APAC Returnable Transport Packaging Market Size 2024-2028

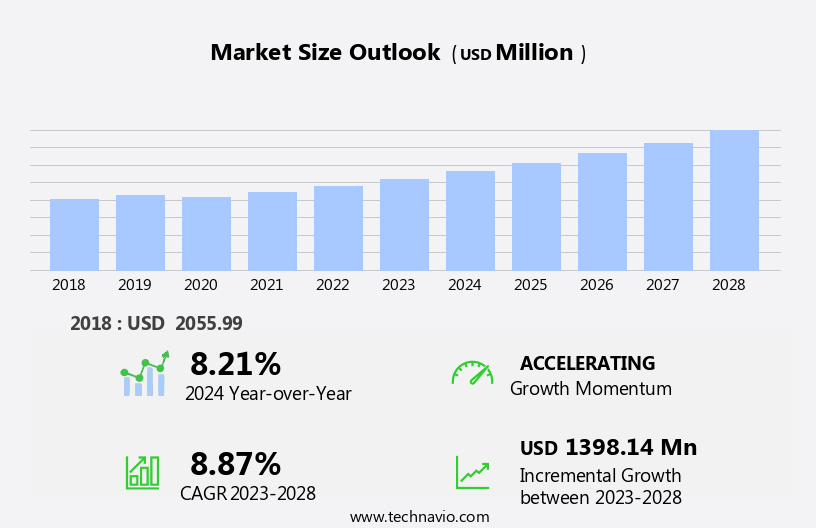

The APAC returnable transport packaging market size is forecast to increase by USD 1.4 billion at a CAGR of 8.87% between 2023 and 2028.

- In the Asia-Pacific (APAC) region, the returnable transport packaging (RTP) market is experiencing significant growth. Key factors driving this expansion include the long-term cost savings for buyers, who benefit from the reusability of RTP, and the burgeoning e-commerce sector. The e-commerce industry's rapid growth in APAC presents a substantial opportunity for RTP market growth, as the need for efficient and durable packaging solutions increases. Additionally, RTP offers advantages such as lower handling costs and reduced product damage, making it an attractive option for businesses in the region. Asset management and reverse logistics play a crucial role in the RTP market, ensuring the durability and standardization of reusable packaging. Overall, the combination of these factors is fueling the growth of the RTP market in APAC.

What will be the size of the APAC Returnable Transport Packaging Market during the forecast period?

- The Returnable Transport Packaging (RTP) market in the Asia Pacific (APAC) region is experiencing significant growth due to the increasing demand for sustainable logistics solutions in the transport, manufacturing, and distribution sectors. RTP, including pallets, containers, crates, totes, IBCs, drums, bins, and bulk containers, plays a crucial role in the circular economy by promoting reverse logistics and cost savings through reuse. The implementation of RFID technology for tracking and efficient management of RTP assets is a key trend driving market growth. The APAC region's vast manufacturing industry and the need for efficient distribution networks further boost the demand for RTP.

- Sustainability considerations are also a significant factor, as businesses seek to reduce their carbon footprint and minimize waste in the supply chain. The RTP market in APAC offers numerous opportunities for cost savings and improved efficiency. The use of reusable packaging reduces the need for constant procurement and disposal, leading to substantial cost savings. Additionally, the efficient management of RTP assets through RFID technology and reverse logistics initiatives can streamline operations and improve overall supply chain performance. Thus, the market is poised for continued growth due to the increasing demand for sustainable logistics solutions, the need for cost savings, and the implementation of RFID technology for efficient management of RTP assets.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Containers

