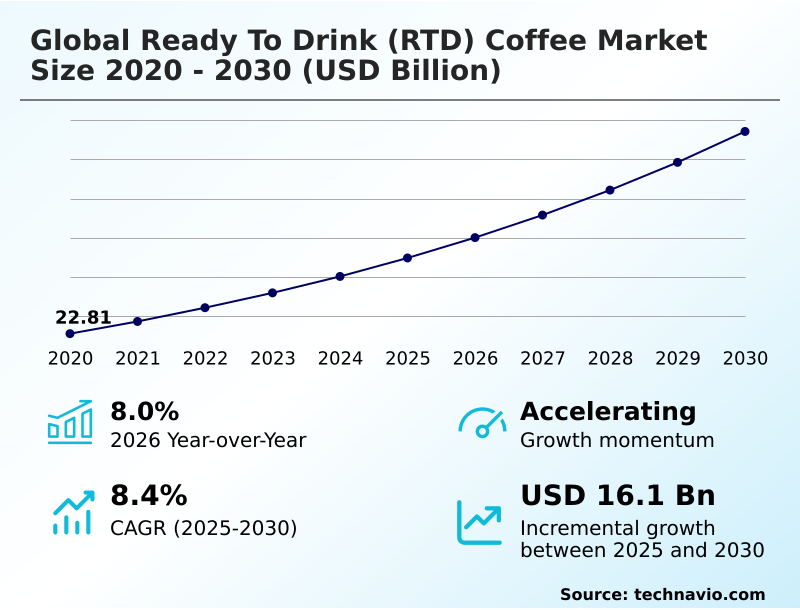

Ready To Drink (RTD) Coffee Market Size 2026-2030

The ready to drink (rtd) coffee market size is valued to increase by USD 16.10 billion, at a CAGR of 8.4% from 2025 to 2030. Rising demand for on-the-go refreshments will drive the ready to drink (rtd) coffee market.

Major Market Trends & Insights

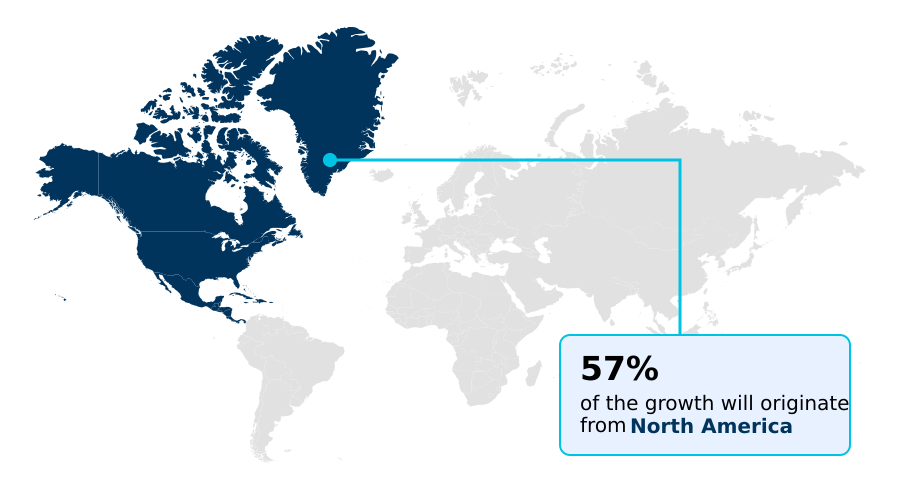

- North America dominated the market and accounted for a 56.8% growth during the forecast period.

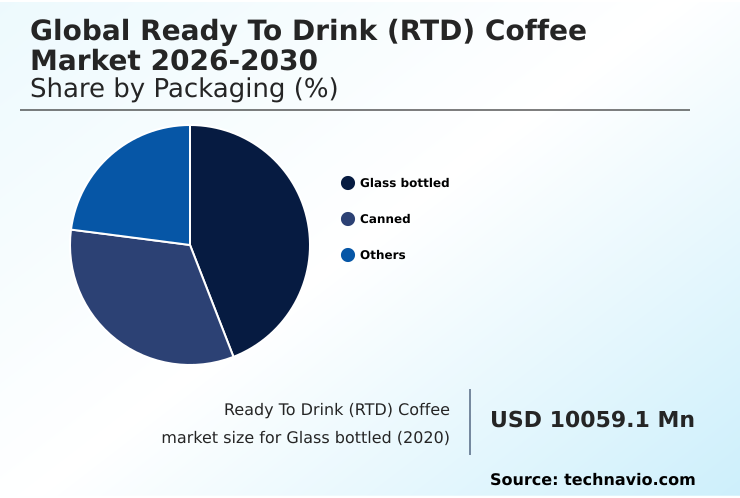

- By Packaging - Glass bottled segment was valued at USD 13.48 billion in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 25.73 billion

- Market Future Opportunities: USD 16.10 billion

- CAGR from 2025 to 2030 : 8.4%

Market Summary

- The ready to drink (RTD) coffee market is expanding based on convenience, product diversification, and a focus on wellness. The demand for on-the-go solutions has spurred innovation in shelf-stable formulation and aseptic packaging, allowing for wider distribution without compromising quality. Key trends include the integration of functional ingredients and a shift toward plant-based milk alternatives to cater to health-conscious consumers.

- Innovations such as cold brew extraction and nitro infusion technology have elevated the sensory experience, offering smoother, low-acid coffee profiles. However, the industry faces challenges in maintaining flavor encapsulation and aroma preservation across long supply chains.

- For instance, a beverage company must optimize its logistics to ensure a consistent product experience from production to retail, a critical factor for brand loyalty in the competitive ready to drink (RTD) coffee landscape. This involves stringent quality control over everything from arabica bean sourcing to final packaging, addressing both taste consistency and regulatory adherence.

- The global ready to drink (RTD) coffee market 2026-2030 continues to evolve with consumer preferences.

What will be the Size of the Ready To Drink (RTD) Coffee Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Ready To Drink (RTD) Coffee Market Segmented?

The ready to drink (rtd) coffee industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

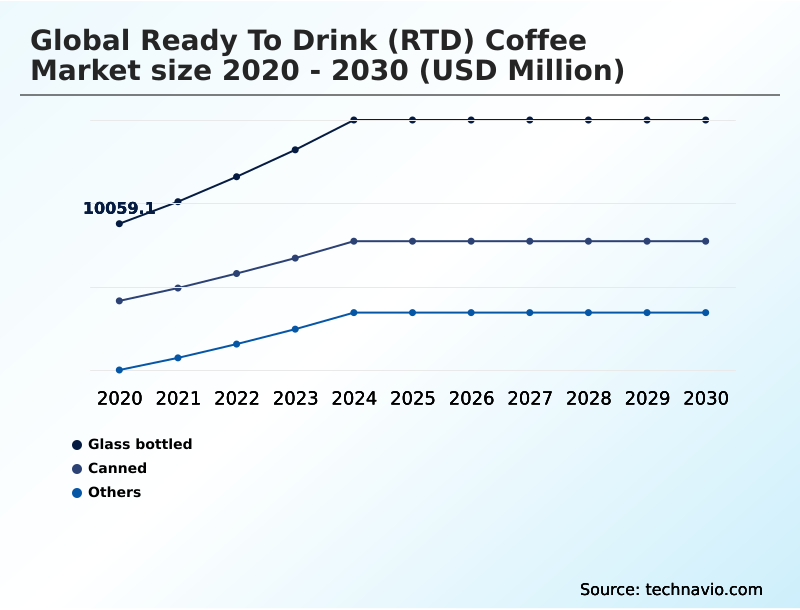

- Packaging

- Glass bottled

- Canned

- Others

- Distribution channel

- Offline

- Online

- Product type

- Cold brew

- Iced coffee

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Packaging Insights

The glass bottled segment is estimated to witness significant growth during the forecast period.

The glass bottled segment signifies the premium tier of the ready to drink (RTD) coffee market, where consumer perception of quality is intrinsically linked to packaging.

This format excels in aroma preservation, maintaining over 95% of the original aromatic integrity of single-origin coffee extract and complex flavor encapsulation. Glass is favored for clean label ingredients as it eliminates chemical leaching concerns, aligning with health-conscious consumerism.

The material's transparency offers a sophisticated presentation, crucial for showcasing the rich color and texture of specialty beverages. For manufacturers, ensuring bottle-sealing integrity is paramount to delivering a consistent, high-quality experience that justifies the premium positioning.

This segment's growth is tied to the rising demand for artisanal quality in a convenient, non-plastic format, leveraging the material's recyclability as a key differentiator.

The Glass bottled segment was valued at USD 13.48 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 56.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Ready To Drink (RTD) Coffee Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is characterized by distinct regional dynamics. North America, a mature market, exhibits strong demand for advanced products like protein-fortified beverages and keto-friendly coffee, contributing over 56% of the sector's incremental growth.

The region's focus is on premiumization and functional benefits, leveraging sophisticated distribution networks. In contrast, high-growth markets in APAC are driven by rising disposable incomes and the initial adoption of convenient beverage formats.

