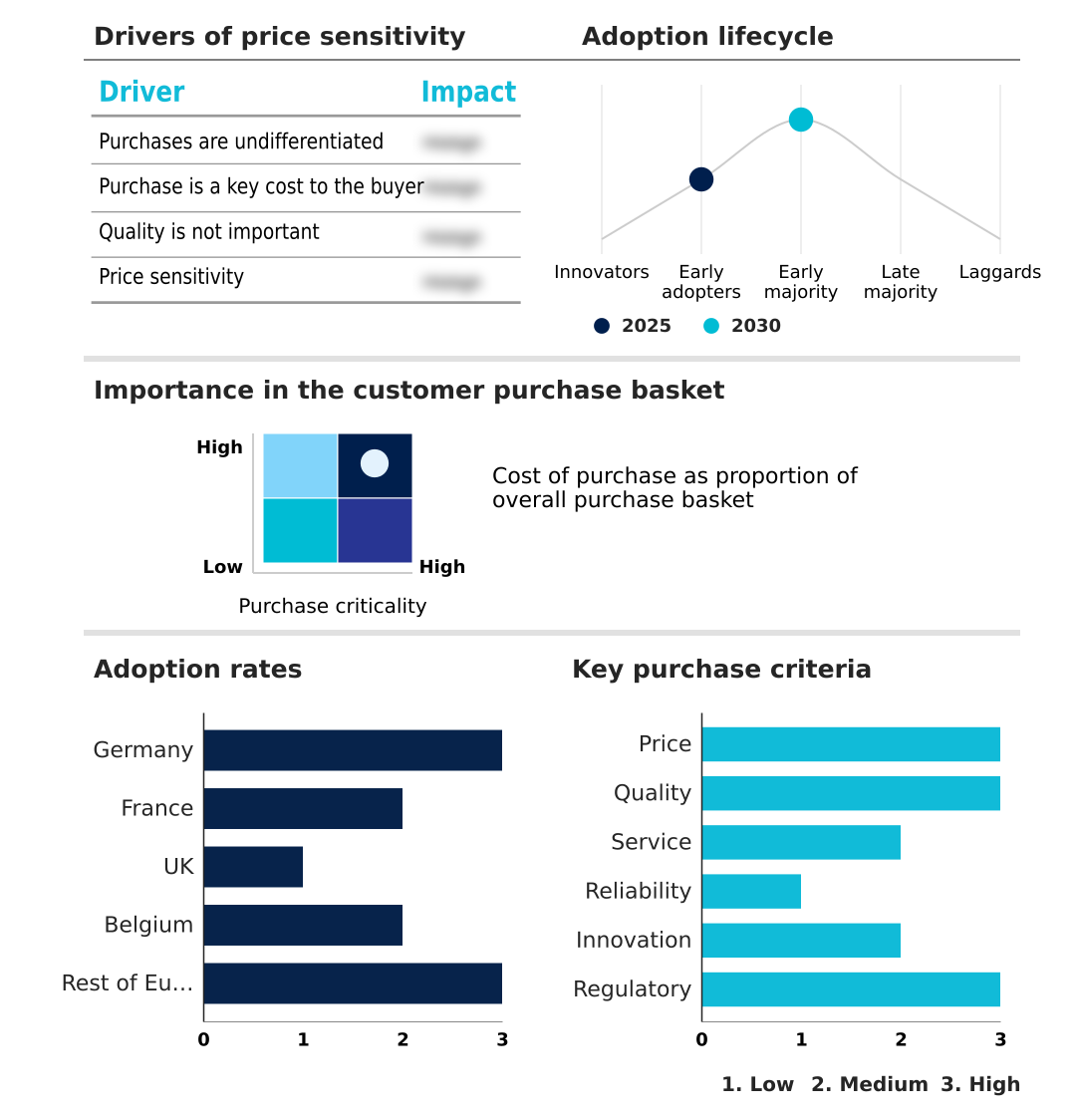

The europe power tools market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the europe power tools market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Europe Power Tools Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, europe power tools market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adolf Wurth GmbH and Co. KG - Offerings span a broad portfolio of power tools, including drilling, cutting, and fastening solutions for professional, industrial, and residential applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adolf Wurth GmbH and Co. KG

- ANDREAS STIHL AG and Co. KG

- Atlas Copco AB

- C. and E. Fein GmbH

- Draper Tools Ltd.

- Einhell Germany AG

- Emerson Electric Co.

- Festool GmbH

- FLEX-Elektrowerkzeuge GmbH

- Hilti AG

- Husqvarna AB

- Makita Corp.

- Metabowerke GmbH

- Mirka Ltd.

- Robert Bosch GmbH

- RUPES S.p.A.

- Scheppach GmbH

- SKIL

- Stanley Black and Decker Inc.

- Techtronic Industries Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Europe power tools market

- In October 2024, ANDREAS STIHL AG and Co. KG inaugurated its first manufacturing plant in Romania dedicated exclusively to battery-powered products, establishing a regional competence center for cordless equipment.

- In February 2025, Robert Bosch GmbH launched its Toolbox App 2.0, introducing AI-driven diagnostics for real-time tool health monitoring to enhance predictive maintenance in the professional sector.

- In March 2025, Stanley Black and Decker Inc. announced an 11% increase in European sales, driven by strategic pricing and strong demand for its professional-grade outdoor and construction equipment.

- In April 2025, Makita Corp. expanded its cordless product line by introducing new high-capacity battery units with advanced tabless cell technology, aiming to bridge the performance gap with petrol-powered machinery.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Europe Power Tools Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 214 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.7% |

| Market growth 2026-2030 | USD 2276.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.5% |

| Key countries | Germany, France, UK, Belgium and Rest of Europe |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The power tools market in Europe is defined by a strategic pivot towards intelligent and sustainable equipment. Boardroom decisions are increasingly influenced by the need to align with circular economy principles in manufacturing and stringent ecodesign for sustainable products regulations.

- The integration of sustainable material engineering and modular tool design is no longer a niche consideration but a central pillar of product strategy. This shift is driven by the necessity to mitigate risks associated with the carbon border adjustment mechanism and REACH directives compliance.

- For example, adopting a modular tool design that facilitates easier repairs has been shown to reduce out-of-warranty service costs by over 20%. The market's evolution is further shaped by technologies like tabless cell technology, high-capacity battery packs, and advanced electric motors.

- Innovations in brushless motor systems and pneumatic fastening systems continue, but the core focus is on creating integrated ecosystems featuring real-time performance monitoring and predictive analytics for tools. This requires investment in everything from semiconductor chips and permanent magnets to vibration-damping technologies and kickback control sensors, fundamentally altering the competitive landscape.

What are the Key Data Covered in this Europe Power Tools Market Research and Growth Report?

-

What is the expected growth of the Europe Power Tools Market between 2026 and 2030?

-

USD 2.28 billion, at a CAGR of 3.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Commercial, Residential, and Industrial), Technology (Electric, Pneumatic, and Engine-driven), Type (Drilling and fastening tools, Cutting tools, Grinding and polishing tools, and Others) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Expansion of professional construction and infrastructure sector, Volatility in critical raw material supply chains and procurement costs

-

-

Who are the major players in the Europe Power Tools Market?

-

Adolf Wurth GmbH and Co. KG, ANDREAS STIHL AG and Co. KG, Atlas Copco AB, C. and E. Fein GmbH, Draper Tools Ltd., Einhell Germany AG, Emerson Electric Co., Festool GmbH, FLEX-Elektrowerkzeuge GmbH, Hilti AG, Husqvarna AB, Makita Corp., Metabowerke GmbH, Mirka Ltd., Robert Bosch GmbH, RUPES S.p.A., Scheppach GmbH, SKIL, Stanley Black and Decker Inc. and Techtronic Industries Co. Ltd.

-

Market Research Insights

- Market dynamics are shaped by a pronounced shift toward battery-operated alternatives, which improve operational flexibility. The adoption of smart tool connectivity enhances inventory control, with some firms reporting a 15% reduction in tool loss.

- Furthermore, the focus on ergonomic tool design and user health protection features is critical; tools with integrated dust extraction systems achieve over 90% compliance with new occupational safety standards. This emphasis on advanced, efficient, and safe professional-grade devices is reshaping purchasing criteria.

- The market is also seeing a rise in tool-as-a-service models, which can improve capital efficiency for large enterprises by converting capital expenditures into operational costs, fostering a more agile approach to equipment acquisition.

We can help! Our analysts can customize this europe power tools market research report to meet your requirements.

RIA -

RIA -