- Pallets

- Drums and barrels

- Others

- End-user

- Food and beverage industry

- Manufacturing industry

- Retail industry

- Geography

- APAC

- China

- India

- Japan

- South Korea

- APAC

By Product Insights

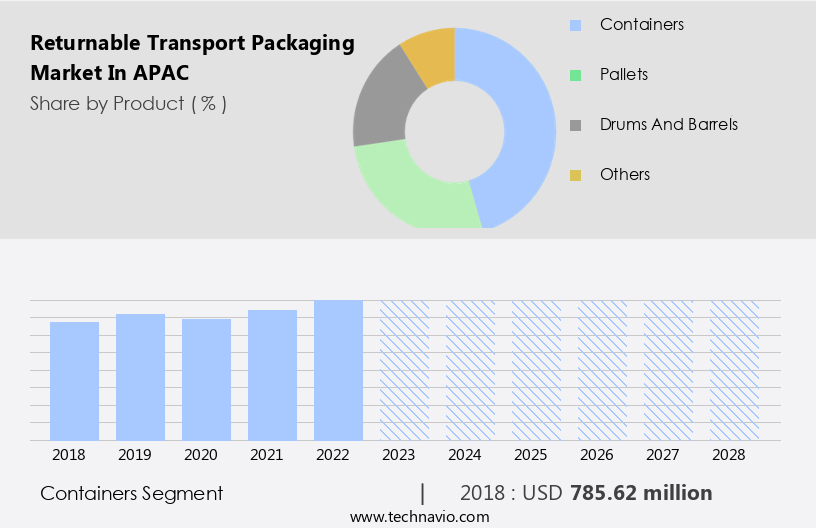

- The containers segment is estimated to witness significant growth during the forecast period. The Returnable Transport Packaging (RTP) market in APAC is primarily driven by the logistics and supply chain sectors, with a focus on sustainability and cost savings. Reusable packaging solutions, such as pallets, containers, crates, totes, IBCs, drums, and bins, are integral to the circular economy and reverse logistics processes. Bulk containers are commonly used in agriculture, manufacturing, and distribution industries for efficient handling and transportation. The use of RFID tracking and traceability systems enhances asset tracking and regulatory compliance.

- Sustainability is a key consideration, with plastic, metal, and wood packaging options offering varying benefits in terms of durability and environmental impact. The retail sector, particularly in countries like China and India with large e-commerce markets and growing middle classes, is a significant demand driver for RTP. The need for efficient and cost-effective packaging solutions in the context of increasing logistics and supply chain complexities is a major trend. Regulations governing packaging waste and green logistics are also influencing market growth. Overall, the RTP market in APAC is expected to continue its expansion, driven by the need for sustainable, cost-effective, and efficient packaging solutions in various industries.

Get a glance at the market share of various segments Request Free Sample

- The containers segment was valued at USD 785.62 million in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of APAC Returnable Transport Packaging Market?

- Long-term cost-saving opportunities for buyers is the key driver of the market. In the Asia Pacific (APAC) region, the market for returnable transport packaging (RTP) solutions has gained significant traction due to their numerous advantages in logistics and supply chain management. These solutions, which include pallets, containers, crates, totes, IBCs, drums, bins, and bulk containers, are primarily manufactured using lightweight materials, such as plastic, to reduce transportation costs. The increasing demand for RTP in developing countries, like India, where most transportation is done via road, is a result of their space-saving benefits during transit. The implementation of returnable transport packaging solutions contributes to sustainability by reducing packaging waste and promoting a circular economy. Asset management and reverse logistics play crucial roles in optimizing the use of these reusable packaging solutions. The long-term cost savings and efficiency gains from using RTP are substantial, with an average lifespan ranging between 15 and 20 years.

- The adoption of RTP is not only beneficial for manufacturing and distribution industries but also for sectors like agriculture. The use of RTP in various forms, such as pallets and totes, facilitates efficient handling and transportation. The integration of technologies like RFID, tracking, and traceability further enhances the asset tracking capabilities of RTP, ensuring regulatory compliance and standardization. RTP solutions are available for rental or pooling, offering flexibility to businesses while minimizing their capital investment. The materials used in RTP manufacturing can vary, with plastic, metal, and wood being common choices. The durability and strength of these materials ensure that RTP can withstand the rigors of transportation and handling. The shift towards green logistics and the growing emphasis on sustainability have further fueled the demand for RTP in the APAC region. The regulations governing the use of packaging materials are becoming increasingly stringent, making RTP an attractive alternative to disposable packaging. The adoption of RTP is expected to continue its upward trend during the forecast period, offering substantial cost savings and efficiency gains to businesses.

What are the market trends shaping the APAC Returnable Transport Packaging Market?

