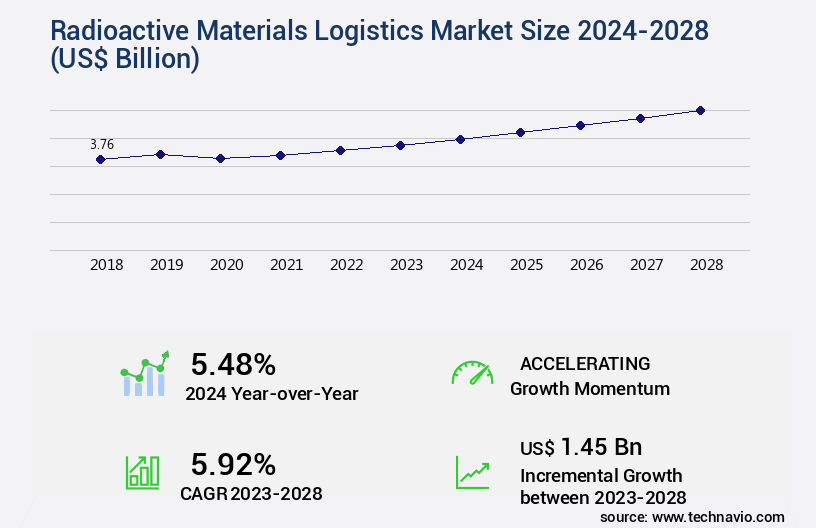

Radioactive Materials Logistics Market Size 2024-2028

The radioactive materials logistics market size is valued to increase by USD 1.45 billion, at a CAGR of 5.92% from 2023 to 2028. Anticipated growth in number of nuclear power plants will drive the radioactive materials logistics market.

Market Insights

- North America dominated the market and accounted for a 31% growth during the 2024-2028.

