Rapid Thermal Processing Equipment Market Size 2026-2030

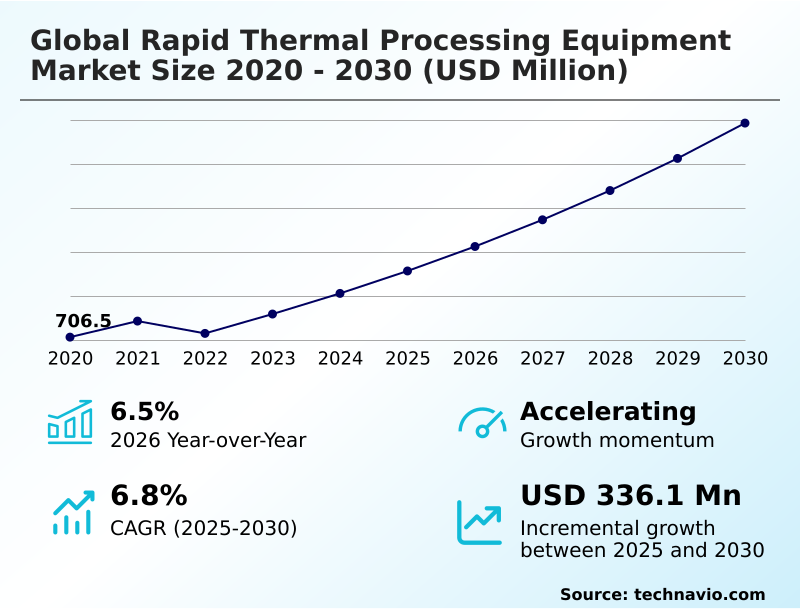

The rapid thermal processing equipment market size is valued to increase by USD 336.1 million, at a CAGR of 6.8% from 2025 to 2030. Aggressive scaling of semiconductor nodes to advanced levels will drive the rapid thermal processing equipment market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 57.3% growth during the forecast period.