- Increased adoption of returnable transport packaging is the upcoming trend in the market. In the Asia Pacific (APAC) region, the market for Returnable Transport Packaging (RTP) is experiencing significant growth due to various factors. Sustainability is a primary driver, as RTP solutions, including pallets, containers, crates, totes, IBCs, drums, and bins, contribute to the circular economy by reducing packaging waste. Compared to disposable packaging, RTP emits 28%-30% less carbon dioxide, making it an eco-friendly choice for logistics and supply chain operations. RTP offers cost savings through asset management and reverse logistics. The initial investment is higher, but the repeated use of these assets results in long-term efficiency and cost savings. RTP is more durable and stable than disposable packaging, minimizing the risk of damage during handling and transportation.

- RTP is essential in industries such as agriculture, manufacturing, and distribution, where bulk containers and pallets are commonly used. The use of RTP aligns with the principles of green logistics, promoting a more sustainable approach to logistics and supply chain operations. RTP comes in various materials, including plastic, metal, and wood, catering to different handling and transportation requirements. The standardization and regulations surrounding RTP ensure consistent quality and safety. RTP solutions, such as pallets and containers, can be rented or pooled, providing flexibility for businesses. Advancements in technology, such as RFID and tracking, enable better asset tracking and traceability, enhancing the overall efficiency and effectiveness of RTP in the APAC market.

What challenges does APAC Returnable Transport Packaging Market face during the growth?

- Fluctuating raw material prices is a key challenge affecting the market growth. In the dynamic returnable transport packaging (RTP) market in Asia Pacific, the use of sustainable packaging solutions, such as reusable pallets, containers, crates, totes, IBCs, drums, and bins, is a significant trend. These packaging solutions are essential for efficient logistics and supply chain operations, particularly in sectors like agriculture, manufacturing, and distribution. The primary raw materials for RTP production are plastic and metal, with plastic accounting for a substantial market share due to its durability, standardization, and ease of handling. However, the cost of raw materials, particularly plastic, is a critical challenge due to the volatility of crude oil prices and high demand from export-centric industries.

- This price instability can impact the overall cost savings and efficiency of RTP asset management and reverse logistics in the circular economy. Sustainability is a key focus in the RTP industry, with regulations promoting green logistics and the reduction of packaging waste. RFID tracking and traceability systems ensure optimal asset tracking and efficient handling during transportation. Wood is another material used in RTP production, offering advantages in terms of cost and environmental sustainability. Regulations and standardization are crucial factors in the RTP market, ensuring the safe and effective use of these packaging solutions in various industries.

Exclusive APAC Returnable Transport Packaging Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, market growth and forecasting, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amatech Inc.

- Balmer Lawrie and Co. Ltd.

- Berry Global Inc.

- Brambles Ltd.

- Bulk Lift International LLC

- BWAY Corp.

- CABKA Group GmbH

- CORDSTRAP BV

- Craemer GmbH

- DS Smith Plc

- Greif Inc.

- IFCO SYSTEMS GmbH

- Myers Industries Inc.

- Rehrig Pacific Co.

- Schoeller Allibert Services B.V.

- SCHUTZ GmbH and Co. KGaA

- Tank Holding Corp.

- The Supreme Industries Ltd.

- Time Technoplast Ltd.

- TranPak Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The Returnable Transport Packaging (RTP) market in APAC is a significant sector, encompassing various logistics and supply chain applications. This market caters to the demand for sustainable and cost-effective packaging solutions in industries such as automotive, electronics, pharmaceuticals, and food and beverage. Key players in this market include those that manufacture and supply RTP solutions, such as pallets, containers, and reusable bulk containers. These companies prioritize innovation and technology to create durable and lightweight packaging solutions. The market is driven by factors like increasing globalization, the growing e-commerce industry, and the need for efficient and sustainable supply chain solutions.

Additionally, governments in the APAC region are implementing regulations to reduce waste and promote the use of reusable packaging. The RTP market in APAC is expected to grow at a steady pace due to the increasing demand for just-in-time delivery and the need for efficient and cost-effective logistics solutions. The market is also influenced by factors like the rising trend of automation in manufacturing and the increasing adoption of Industry 4.0 technologies. Thus, the market is a dynamic and growing sector, driven by various factors and applications. Companies in this market focus on innovation and sustainability to cater to the evolving needs of industries and consumers.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

156 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.87% |

|

Market growth 2024-2028 |

USD 1.4 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.21 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -