Private Label Food And Beverages Market Size 2025-2029

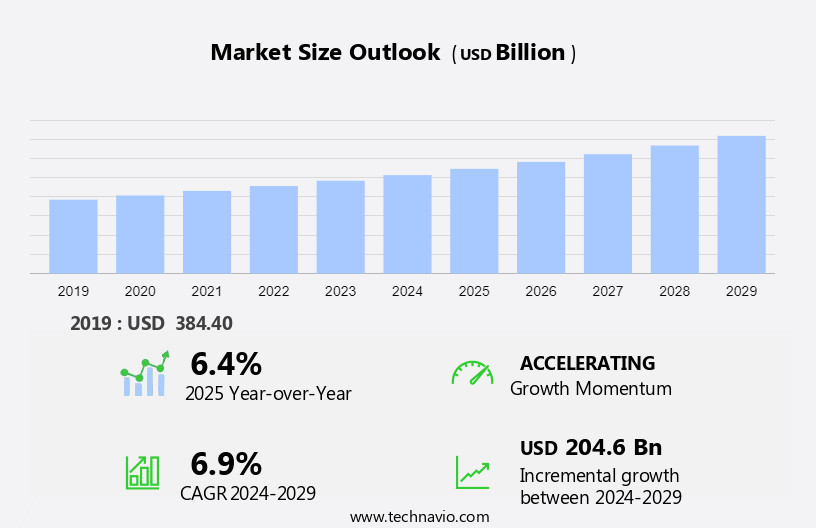

The private label food and beverages market size is forecast to increase by USD 204.6 billion at a CAGR of 6.9% between 2024 and 2029.

- The private label food and beverage market is witnessing significant growth due to several key trends. The increasing preference for healthier food options, such as non-GMO, organic, and gluten-free, is driving the demand for private label products in various categories, including soup, coffee, ice cream, yogurt, chocolate, tea, meat, condiments, sauces, dressings, bakery products, and baby food. Furthermore, the rise of e-commerce platforms is enabling private label brands to expand their reach and penetrate new markets, especially in niche categories like alcoholic drinks, premium chocolate, confectionery, olive oil, savory snacks, cheese, and bottled water. However, challenges such as maintaining product quality and consistency, ensuring food safety, and effective packaging design remain crucial for private label companies to succeed in this competitive landscape.

What will be the Size of the Market During the Forecast Period?

- The private label food and beverage market encompasses a diverse range of products sold under the brand names of retailers rather than recognized manufacturers. This market segment includes offerings from convenience stores, dollar stores, general merchandise retailers, department stores, e-retailers, and others. Market size is significant, with continued growth driven by consumer preferences for affordable, convenient, and high-quality options. Clean label products, non-GMO offerings, and transparent labeling are increasingly popular trends, reflecting a focus on health and wellness.

- Private label product categories span bakery items, dairy, meat, and condiments and sauces. Retailers continually strive to enhance product quality, meeting evolving consumer demands and expectations. The private label food and beverage market's growth trajectory remains strong, as retailers leverage their brand recognition and consumer trust to capture market share in various product categories.

How is this Industry segmented and which is the largest segment?

The industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Distribution Channel

- Offline

- Online

- Product

- Food

- Beverages

- Geography

- Europe

- Germany

- UK

- North America

- Canada

- US

- APAC

- China

- India

- Japan

- Middle East and Africa

- South America

- Brazil

- Europe

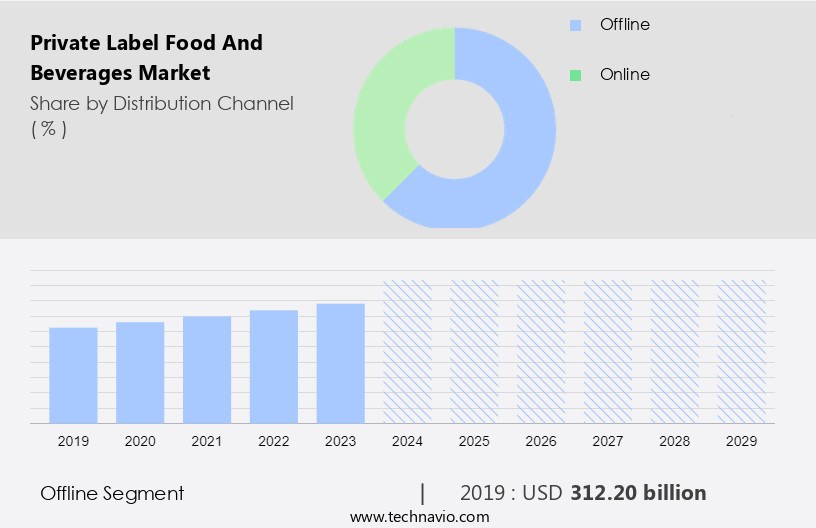

By Distribution Channel Insights

- The offline segment is estimated to witness significant growth during the forecast period.

