Professional Services Market Size 2026-2030

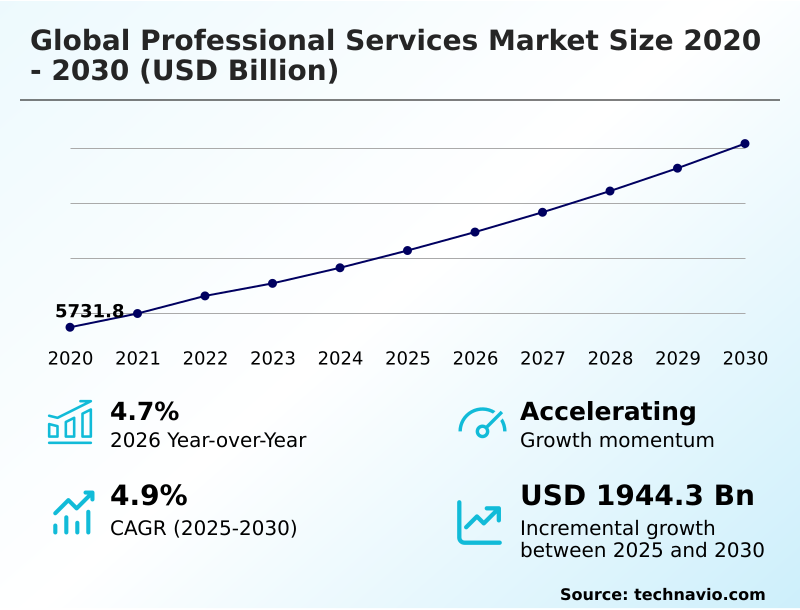

The professional services market size is valued to increase by USD 1944.3 billion, at a CAGR of 4.9% from 2025 to 2030. Institutionalization of agentic AI and autonomous service delivery will drive the professional services market.

Major Market Trends & Insights

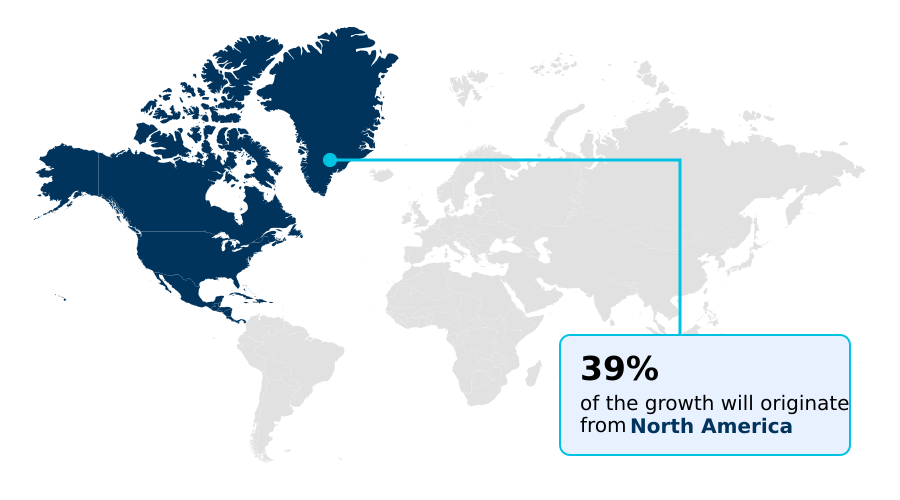

- North America dominated the market and accounted for a 38.6% growth during the forecast period.