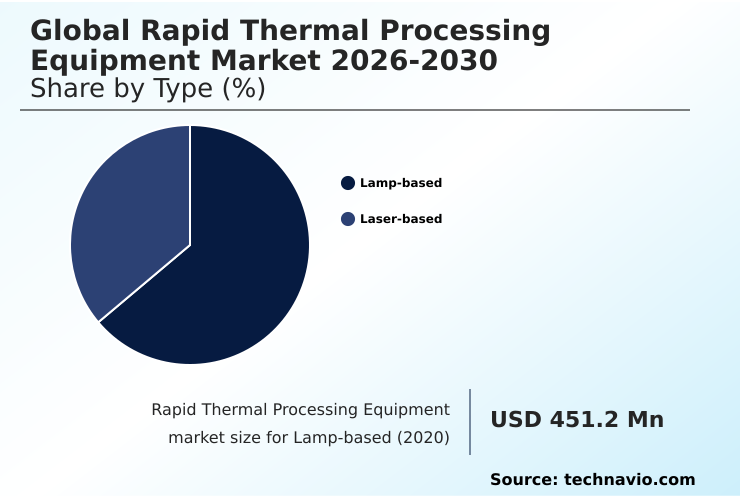

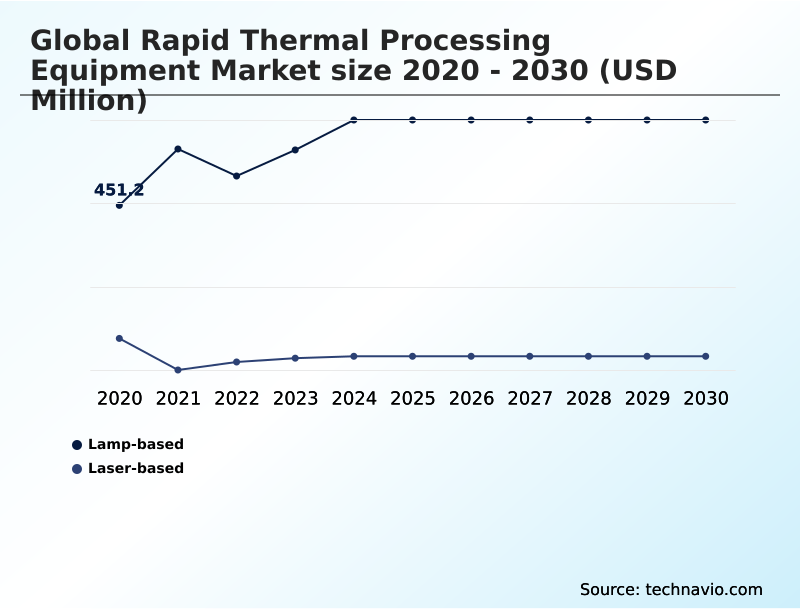

- By Type - Lamp-based segment was valued at USD 576.9 million in 2024

- By Application - Industrial segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 486.5 million

- Market Future Opportunities: USD 336.1 million

- CAGR from 2025 to 2030 : 6.8%

Market Summary

- The rapid thermal processing equipment market is integral to the advancement of the semiconductor industry, enabling the fabrication of smaller, faster, and more efficient integrated circuits. These systems provide precise, high-temperature treatments over very short durations, a critical capability for processes such as dopant activation, defect annealing, and film densification.

- Market momentum is driven by the relentless scaling of semiconductor nodes and the proliferation of high-performance computing, AI, and IoT applications, which demand increasingly complex chip architectures. For instance, a manufacturer of AI accelerators must maintain stringent thermal uniformity to maximize the yield of functional dies per wafer, directly impacting production costs and market competitiveness.

- Concurrently, the industry is expanding its use of wide-bandgap materials like silicon carbide for power electronics in electric vehicles and renewable energy systems. This shift necessitates specialized thermal processing equipment capable of handling higher temperatures and different substrate properties.

- However, the high capital investment required for these advanced tools and the persistent shortage of a skilled workforce capable of operating and maintaining them pose significant constraints on market expansion. Strategic navigation of these dynamics is essential for stakeholders to capitalize on emerging opportunities.

What will be the Size of the Rapid Thermal Processing Equipment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Rapid Thermal Processing Equipment Market Segmented?

The rapid thermal processing equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Lamp-based

- Laser-based

- Application

- Industrial

- Research and development

- Technology

- Fully automated

- Semi-automated

- Manual

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- APAC

By Type Insights

The lamp-based segment is estimated to witness significant growth during the forecast period.

The lamp-based segment is foundational to the rapid thermal processing equipment market, providing essential capabilities for high-volume semiconductor manufacturing processes.

These systems leverage high-intensity lamps for wafer surface treatment, ensuring precise thermal budget control during critical steps like dopant activation and defect annealing.

Their role is vital in fabricating a range of devices, from power electronics manufacturing to standard logic chips, where achieving high thermal uniformity across three-hundred-millimeter wafers is a prerequisite for semiconductor yield enhancement.

As foundry capacity expansion continues, the demand for reliable and cost-effective lamp-based solutions grows, particularly for mature technology nodes.

Innovations focus on improving real-time metrology integration, which has been shown to reduce process variability by over 15%, enhancing overall equipment uptime improvement and supporting high-mix production environments.

The Lamp-based segment was valued at USD 576.9 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 57.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Rapid Thermal Processing Equipment Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the rapid thermal processing equipment market is dominated by APAC, which accounts for over 57% of the incremental growth, driven by massive foundry capacity expansion and a focus on consumer electronics manufacturing.

This region's leadership is reinforced by its robust semiconductor supply chain resilience and a high concentration of facilities specializing in high-bandwidth memory production and advanced packaging solutions.

North America is experiencing a resurgence due to strategic investments in domestic fab automation software and cleanroom equipment standards, aimed at bolstering aerospace and defense electronics production. Europe is concentrating on automotive semiconductor reliability and industrial IoT deployments.

Regional growth is accelerating, with North America showing the highest projected CAGR, while the Middle East and Africa represent a fast-emerging market, demonstrating a nearly 8% growth rate.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Advancements in the global rapid thermal processing equipment market are increasingly defined by specialized applications. For instance, rapid thermal processing for SiC substrates is critical for the electric vehicle industry, while laser-based annealing for 3D NAND memory is essential for increasing data storage density. The push toward smaller transistors necessitates millisecond annealing for advanced logic nodes to maintain performance.