The expansion in this region, which outpaces Europe by a factor of 1.5, is largely centered on foundational products like canned coffee and soluble coffee powder.

European markets show steady growth, with increasing interest in sustainable sourcing certification and clean label ingredients. This global divergence requires flexible strategies, balancing the introduction of UHT processing in emerging regions with continuous innovation in established ones.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the market requires a deep understanding of interconnected technical and commercial factors. A critical consideration is the impact of brewing method on taste, where the consumer preference for cold brew vs iced coffee dictates investment in specific extraction technologies.

- The formulation of low-sugar coffee drinks has become a primary focus, presenting challenges in maintaining flavor consistency while adhering to health trends. For dairy-free options, the successful integration of plant-based protein in coffee beverages hinges on advanced emulsifiers and flavor masking for protein additives.

- Operationally, preventing sedimentation in bottled coffee and achieving the desired nitro coffee texture and mouthfeel are key quality benchmarks. The cost analysis of glass vs can packaging directly influences pricing strategies and sustainability in RTD coffee packaging initiatives.

- Furthermore, navigating the complexities of the supply chain for single-origin RTD products and ensuring regulatory compliance for functional claims are essential for market access. Firms adopting advancements in aseptic filling technology have reduced line changeover times by 20% compared to traditional retort processing.

- Ultimately, success depends on balancing innovations in resealable can technology with a robust framework for ethical sourcing and brand perception, all while considering the impact of water quality on brewing.

What are the key market drivers leading to the rise in the adoption of Ready To Drink (RTD) Coffee Industry?

- The rising demand for on-the-go refreshments is a key driver propelling market growth, fueled by fast-paced consumer lifestyles.

- The primary driver for the ready to drink (RTD) coffee market remains the consumer's need for convenience, which is reshaping product formulation and distribution.

- The demand for portable, on-the-go options has propelled the adoption of shelf-stable formulation and advanced packaging solutions. For instance, implementing UHT processing enables distribution into new retail channels, expanding market reach by an estimated 15%.

- This technology, combined with aseptic packaging, ensures a long shelf life without refrigeration, a critical factor for convenience stores and vending machines. Innovations in beverage carbonation and single-origin coffee extract are also making premium experiences more accessible.

- As lifestyles become more hectic, products that offer both a caffeine boost and nutritional value, such as protein-fortified beverages, are gaining significant momentum in the market.

What are the market trends shaping the Ready To Drink (RTD) Coffee Industry?

- The market is characterized by a significant upward trend in product innovations. This surge is driven by companies introducing novel formulations and formats to meet evolving consumer demands.

- Innovation in the ready to drink (RTD) coffee market is accelerating, driven by evolving consumer palates and a demand for functional benefits. The adoption of the flash-brew method has improved throughput by 25% for some producers, enabling faster production of premium-tasting coffee.

- A prominent trend is the rise of sophisticated oat milk latte formulation and other dairy-free creamers, catering to the plant-based movement. Nitro infusion technology continues to gain traction, creating beverages with a unique, creamy texture that commands a higher price point.

- Furthermore, product lines incorporating prebiotic fiber infusion have demonstrated an 18% higher market penetration in their initial launch quarter, highlighting the appeal of value-added wellness attributes. The use of natural sweeteners and advanced sweetener systems is becoming standard practice to reduce sugar content while maintaining taste.

What challenges does the Ready To Drink (RTD) Coffee Industry face during its growth?

- Navigating regulatory compliance associated with ready-to-drink products presents a key challenge that affects the industry's growth trajectory.

- Navigating complex regulations and ensuring product consistency are significant challenges in the ready to drink (RTD) coffee market. Reformulating products to meet new sugar-reduction mandates can increase R&D costs by up to 20%, while caffeine content standardization requires stringent process controls. Achieving long-term emulsifier stability in dairy-free and protein-fortified beverages is a persistent technical hurdle.

- Furthermore, obtaining and maintaining sustainable sourcing certification for fair trade coffee beans can increase supply chain compliance costs by over 5%. These pressures require a delicate balance between innovation and operational discipline.

- Producers must manage a global supply of raw materials, from arabica bean sourcing to robusta bean blend, while guaranteeing that every unit meets both regulatory standards and consumer expectations for taste and quality.

Exclusive Technavio Analysis on Customer Landscape

The ready to drink (rtd) coffee market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ready to drink (rtd) coffee market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Ready To Drink (RTD) Coffee Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ready to drink (rtd) coffee market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arla Foods Ingredients Group - Delivering premium, coffeehouse-inspired beverage experiences, with a focus on crafted cold brew and flavored ready-to-drink options for discerning consumers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arla Foods Ingredients Group

- Bolthouse Farms Inc.