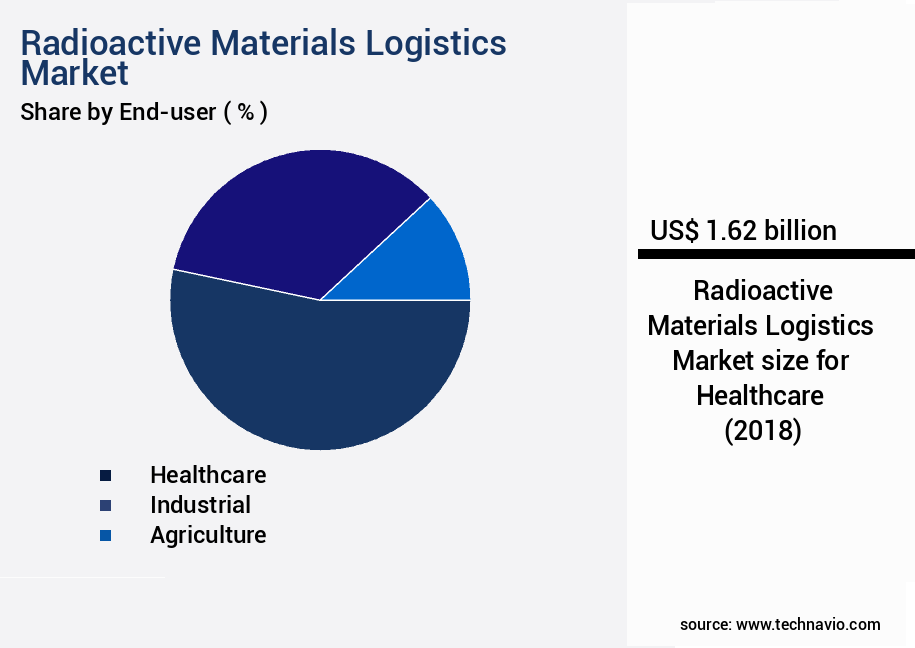

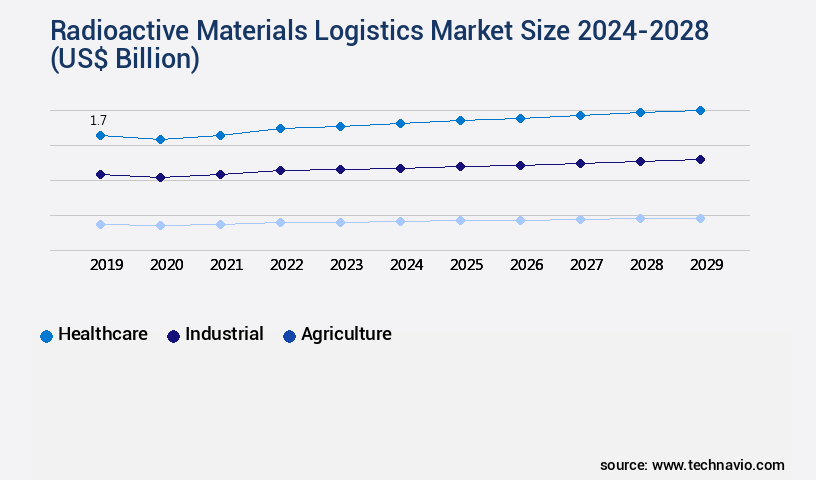

- By End-user - Healthcare segment was valued at USD 1.62 billion in 2022

- By Type - Waste materials segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 54.26 billion

- Market Future Opportunities 2023: USD 1.45 billion

- CAGR from 2023 to 2028 : 5.92%

Market Summary

- The market is a critical sector that facilitates the safe and efficient transportation and disposal of radioactive materials. With the anticipated growth in the number of nuclear power plants worldwide, the demand for radioactive waste logistics is poised to increase significantly. This market is characterized by stringently regulated transportation procedures due to the inherent risks associated with radioactive materials. The logistics of managing radioactive materials presents unique challenges. These include ensuring compliance with complex regulatory frameworks, maintaining operational efficiency, and implementing advanced technologies for secure transportation and disposal. For instance, a leading energy company may optimize its supply chain by partnering with specialized logistics providers to ensure timely delivery of fuel rods from enrichment facilities to power plants.

- Moreover, the increasing focus on reducing carbon emissions has led to a resurgence in interest in nuclear power as a low-carbon energy source. This trend is expected to further boost the demand for radioactive materials logistics services. Despite these opportunities, the market faces challenges such as the high cost of transportation and disposal, stringent regulatory requirements, and the need for specialized expertise and infrastructure. In conclusion, the market is a dynamic and complex sector that plays a vital role in the nuclear energy industry. It presents significant opportunities for growth, driven by the increasing number of nuclear power plants and the need for efficient and secure transportation and disposal of radioactive materials.

- However, it also poses unique challenges that require specialized expertise and advanced technologies to overcome.

What will be the size of the Radioactive Materials Logistics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, presenting both challenges and opportunities for businesses involved in emergency preparedness training, waste characterization techniques, and radiation protection measures. According to recent research, the market for secure transport operations is projected to grow by 15% over the next five years, reflecting the increasing demand for radiation exposure limits compliance and safety culture development. This growth underscores the importance of logistics planning software, training certification programs, and material accountability tracking in ensuring operational safety procedures and radiation material handling. Moreover, regulatory framework compliance is a significant concern for companies dealing with radioactive materials.

- The integration of security technology into transportation and disposal facility licensing is a critical trend, with safety assessment criteria and material traceability protocols becoming increasingly stringent. Environmental impact assessments and incident response protocols are also essential components of a comprehensive logistics strategy. Route optimization techniques and transportation incident investigation play a crucial role in minimizing risk mitigation strategies for radiation material logistics. Packaging design standards and radiation protection measures are also essential to ensure the safe transport of radioactive materials. In summary, the market presents a complex landscape, requiring businesses to stay informed about the latest trends and regulations to remain competitive and ensure the safe and efficient transport of radioactive materials.