- Consequently, RTP equipment for power device manufacturing must handle higher temperatures with exceptional control. A key challenge is maintaining thermal budget control in GAA transistors, which demands sophisticated process monitoring. Firms are optimizing dopant activation with flash anneal techniques and closely studying the impact of RTP on semiconductor process yield to enhance production outcomes.

- This includes perfecting RTP for ohmic contact in GaN HEMTs and using spike annealing for ultra-shallow junctions. Beyond traditional silicon, RTP systems for photovoltaic cell efficiency are gaining traction, with some innovations leading to a 5% increase in energy conversion over conventional methods. Similarly, low-temperature annealing for flexible electronics is opening new product categories.

- The complexity extends to managing thermal stress in 300mm wafers and perfecting RTP for high-k metal gate stacks. The evolution toward RTP in heterogeneous integration and chiplets underscores the need for real-time process control in RTP systems and advanced pyrometry for temperature uniformity. This ensures that RTP integration with ALD and CVD processes is seamless, enabling next-generation device fabrication.

What are the key market drivers leading to the rise in the adoption of Rapid Thermal Processing Equipment Industry?

- The aggressive scaling of semiconductor nodes to advanced levels is a primary driver for the market, demanding more precise and sophisticated thermal processing solutions.

- Market growth is fundamentally driven by aggressive semiconductor node scaling and the surging demand for AI accelerator production and high-performance computing clusters.

- This necessitates equipment capable of superior thermal process control to produce chips with high computational density and energy efficiency.

- The adoption of wide-bandgap semiconductors is another major driver, as materials like silicon carbide and gallium nitride are critical for electric vehicles and renewable energy inverters, enabling higher voltage operation and greater power conversion efficiency.

- This expands the market beyond traditional silicon, creating demand for specialized equipment that can reduce substrate bowing and optimize crystal quality.

- As data center hardware expands to support generative AI services, the need for reliable thermal processing to manufacture the underlying silicon with minimal variability intensifies, driving continuous innovation.

What are the market trends shaping the Rapid Thermal Processing Equipment Industry?

- Government initiatives aimed at bolstering domestic semiconductor fabrication are significantly expanding production capacity. This trend directly fuels demand for advanced manufacturing equipment.

- Key trends are reshaping the market, driven by government initiatives promoting semiconductor supply chain resilience and strategic foundry capacity expansion. These programs accelerate the adoption of advanced wafer fabrication equipment, including systems tailored for photovoltaic cell fabrication, which have demonstrated the ability to boost cell efficiencies beyond 23%.

- The proliferation of the IoT device fabrication ecosystem creates demand for high-throughput tools that enhance process window optimization. Equipment providers are responding with modular designs featuring real-time feedback, capable of reducing cycle times by up to 20%. This supports the production of 5G-enabled edge devices and smart infrastructure components, where controlled annealing is critical for performance and reliability.

- Technology transfer agreements are also facilitating market entry in emerging regions, broadening the global manufacturing footprint.

What challenges does the Rapid Thermal Processing Equipment Industry face during its growth?

- High capital and operational costs associated with acquiring and maintaining advanced manufacturing equipment present a significant challenge to market growth and expansion.

- Significant challenges constrain market growth, led by high capital and operational costs that limit fab automation software adoption and slow cost of ownership reduction. These expenses can deter smaller companies and strain budgets for larger firms, with new facilities in some regions costing up to 35% more than in established hubs.

- A critical shortage of skilled labor further hampers productivity, with one industry report projecting a need for one million additional workers globally. This talent gap delays project timelines and hinders the adoption of advanced techniques for power electronics manufacturing and other specialized fields.

- Supply chain disruptions, exacerbated by geopolitical tensions, add another layer of risk, impacting the availability of critical components and threatening equipment uptime improvement efforts, ultimately affecting everything from medical device electronics to aerospace and defense electronics.