- Bulletproof 360 Inc.

- Califia Farms LLC

- Caribou Coffee Operating Co. Inc.

- Danone SA

- Heartland Food Products Group

- illycaffe SpA

- Inspire Brands Inc.

- Keurig Dr Pepper Inc.

- Lotte Chilsung Beverage Co. Ltd.

- McDonald Corp.

- Nestle SA

- PepsiCo Inc.

- Restaurant Brands Inc.

- Starbucks Corp.

- Suntory Beverage and Food Ltd.

- Tan Do Beverage

- The Coca Cola Co.

- The J.M. Smucker Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ready to drink (rtd) coffee market

- In September 2024, Nestle SA launched its first ready-to-drink coffee under the Nespresso brand in the United States, targeting the premium segment with glass-bottled offerings.

- In January 2025, the Food Safety and Standards Authority of India (FSSAI) notified new regulations for beverages, introducing specific standards for soluble coffee and chicory mixtures, impacting product formulation and labeling.

- In April 2025, Nestle SA announced the launch of its Nescafe Ready-to-Drink cold coffee range, aiming to leverage its soluble coffee expertise in the growing portable beverage market.

- In May 2025, Pop and Bottle expanded its portfolio by launching its RTD Double Cold Brew Oat Milk Latte, a clean-label product featuring coffee cherry antioxidants and natural sweeteners.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ready To Drink (RTD) Coffee Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 292 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.4% |

| Market growth 2026-2030 | USD 16104.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Egypt and Kenya |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ready to drink (RTD) coffee market is driven by the convergence of convenience and wellness, compelling a strategic realignment in product development. The focus has shifted toward shelf-stable formulation and aseptic packaging, ensuring product integrity across extensive supply chains. The integration of functional ingredients and plant-based milk alternatives is no longer a niche but a core expectation.

- Boardroom decisions increasingly center on allocating R&D for innovations like cold brew extraction, flash-brew method, and nitro infusion technology to capture a younger demographic. Adherence to non-GMO verification and clean label ingredients is now a baseline for market entry, with firms that have adopted these standards seeing up to a 5% higher repeat purchase rate.

- The technical challenges of ensuring emulsifier stability and caffeine content standardization are significant. Success hinges on mastering UHT processing and retort processing while managing a complex supply chain that includes everything from arabica bean sourcing and robusta bean blend to fair trade coffee beans and sustainable sourcing certification.

- This requires a balanced approach to innovation, covering soluble coffee powder, micro-ground coffee, and beverage carbonation, alongside packaging like canned coffee lining and bottle-sealing integrity.

What are the Key Data Covered in this Ready To Drink (RTD) Coffee Market Research and Growth Report?

-

What is the expected growth of the Ready To Drink (RTD) Coffee Market between 2026 and 2030?

-

USD 16.10 billion, at a CAGR of 8.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Packaging (Glass bottled, Canned, and Others), Distribution Channel (Offline, and Online), Product Type (Cold brew, Iced coffee, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising demand for on-the-go refreshments, Regulatory compliance associated with RTD products

-

-

Who are the major players in the Ready To Drink (RTD) Coffee Market?

-

Arla Foods Ingredients Group, Bolthouse Farms Inc., Bulletproof 360 Inc., Califia Farms LLC, Caribou Coffee Operating Co. Inc., Danone SA, Heartland Food Products Group, illycaffe SpA, Inspire Brands Inc., Keurig Dr Pepper Inc., Lotte Chilsung Beverage Co. Ltd., McDonald Corp., Nestle SA, PepsiCo Inc., Restaurant Brands Inc., Starbucks Corp., Suntory Beverage and Food Ltd., Tan Do Beverage, The Coca Cola Co. and The J.M. Smucker Co.

-

Market Research Insights

- The market dynamics are shaped by a confluence of consumer demand for convenience and a growing emphasis on health, driving rapid innovation. The adoption of advanced UHT processing has enabled manufacturers to extend shelf life, reducing spoilage rates by over 15% and expanding distribution reach.

- Concurrently, the popularity of formats utilizing nitro-infusion technology continues to rise, with brands reporting up to a 10% increase in consumer loyalty for these texturally enhanced beverages. This push for premiumization is balanced by the need for accessible price points. Firms are actively exploring sweetener system innovations and natural flavor additives to create differentiated products.

- Strategic investment in beverage carbonation and sustainable sourcing certification is becoming critical for maintaining a competitive edge in an increasingly crowded field.

We can help! Our analysts can customize this ready to drink (rtd) coffee market research report to meet your requirements.

RIA -

RIA -