Rosacea Treatment Market Size 2024-2028

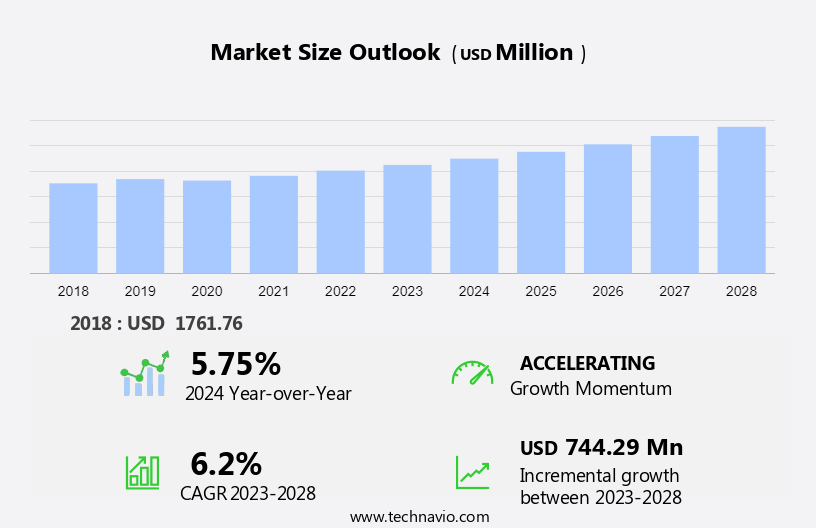

The rosacea treatment market size is forecast to increase by USD 744.29 million, at a CAGR of 6.2% between 2023 and 2028.

- Rosacea, a chronic inflammatory skin condition, is gaining significant attention due to the rising prevalence and increasing awareness of the disease. The market is witnessing notable growth, driven by several factors. One of the primary trends is the growing focus on personalized treatment approaches, with the integration of telemedicine and digital technologies enabling remote consultations and customized treatment plans. Another trend is the increasing demand for cosmetic procedures to manage the symptoms and improve the appearance of the skin.

- However, concerns regarding side effects and safety issues related to certain treatments, such as antibiotics and immunosuppressants, are challenging the market's growth. Additionally, the exploration of alternative therapies, like light therapy and blood-derived treatments from companies like Lupin, is providing new opportunities for market expansion. Overall, the market is expected to witness steady growth, with a focus on developing safe, effective, and personalized treatment options.

What will be the Size of the Rosacea Treatment Market During the Forecast Period?

- The market encompasses a range of solutions designed to address the symptoms and progression of rosacea, a common skin condition characterized by facial redness, inflammation, and the presence of papulopustular bumps, resembling acne. Rosacea can also lead to visible blood vessels, ocular rosacea, and phymatous changes. The market caters to both first-line therapy and other treatment types, including topical agents, antibiotics, oral medications, and light therapies. Topical treatments offer antimicrobial effects and are often used for mild to moderate rosacea, while systemic exposure to antibiotics is typically reserved for more severe cases. Laser and light therapies are effective in reducing inflammation and improving the appearance of visible blood vessels.

- The market's growth is influenced by the increasing prevalence of rosacea, particularly among fair-skinned individuals, and the rising geriatric population. Rosacea can lead to significant social and psychological distress, making early diagnosis and effective treatment crucial. Despite advancements in treatment options, challenges remain due to the complex nature of rosacea and the potential side effects associated with certain treatments. Other treatment types, such as sol-gel technologies, continue to emerge, offering new possibilities for managing this chronic condition.

How is this Rosacea Treatment Industry segmented and which is the largest segment?

The rosacea treatment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Distribution Channel

- Hospital pharmacies

- Retail pharmacies

- Online pharmacies

- Route Of Administration

- Topical

- Oral

- Injectable

- Geography

- North America

- US

- Europe

- Germany

- UK

- Asia

- China

- Rest of World (ROW)

- North America

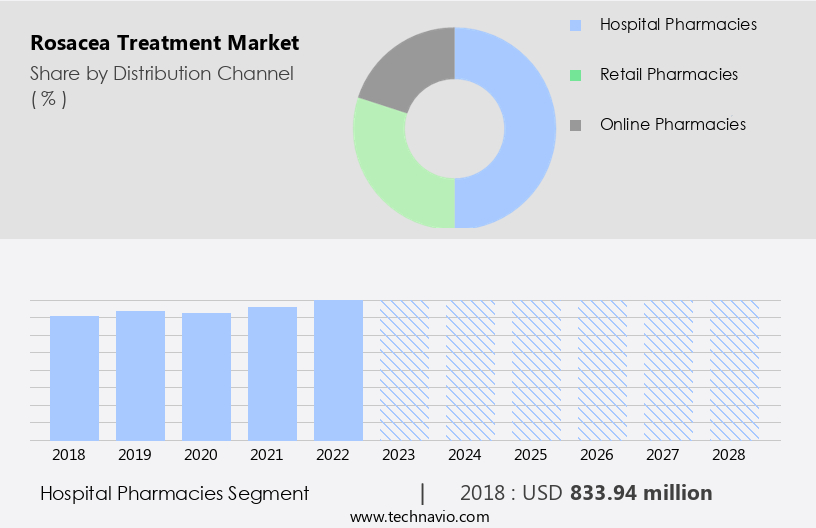

By Distribution Channel Insights

- The hospital pharmacies segment is estimated to witness significant growth during the forecast period.