Exclusive Technavio Analysis on Customer Landscape

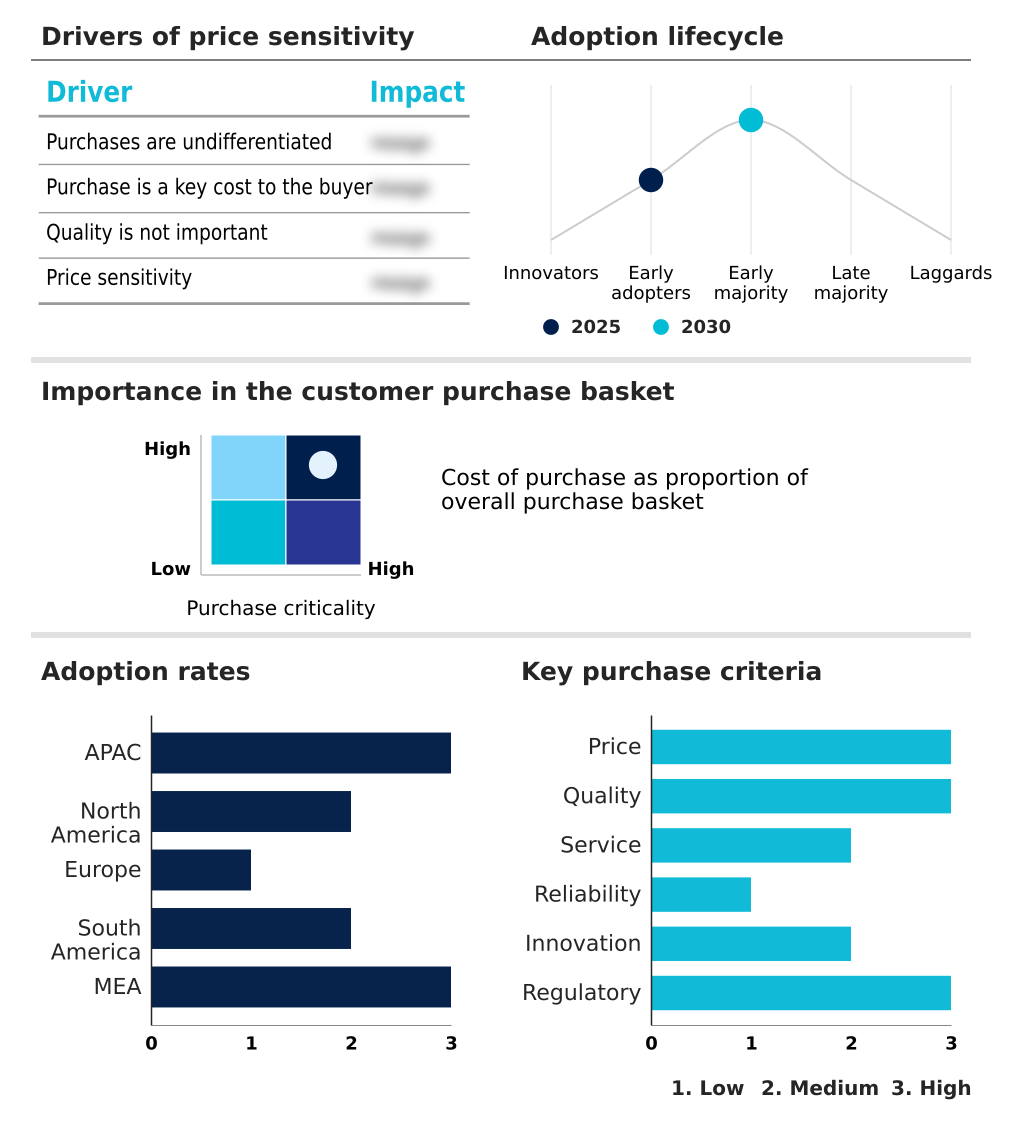

The rapid thermal processing equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the rapid thermal processing equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Rapid Thermal Processing Equipment Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, rapid thermal processing equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Allwin21 Corp. - Key offerings focus on advanced thermal processing systems delivering precise dopant activation and annealing, crucial for manufacturing next-generation semiconductors at scaled technology nodes.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Allwin21 Corp.

- AMETEK Inc.

- ANNEALSYS SAS

- Applied Materials Inc.

- centrotherm international AG

- CoorsTek Inc.

- CVD Equipment Corp.

- ECM Techologies

- JTEKT Thermo Systems Corp.

- KOKUSAI ELECTRIC CORP

- Levitech B.V.

- Mattson Technology Inc.