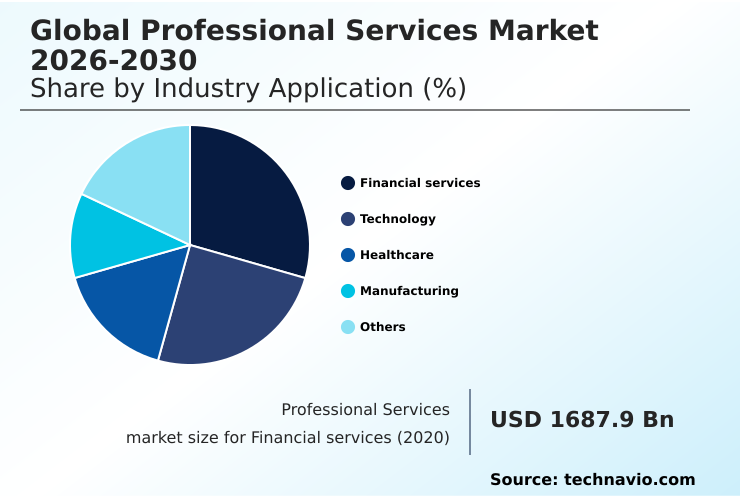

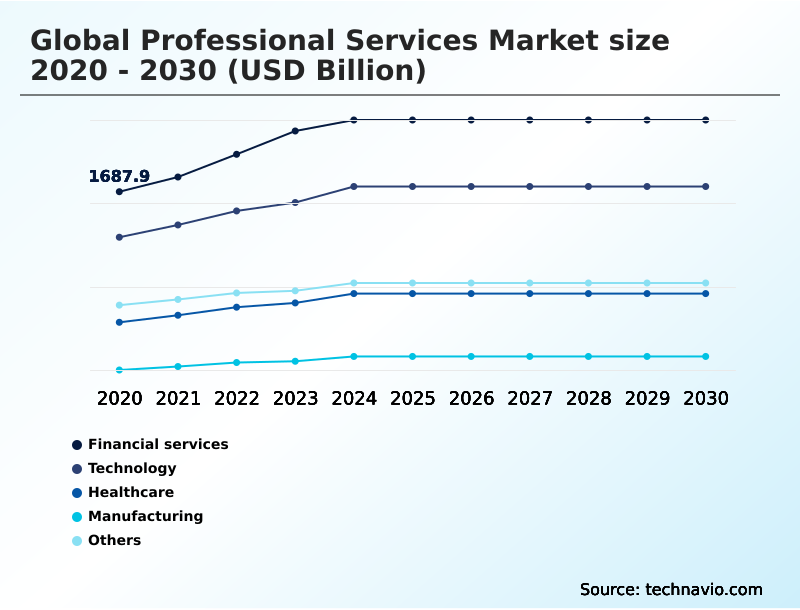

- By Industry Application - Financial services segment was valued at USD 2102.9 billion in 2024

- By Delivery Mode - On-site services segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3339.4 billion

- Market Future Opportunities: USD 1944.3 billion

- CAGR from 2025 to 2030 : 4.9%

Market Summary

- The professional services market is undergoing a significant transformation, pivoting from traditional, time-based consulting to value-driven, technology-augmented partnerships. Key drivers include the institutionalization of agentic AI and the demand for specialized ESG advisory to navigate complex regulatory landscapes. Firms are moving beyond basic automation, deploying autonomous service delivery models for tasks like predictive modeling and audit verification.

- A key business scenario involves a multinational manufacturing firm engaging a consultancy to re-engineer its global supply chain. By implementing digital twin technology and predictive maintenance protocols, the firm achieves a significant reduction in operational downtime and inventory costs, illustrating the shift toward outcome-oriented engagements.

- This evolution is also marked by challenges, such as the need to address structural human capital deficits by developing talent with advanced digital fluency.

- The market's future hinges on the ability of providers to integrate human expertise with sophisticated AI governance, ensuring data sovereignty while delivering measurable business outcomes through innovative, often subscription-based, advisory models that replace outdated billable hour structures.

What will be the Size of the Professional Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Professional Services Market Segmented?

The professional services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Industry application

- Financial services

- Technology

- Healthcare

- Manufacturing

- Others

- Delivery mode

- On-site services

- Remote services

- Hybrid models

- End-user

- Large enterprises

- SMEs

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Industry Application Insights

The financial services segment is estimated to witness significant growth during the forecast period.

The professional services market is segmented by industry application, delivery mode, and geography. Financial services represents a critical segment, where the complexity of global regulations and the adoption of fintech solutions drive demand for specialized advisory.

Firms are leveraging agentic AI and cloud-native architectures to enhance operational efficiency and manage cyber resilience. ESG advisory is another high-growth area, as institutions navigate stringent carbon disclosure mandates and green taxonomies.

The integration of autonomous contract drafting tools has improved document review efficiency by over 30%. This demand for digital transformation and value-based pricing models underscores the sector's shift toward technology-led, outcome-oriented engagements focused on data sovereignty and risk management.

The Financial services segment was valued at USD 2102.9 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Professional Services Market Demand is Rising in North America Get Free Sample

The geographic landscape of the professional services market is defined by varied regional dynamics.

North America, contributing nearly 38.6% of the market's incremental growth, leads in the adoption of agentic AI frameworks and corporate wellness consulting, driven by a focus on operational efficiency.