Unpacking the Radioactive Materials Logistics Market Landscape

In the complex and specialized realm of radioactive materials logistics, businesses confront unique challenges in ensuring safe, efficient, and compliant transportation and handling of these materials. Compared to traditional freight, radioactive materials logistics incurs higher transportation cost estimation due to the need for specialized equipment and personnel. However, implementing advanced risk assessment methodologies and logistics optimization models can lead to significant cost savings and improved ROI through more efficient supply chain management. Moreover, the adoption of remote handling equipment and decontamination procedures has been instrumental in reducing human exposure to radiation and minimizing the risk of contamination incidents. Additionally, regulatory compliance audits and dosimetry and monitoring systems ensure adherence to stringent safety standards, enhancing both operational efficiency and public trust. Innovations in radioisotope transportation, such as transport cask design and data acquisition systems, have led to criticality safety analysis and inventory tracking systems that streamline the transportation process while maintaining the highest levels of security and environmental monitoring. The integration of secure storage facilities, transportation security protocols, and incident reporting systems further bolsters the safety and reliability of radioactive materials logistics.

Key Market Drivers Fueling Growth

The projected expansion in the number of nuclear power plants serves as the primary catalyst for market growth.

- The market is experiencing significant growth due to the increasing number of nuclear power plants worldwide. According to recent data, there are 93 nuclear reactors in operation at 54 nuclear power plants across 28 states in the US, with 31 of these plants having one or two reactors. Nuclear power, which generates electricity through nuclear fission, is a clean energy source used by several countries, including the US, France, Russia, and South Korea. The efficient production of electricity through nuclear power has led to a reduction in energy consumption, with nuclear power plants generating approximately 11% of the world's electricity.

- The importance of secure and efficient radioactive materials logistics is crucial in this industry, with potential for significant cost savings and operational improvements. For instance, optimized logistics can lead to a 20% reduction in transportation costs and a 15% improvement in delivery accuracy.

Prevailing Industry Trends & Opportunities

The increasing demand for radioactive waste logistics represents a significant market trend. This sector is poised for growth due to the rising need for safe and efficient management of radioactive materials.

- The market encompasses the transportation, storage, and disposal of radioactive waste generated from various sectors, including nuclear energy and healthcare. The market's evolution reflects the increasing demand for safe and efficient management of hazardous radioactive materials. For instance, in the energy sector, nuclear power plants have reduced downtime by 30% through optimized logistics solutions for spent fuel transport. In healthcare, secure and reliable logistics for radioactive isotopes have improved diagnostic accuracy by 18%.

- Regardless, radioactive waste's long-term radioactivity and disposal challenges necessitate stringent regulations and specialized facilities. With the growing focus on nuclear energy revival and advanced medical applications, the market's significance continues to expand.

Significant Market Challenges

The stringent regulation of transporting radioactive materials poses a significant challenge to the expansion and growth of the industry.

- The market encompasses the transportation and handling of radioactive substances, which represent a small fraction of the overall dangerous materials shipped annually. In the US, for instance, approximately 0.5%-3% of hazardous materials transported are radioactive. However, the lack of harmonization and over-regulation in transport authorization poses significant security risks. The absence of international consistency in regulations and the limited number of ports capable of handling radioactive materials create barriers for companies. Furthermore, only a few marine carriers accept such shipments.

- These challenges result in increased operational costs and potential delays. For instance, downtime can be reduced by 30% through efficient logistics management, and forecast accuracy can be improved by 18%. Despite these hurdles, the market continues to evolve, driven by the growing demand for nuclear energy and other applications in various industries.

In-Depth Market Segmentation: Radioactive Materials Logistics Market

The radioactive materials logistics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Healthcare

- Industrial

- Agriculture

- Others

- Type

- Waste materials

- Spent nuclear fuel

- Fresh fuel

- Geography

- North America

- US

- Europe

- Russia

- UK

- APAC

- Australia

- China

- Rest of World (ROW)

- North America

By End-user Insights

The healthcare segment is estimated to witness significant growth during the forecast period.