Private label food and beverages are a significant category In the US retail market, with supermarkets, hypermarkets, grocery stores, hard discount stores, dollar stores, and convenience stores serving as the primary distribution channels. The expansion of private label companies In the US is a key growth driver for this segment. For instance, Aldi Stores, a German-owned chain known for its affordable prices and private label brands, expanded its footprint In the Southeast region in 2023, opening new locations throughout Louisiana. With a 15,000 square meter retail space, Aldi's new store in Shenzhen, China, is strategically located near the North high-speed rail station In the Longhua district.

Get a glance at the Private Label Food And Beverages Industry report of share of various segments Request Free Sample

The offline segment was valued at USD 312.20 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

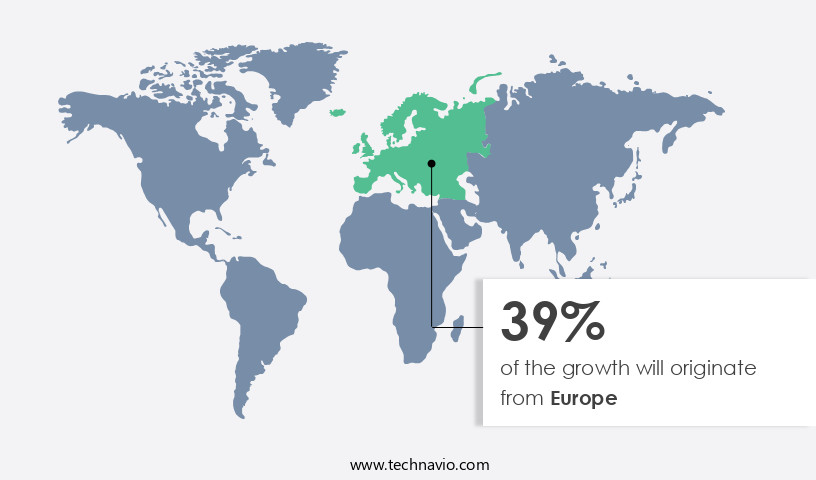

- Europe is estimated to contribute 39% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The European market is a significant sector, with consumers increasingly preferring these products as cost-effective alternatives to branded items. Retailers, including supermarkets and hypermarkets, convenience stores, dollar stores, general merchandise retailers, department stores, e-retailers, and others, have been investing heavily in brand development and product promotion. Private labels cater to various categories such as non-GMO bakery products, cereals, dairy products, yogurt, ice cream, baby food, poultry, eggs, fish, condiments and sauces, deli dressings, salads, gravies and sauces, general food, savory snacks, confectionery, soup, processed food, coffee, tea, bottled water, juices, carbonated beverages, sports drinks, alcoholic drinks, and more. These offerings are accessible through both online and offline channels, providing consumers with convenience and flexibility. The market's growth can be attributed to the increasing focus on health benefits, premium private-label products, and product quality.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Private Label Food And Beverages Industry?

Increasing dollar value share of private label brands is the key driver of the market.

- Private label food and beverages account for a significant portion of the overall growth in consumer packaged goods sales in the US. Supermarkets and Hypermarkets, Convenience Stores, Dollar Stores, General Merchandise Retailers, Department Stores, E-Retailers, and others continue to expand their private label offerings to cater to consumers' evolving preferences. The increasing popularity of private label brands can be attributed to several factors, including competitive pricing, easy availability, and the introduction of premium and specialty products. In the food and beverage category, private label brands have gained traction with offerings such as Non-GMO bakery products, cereals, dairy products including yogurt and ice cream, baby food, poultry, eggs, fish, condiments and sauces, deli dressings, salads, gravies and sauces, general food, savory snacks, confectionery, soup, processed food, coffee, tea, bottled water, juices, carbonated beverages, sports drinks, and alcoholic drinks.

- Consumers are increasingly drawn to private label brands due to their perceived high product quality, which is often on par with or even surpassing that of national brands. For instance, Kirkland Signature, a popular private label brand, has seen strong sales growth In the US due to its competitive pricing and perceived product quality In the dairy, meat, carbonated drinks, and other categories. Overall, the trend towards beverages is expected to continue, as consumers seek affordable and high-quality options.

What are the market trends shaping the Private Label Food And Beverages Industry?

Increasing online presence of private label brands is the upcoming market trend.

- Private label food and beverage products have gained significant traction in retail markets, with supermarkets and hypermarkets, convenience stores, dollar stores, general merchandise retailers, department stores, and e-retailers increasingly offering their own brands. The convenience of products, coupled with their competitive pricing, appeals to consumers. In the food category, bakery products, cereals, dairy items like yogurt and ice cream, baby food, poultry, eggs, fish, and condiments and sauces, deli dressings, salads, gravies and sauces, general food, savory snacks, confectionery, soup, processed food, coffee, tea, bottled water, juices, carbonated beverages, sports drinks, and alcoholic drinks are popular offerings.