- Picotech Ltd

- PLASMA THERM

- SemiTEq JSC

- Tokyo Electron Ltd.

- UniTemp GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Rapid thermal processing equipment market

- In September 2024, the National Science Foundation allocated $42.4 million in grants to support semiconductor talent development and equipment research, indirectly boosting advancements in thermal processing for IoT device fabrication.

- In October 2024, KLA Corporation launched a specialized metrology tool designed to monitor thermal distribution within lamp-based chambers, enhancing process control for high-volume manufacturing.

- In January 2025, CVD Equipment Corp. announced an expansion of its thermal processing capabilities targeting high-power electronics, including systems for silicon carbide production relevant to rapid thermal applications.

- In February 2025, Intel advanced its Arizona fabrication operations with new capacity for eighteen-angstrom processes, integrating rapid thermal processing for critical transistor formation steps in high-performance logic chips.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Rapid Thermal Processing Equipment Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 287 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.8% |

| Market growth 2026-2030 | USD 336.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.5% |

| Key countries | China, Japan, South Korea, India, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, South Africa, Saudi Arabia, UAE, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The rapid thermal processing equipment market is evolving beyond simple heating, becoming a cornerstone of advanced semiconductor manufacturing processes. Its importance is magnified in the context of Moore's Law, where precise thermal budget control is non-negotiable for achieving high semiconductor yield enhancement at sub-five nanometer dimensions.

- Systems are engineered for exceptional thermal uniformity across three-hundred-millimeter wafers, utilizing both lamp-based heating and laser annealing systems. Critical applications include dopant activation, implant activation, and defect annealing, especially for silicon carbide processing and gallium nitride devices used in power electronics manufacturing.

- The industry is focused on developing gate-all-around architectures and advanced packaging solutions like heterogeneous integration, which require millisecond annealing and spike annealing technology to create ultra-shallow junction formation. Boardroom decisions are increasingly influenced by the need for EUV lithography compatibility and cluster tool integration, with some firms achieving a 20% reduction in cycle times through process module optimization.

- This involves wafer fabrication equipment capable of everything from wafer surface treatment to ohmic contact formation, supported by real-time metrology. The technology is also pivotal for 3D NAND fabrication, photovoltaic cell fabrication, and ensuring high-bandwidth memory production can meet the demands of AI. Techniques such as plasma-enhanced processing, atomic layer deposition, and chemical vapor deposition are now closely integrated.

What are the Key Data Covered in this Rapid Thermal Processing Equipment Market Research and Growth Report?

-

What is the expected growth of the Rapid Thermal Processing Equipment Market between 2026 and 2030?

-

USD 336.1 million, at a CAGR of 6.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Lamp-based, and Laser-based), Application (Industrial, and Research and development), Technology (Fully automated, Semi-automated, and Manual) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Aggressive scaling of semiconductor nodes to advanced levels, High capital and operational costs

-

-

Who are the major players in the Rapid Thermal Processing Equipment Market?

-

Allwin21 Corp., AMETEK Inc., ANNEALSYS SAS, Applied Materials Inc., centrotherm international AG, CoorsTek Inc., CVD Equipment Corp., ECM Techologies, JTEKT Thermo Systems Corp., KOKUSAI ELECTRIC CORP, Levitech B.V., Mattson Technology Inc., Picotech Ltd, PLASMA THERM, SemiTEq JSC, Tokyo Electron Ltd. and UniTemp GmbH

-

Market Research Insights

- The market is shaped by a dynamic interplay of technological innovation and operational demands. The push for semiconductor node scaling in AI accelerator production and data center hardware requires sophisticated thermal management, with some systems reducing cycle times by up to 20%.

- Simultaneously, the expansion of 5G-enabled edge devices and IoT device fabrication drives demand for equipment that supports high-mix production environments efficiently. In the renewable energy sector, specialized thermal processing for photovoltaic cell manufacturing has boosted cell efficiencies above 23%, underscoring the equipment's role in improving power conversion efficiency.

- This evolution highlights a market where equipment uptime improvement and process window optimization are key differentiators, influencing purchasing decisions across all segments from consumer electronics manufacturing to automotive semiconductor reliability.

We can help! Our analysts can customize this rapid thermal processing equipment market research report to meet your requirements.

RIA -

RIA -