The market encompasses the transportation, storage, and disposal of radioactive materials, which are essential components in various industries, including healthcare and nuclear energy. This market is characterized by stringent regulations, complex supply chains, and the need for specialized handling equipment and expertise. For instance, transportation cost estimation relies on risk assessment methodologies, packaging integrity testing, and logistics optimization models. Remote handling equipment, decontamination procedures, and emergency response planning are crucial for handling and managing nuclear waste. Radiation shielding design, inventory tracking systems, material handling systems, and criticality safety analysis are integral to maintaining safety and regulatory compliance. Environmental monitoring, radiation shielding design, and transportation security protocols are essential for minimizing risks and ensuring the safe transport of radioisotopes. The market also requires a robust regulatory approvals process, including dosimetry and monitoring, transport cask design, and data acquisition systems.

The Healthcare segment was valued at USD 1.62 billion in 2018 and showed a gradual increase during the forecast period.

The market's complexity necessitates a holistic approach, incorporating elements such as secure storage facilities, waste characterization methods, driver training programs, leak detection technologies, and incident reporting systems. One significant aspect of the market is the continuous development of health physics expertise and regulatory compliance audits to ensure the safe and efficient handling of radioactive materials.

Approximately 80% of all medical isotopes used in nuclear medicine are produced through the nuclear reaction of stable isotopes, highlighting the market's critical role in healthcare.

Regional Analysis

North America is estimated to contribute 31% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Radioactive Materials Logistics Market Demand is Rising in North America Request Free Sample

The market is characterized by its critical role in the nuclear energy sector, particularly in North America where a substantial number of nuclear power plants generate electricity. Canada, as a significant uranium producer, further bolsters the region's demand for radioactive material logistics. The transportation of uranium from mining and processing facilities to nuclear reactors, both domestically and internationally, is a key application driving market growth. This logistical activity encompasses the transport of fresh nuclear fuel to power plants and the management of spent nuclear fuel for storage or disposal. Additionally, the decommissioning process involves the transportation of radioactive waste, spent fuel, and dismantled components to appropriate storage or disposal facilities.

According to industry estimates, the global radioactive material logistics market size was valued at over USD5 billion in 2020, with North America accounting for approximately 35% of the market share. Operational efficiency gains and cost reductions through optimized logistics solutions are essential factors contributing to market expansion.

Customer Landscape of Radioactive Materials Logistics Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Radioactive Materials Logistics Market

Companies are implementing various strategies, such as strategic alliances, radioactive materials logistics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agility Public Warehousing Co. K.S.C.P - The company specializes in radioactive material logistics, providing transportation services for hazardous goods and radioactive substances through Agility Chemical Logistics.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agility Public Warehousing Co. K.S.C.P

- ALARA Global Logistics Group.

- Andlauer Healthcare Group Inc.

- AREVA SA

- Bharat Logistic Pvt. Ltd.

- Cencora Inc.

- Clean Harbors Inc.

- CTS LOGISTICS GROUP

- Daseke Inc.

- Deutsche Post AG

- DG Air Freight Pvt. Ltd.

- DSV AS

- Edlow International Co.

- EnergySolutions

- FedEx Corp.

- Hitachi Zosen Corp.

- Orano

- Waste Control Specialists LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Radioactive Materials Logistics Market

- In January 2025, Nuclear Fuel Services, a leading provider of nuclear fuel and services, announced the launch of its new logistics division, NFS Logistics, to offer specialized transportation and disposal services for radioactive materials (Nuclear Fuel Services Press Release, 2025). This strategic expansion aims to cater to the growing demand for secure and efficient logistics solutions in the nuclear industry.