Europe's market is heavily shaped by regulatory demands, with a surge in ESG advisory and services related to sovereign cloud architecture to comply with data localization rules.

Meanwhile, the APAC region is the primary engine for volume growth, fueled by massive investments in digital infrastructure and smart city development, which have expanded access to professional business process management by over 30%.

In South America and the Middle East and Africa, growth is tied to the modernization of financial sectors and large-scale giga-projects, respectively, highlighting a global shift toward specialized, technology-driven advisory services.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic direction of the global professional services market 2026-2030 is increasingly shaped by the imperative to deliver measurable outcomes. Firms are adopting agentic AI for autonomous service delivery, moving beyond simple automation to handle complex professional workflows. A critical focus is ESG advisory for carbon disclosure mandates, a non-negotiable service line for clients facing stringent new regulations.

- Simultaneously, the demand for sovereign cloud for data localization compliance is reshaping IT consulting, as national security concerns drive the need for decentralized cloud architectures. The generative AI impact on billable hour models is profound, accelerating the shift toward value-based pricing in management consulting.

- This transition is not without hurdles, as navigating regulatory fragmentation in legal services and addressing human capital deficits in accounting requires significant investment in talent and technology. Organizations that successfully provide digital transformation consulting for large enterprises, coupled with robust cybersecurity auditing for cloud-native systems, are poised for leadership.

- The most successful firms are developing productized offerings for scalable legal services and implementing human-AI collaborative workflows in professional services. Firms offering climate-related financial disclosures advisory services are seeing their project pipelines grow at twice the rate of those with more generalized offerings.

- This new landscape demands a deep understanding of nearshoring trends driving consultancy demand and the nuances of digital core reinvention using generative AI to manage risk transfer strategies for digital infrastructure.

What are the key market drivers leading to the rise in the adoption of Professional Services Industry?

- The institutionalization of agentic AI and the shift toward autonomous service delivery are key drivers of market growth.

- The institutionalization of agentic AI is a primary driver propelling the professional services market toward autonomous service delivery. Facing persistent labor shortages, firms are deploying intelligent agents for end-to-end professional workflows, successfully decoupling revenue growth from headcount.

- This integration improves operational efficiency, with early adopters reporting a 40% increase in the speed of completing routine analytical tasks.

- Another major driver is the proliferation of sustainability consulting, fueled by stringent carbon disclosure mandates and investor pressure for transparent ESG advisory.

- The demand for sovereign cloud services has also escalated, driven by national digital security mandates that require localized data management.

- This has led to a significant shift toward high-value, specialized engagements focused on digital sovereignty services and cyber resilience, with the cloud advisory sub-segment expanding at a record pace.

What are the market trends shaping the Professional Services Industry?

- The increasing mandate for sustainability disclosures is a significant market trend, creating substantial demand for related advisory services.

- Key trends are reshaping the professional services market, driven by the industrialization of generative AI systems and a move toward value-based pricing. The transition away from traditional billable hour models is accelerating, with over 60% of large enterprises now preferring outcome-oriented engagement frameworks that link fees to strategic results.

- This shift is particularly evident in management consulting, where subscription-based advisory services provide predictable costs and recurring revenue streams. The demand for mandatory sustainability disclosures has also created a surge in ESG advisory, requiring a multidisciplinary blend of legal and data science expertise.

- Firms that have integrated AI-powered predictive modeling into their service offerings report a 25% improvement in forecast accuracy for clients, underscoring the move toward leveraging technological insights as a primary engine for growth.

What challenges does the Professional Services Industry face during its growth?

- The integration of artificial intelligence and the consequent risk of service commoditization present a key challenge to industry growth.

- The professional services market faces the dual challenge of AI integration and the consequent threat of service commoditization. The rapid advancement of agentic AI frameworks is rendering traditional billable hour models obsolete for baseline cognitive tasks, with automated systems reducing the cost of such services by up to 50% in some areas. This creates significant downward pressure on pricing.

- Another formidable challenge is the intensification of global regulatory fragmentation and data residency mandates, which complicate cross-border service delivery. Firms must now maintain highly localized expert teams and decentralized cloud architectures, increasing operational costs by an estimated 15-20% for multi-jurisdictional compliance.

- Furthermore, a structural human capital deficit persists, as the industry struggles with talent retention and the high cost of upskilling professionals in advanced digital fluency.