- With the rise of internet usage and e-commerce, private label sales have expanded online. Major retailers, such as Target Corp. And Costco Wholesale, sell their products through e-commerce platforms, including Amazon. Consumers value the health benefits products, as well as their premium quality and labeling transparency. Private label dairy, meat, carbonated drinks, and other food and beverage items continue to gain popularity due to their affordability and consistent product quality.

What challenges does the Private Label Food And Beverages Industry face during its growth?

Low penetration of companies is a key challenge affecting the industry growth.

- These have gained significant attention In the retail sector, with supermarkets and hypermarkets, convenience stores, dollar stores, general merchandise retailers, department stores, e-retailers, and others offering their own branded products. However, the penetration rate in developing nations is lower than in countries like Switzerland, Spain, and the UK. National brand manufacturers, with their established brand consciousness, loyalty, and reputation, continue to dominate the global food and beverages market. Despite this, these companies face challenges in supply chain management, with smaller scales and less redundancy compared to national brands. These issues came to the forefront in 2022 when many products disappeared from shelves, leaving retailers to bear the brunt of the supply chain disruptions.

- Categories such as bakery products, cereals, dairy (yogurt, ice cream, eggs, poultry, fish), condiments and sauces, deli dressings, salads, gravies and sauces, general food, savory snacks, confectionery, soup, processed food, coffee, tea, bottled water, juices, carbonated beverages, sports drinks, and alcoholic drinks are all part of the market. Consumers are increasingly seeking health benefits from their food and beverage choices, leading to a growing demand for premium private-label products. Product quality remains a critical factor in consumer decision-making, and retailers must ensure that their private label offerings meet or exceed the quality of national brands. Effective labeling and clear communication about product ingredients, certifications, and origin are essential to building consumer trust and loyalty.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aldi Stores Ltd.

- Amazon.com Inc.

- Carrefour SA

- Costco Wholesale Corp.

- Dollar General Corp.

- EDEKA ZENTRALE Stiftung and Co. KG

- Giant Eagle Inc.

- Giant of Maryland LLC

- HEB LP

- Hy Vee Inc.

- Koninklijke DSM NV

- Reliance Industries Ltd.

- Schwarz Unternehmenskommunikation GmbH and Co. KG

- Sobeys Inc.

- SouthEastern Grocers LLC

- Target Corp.

- Tata Sons Pvt. Ltd.

- Tesco Plc

- The Kroger Co.

- Trader Joes

- United Natural Foods Inc.

- Walmart Inc.

- Wegmans Food Markets

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a wide array of product categories, including bakery items, cereals, dairy products, yogurt, ice cream, baby food, poultry, egg, fish, condiments and sauces, deli dressings, salads, gravies and sauces, general food, savory snacks, confectionery, soup, processed food, coffee, tea, bottled water, juices, carbonated beverages, sports drinks, and alcoholic drinks. This market caters to various retail channels, such as supermarkets and hypermarkets, convenience stores, dollar stores, general merchandise retailers, department stores, e-retailers, and others. The demand for beverages continues to grow, driven by several factors. Consumers are increasingly seeking healthier options, leading to the popularity of non-GMO and organic products.

In addition, the rise of premium private-label products has also contributed to the market's expansion. These offerings often provide better value and quality than their branded counterparts, making them attractive to price-sensitive consumers. Labeling plays a crucial role In the food and beverage market. Consumers are becoming more conscious of the ingredients In their food and beverages, leading to a greater emphasis on clear and accurate labeling. Product quality is another essential factor, with retailers focusing on sourcing high-quality ingredients and implementing rigorous production processes to meet consumer expectations. Dairy products, including milk, cheese, and yogurt, are a significant segment of the market.

Moreover, consumers are increasingly turning to dairy products due to their affordability and perceived quality. Meat, particularly poultry and eggs, is another popular category, with offerings gaining traction due to their competitive pricing and consistent quality. Beverages, such as coffee, tea, bottled water, juices, carbonated beverages, sports drinks, and alcoholic drinks, are also essential components of the market. Consumers are drawn to beverages due to their affordability and the convenience they offer. The market is highly competitive, with retailers continually striving to differentiate themselves through product innovation, pricing strategies, and marketing efforts.

In addition, the market is also subject to various trends and consumer preferences, requiring retailers to remain agile and responsive to changing market dynamics. Retailers must remain innovative and responsive to meet the ever-changing needs and expectations of their customers. The market encompasses a wide range of product categories, from bakery items and cereals to dairy products, meat, and beverages. Regardless of the specific category, the focus on product quality, labeling, and consumer value remains a constant theme.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

196 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.9% |

|

Market growth 2025-2029 |

USD 204.6 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.4 |

|

Key countries |

US, Switzerland, Germany, UK, China, India, Canada, Japan, Brazil, and UAE |

|

Competitive landscape |

Leading Companies, market growth and forecasting , Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the Private Label Food And Beverages industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Europe, North America, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the private label food and beverages market growth of industry companies

We can help! Our analysts can customize this private label food and beverages market research report to meet your requirements.