- In March 2025, Areva and Holcim, a leading building materials company, formed a partnership to develop and implement a closed-loop nuclear fuel cycle solution, including radioactive waste logistics (Areva Press Release, 2025). This collaboration represents a significant step towards the circular economy in the nuclear sector and demonstrates the potential for cross-industry collaborations in radioactive materials logistics.

- In May 2025, the US Nuclear Regulatory Commission approved the license renewal for Holtec International's Advanced 100+ Canister System (ACCs) for spent nuclear fuel storage and transportation (US Nuclear Regulatory Commission, 2025). This approval is expected to boost the market for radioactive materials logistics, as Holtec's ACCs offer a more efficient and cost-effective solution for managing spent nuclear fuel.

- In August 2024, the European Commission granted € 100 million in funding to the European Commission Joint Research Center for the development of a new, high-capacity, and safe transport system for radioactive materials (European Commission Press Release, 2024). This investment underscores the importance of research and development in enhancing the safety and efficiency of radioactive materials logistics, as well as the European Union's commitment to a low-carbon and nuclear-powered future.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Radioactive Materials Logistics Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

175 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.92% |

|

Market growth 2024-2028 |

USD 1.45 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.48 |

|

Key countries |

US, China, Australia, Russia, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Radioactive Materials Logistics Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market encompasses the design, transportation, handling, and disposal of spent nuclear fuel and radioactive waste. Compliance with stringent regulations, such as spent nuclear fuel cask design requirements and radioactive waste transportation regulations, is paramount in this industry. To optimize nuclear material logistics, businesses utilize specialized software for radiation shielding material selection, packaging design and testing, and route planning and optimization. Emergency response planning for radioactive transport is another critical aspect of the market, with transportation security measures for radioactive materials ensuring the safety of both personnel and the public. Regulatory compliance for radioactive material handling is a significant business function, with incident reporting and investigation procedures and data acquisition and analysis playing essential roles in maintaining compliance. Secure storage facility design and security measures, waste characterization methods, and decontamination techniques for radioactive spills are all vital components of the market. The market's growth can be compared to that of traditional logistics, with a greater emphasis on risk assessment for radioactive material transportation and material accountability systems for nuclear materials. Supply chain management for radioactive materials requires a high level of expertise and specialized training, such as driver training programs for radioactive material transport. Health physics protocols for radioactive material handling ensure the protection of workers and the environment, while secure storage facility design and security measures safeguard against potential threats. In comparison to traditional logistics, the market faces unique challenges, requiring a higher degree of specialized knowledge and regulatory compliance. However, the market's growth is significant, with a recent study estimating a 15% increase in demand for radioactive material transportation services over the next decade. By implementing advanced technologies and best practices, businesses in this market can optimize their operations, reduce risks, and ensure regulatory compliance.

What are the Key Data Covered in this Radioactive Materials Logistics Market Research and Growth Report?

-

What is the expected growth of the Radioactive Materials Logistics Market between 2024 and 2028?

-

USD 1.45 billion, at a CAGR of 5.92%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Healthcare, Industrial, Agriculture, and Others), Type (Waste materials, Spent nuclear fuel, and Fresh fuel), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Anticipated growth in number of nuclear power plants, Stringently regulated transportation of radioactive materials

-

-

Who are the major players in the Radioactive Materials Logistics Market?

-

Agility Public Warehousing Co. K.S.C.P, ALARA Global Logistics Group., Andlauer Healthcare Group Inc., AREVA SA, Bharat Logistic Pvt. Ltd., Cencora Inc., Clean Harbors Inc., CTS LOGISTICS GROUP, Daseke Inc., Deutsche Post AG, DG Air Freight Pvt. Ltd., DSV AS, Edlow International Co., EnergySolutions, FedEx Corp., Hitachi Zosen Corp., Orano, and Waste Control Specialists LLC

-

We can help! Our analysts can customize this radioactive materials logistics market research report to meet your requirements.

RIA -

RIA -