Exclusive Technavio Analysis on Customer Landscape

The professional services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the professional services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Professional Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, professional services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - Key offerings include strategic consulting, digital transformation, and risk advisory services, focusing on delivering technology-enabled, outcome-based solutions to complex business challenges across various industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- AECOM

- Aon plc

- Bain and Co. Inc.

- Boston Consulting Group Inc.

- Capgemini SE

- Cognizant Technology Solution

- Deloitte Touche Tohmatsu Ltd.

- Ernst and Young Global Ltd.

- Gartner Inc.

- IBM Corp.

- Infosys Ltd.

- Jacobs Solutions Inc.

- KPMG International Ltd.

- Marsh and McLennan Co. Inc.

- McKinsey and Co.

- PricewaterhouseCoopers LLP

- Publicis Groupe SA

- Tata Consultancy Services

- WPP Plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Professional services market

- In May 2025, Boston Consulting Group Inc. announced the acquisition of a leading AI governance boutique to enhance its digital transformation and agentic AI framework consulting services for enterprise clients.

- In March 2025, Deloitte Touche Tohmatsu Ltd. launched its 'Future of Work' initiative, a comprehensive service line combining strategy consulting with proprietary technology platforms to help clients redesign hybrid work models and talent retention strategies.

- In November 2024, Accenture Plc announced a strategic partnership with a major cloud provider to co-develop sovereign cloud solutions tailored for regulated industries, addressing data localization and national digital security mandates.

- In August 2024, KPMG International Ltd. received a major contract to provide ESG advisory and climate risk assessment services for a consortium of financial institutions, aligning their portfolios with new international sustainability reporting standards.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Professional Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 305 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.9% |

| Market growth 2026-2030 | USD 1944.3 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.7% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The professional services market is experiencing a structural pivot defined by the industrialization of agentic AI and autonomous service delivery. This transition moves firms beyond legacy systems toward integrated, technology-led models focused on sustainability consulting and ESG advisory.

- The proliferation of generative AI systems necessitates a new approach to professional workflows, emphasizing predictive modeling and autonomous contract drafting to enhance operational efficiency. As a result, there is a critical need for advanced AI ethics consulting and robust AI governance to manage data sovereignty and ensure cyber resilience.

- Leading firms are implementing proprietary agentic AI frameworks, which has been shown to enhance operational speed by an estimated 40%. The market is also seeing a definitive shift toward value-based pricing and subscription-based advisory models. This move away from traditional billable structures is a direct response to client demands for more transparent, outcome-oriented engagements.

- Service commoditization remains a key concern, compelling providers to focus on high-value human-AI collaborative workflows and specialized productized offerings that address complex challenges like regulatory fragmentation and persistent human capital deficits.

What are the Key Data Covered in this Professional Services Market Research and Growth Report?

-

What is the expected growth of the Professional Services Market between 2026 and 2030?

-

USD 1944.3 billion, at a CAGR of 4.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Industry Application (Financial services, Technology, Healthcare, Manufacturing, and Others), Delivery Mode (On-site services, Remote services, and Hybrid models), End-user (Large enterprises, and SMEs) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Institutionalization of agentic AI and autonomous service delivery, Artificial intelligence integration and service commoditization

-

-

Who are the major players in the Professional Services Market?

-

Accenture Plc, AECOM, Aon plc, Bain and Co. Inc., Boston Consulting Group Inc., Capgemini SE, Cognizant Technology Solution, Deloitte Touche Tohmatsu Ltd., Ernst and Young Global Ltd., Gartner Inc., IBM Corp., Infosys Ltd., Jacobs Solutions Inc., KPMG International Ltd., Marsh and McLennan Co. Inc., McKinsey and Co., PricewaterhouseCoopers LLP, Publicis Groupe SA, Tata Consultancy Services and WPP Plc

-

Market Research Insights

- The professional services market is characterized by dynamic shifts toward digital integration and outcome-oriented frameworks. The adoption of value-based pricing models is accelerating, with firms that utilize them reporting a 15% higher client retention rate compared to those on traditional billable hour models.

- This transition is propelled by the need for greater operational efficiency and a response to significant labor shortages. Furthermore, the integration of managed services and recurring revenue streams has stabilized financials for providers, allowing for sustained investment in technology.

- The focus on measurable effectiveness is paramount, as demonstrated by the fact that projects incorporating human-AI collaborative workflows are completed up to 25% faster. These dynamics underscore a market where technological insight is a primary engine for client satisfaction and competitive advantage.

We can help! Our analysts can customize this professional services market research report to meet your requirements.

RIA -

RIA -