Rosacea, an inflammatory skin condition, is characterized by symptoms such as facial redness, papules, pustules, and visible blood vessels. Topical treatments are a primary option for managing rosacea, offering targeted relief for these symptoms. Metronidazole gel or cream, with antimicrobial and anti-inflammatory properties, is commonly prescribed. It reduces redness and inflammation while targeting bacteria. Azelaic acid, another topical agent, normalizes skin cell turnover and reduces papules and pustules through its anti-inflammatory effects. Diagnosis often involves fair-skinned individuals presenting with flushing, erythematotelangiectatic rosacea, or papulopustular rosacea. Rosacea can affect various areas including the nose, cheeks, forehead, chest, ears, and back. Triggers such as heat, caffeine, stress, and mask-wearing can exacerbate symptoms.

The market has seen growth during the pandemic period due to increased healthcare professional consultations and the availability of digital healthcare service like telemedicine and remote consultations. Topical treatments, oral medications, and laser therapies are common treatment types, each with unique benefits and potential side effects. Strict regulations and regulatory hurdles impact market growth, with novel oral drugs and laser technology offering potential advancements. The prevalence of rosacea among the population aged 40-59 is significant, particularly In the rising geriatric population. Combination therapy and individualized treatment plans are essential for effective management.

Get a glance at the Rosacea Treatment Industry report of share of various segments Request Free Sample

The hospital pharmacies segment was valued at USD 833.94 million in 2018 and showed a gradual increase during the forecast period.

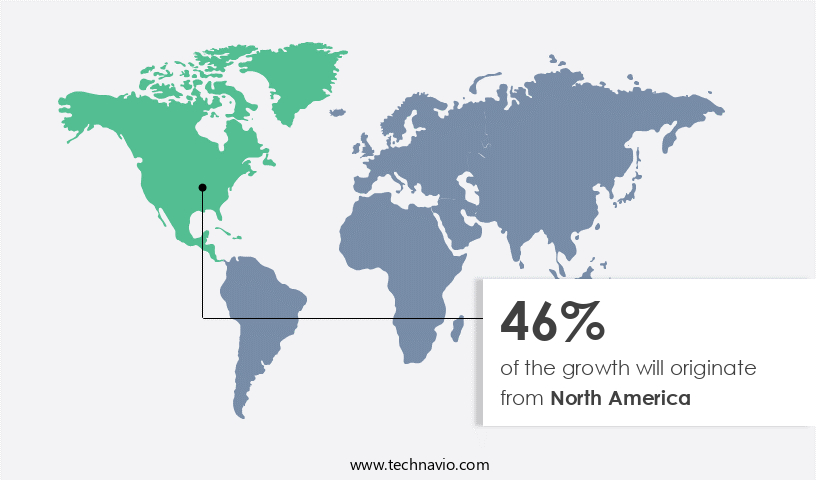

Regional Analysis

- North America is estimated to contribute 46% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American market is experiencing notable expansion due to the rising prevalence of chronic skin disorders, particularly among the geriatric population. Rosacea, an inflammatory skin condition characterized by symptoms such as facial redness, papulopustular bumps, and visible blood vessels, affects an estimated 16 million Americans aged 18 and above. Early diagnosis and treatment are crucial for managing rosacea symptoms, which can be triggered by factors like heat, stress, caffeine, and certain foods. Treatment options include topical agents, such as alpha agonists, retinoids, and corticosteroids, and oral medications, like antibiotics and immunosuppressants. Laser therapies and light treatments offer antimicrobial effects and help reduce inflammation and flare-ups.

Market growth is influenced by the increasing healthcare expenditure and the availability of digital healthcare solutions, such as telemedicine and remote consultations, enabling easier access to rosacea treatment for patients. However, regulatory hurdles and safety concerns related to medications and treatment discontinuation due to side effects pose challenges to the market. Key players In the market include Galderma, which caters to rosacea patients through a range of treatment options and innovative solutions.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Rosacea Treatment Industry?

Growing focus on personalized treatment approaches is the key driver of the market.

- The market experiences growth due to the personalized approach to managing this inflammatory skin condition. Rosacea affects individuals differently, with various triggers, symptoms, and treatment responses. Dermatologists now focus on customized treatment plans based on diagnostic tools, patient history assessments, and biomarker analysis. Identifying individual triggers, such as heat, stress, caffeine, or mask-wearings, is crucial for effective treatment. Rosacea presents with symptoms like facial redness, papulopustular bumps, and visible blood vessels. Early diagnosis and treatment are essential to prevent progression and potential complications, such as ocular rosacea. Personalized treatment options include topical agents like alpha agonists, retinoids, and corticosteroids, as well as oral medications and laser therapies.

- Topical treatments are often the first-line therapy for mild to moderate rosacea, while oral medications may be necessary for more severe cases. Light therapies, such as photodynamic therapy, offer antimicrobial effects and help reduce inflammation. Systemic exposure to these treatments should be monitored closely due to potential side effects and safety concerns. The prevalence of rosacea increases with age, particularly in fair-skinned individuals. The rising geriatric population and the availability of digital healthcare solutions, like telemedicine and remote consultations, facilitate better access to rosacea treatment. Technological advancements introduce novel oral drugs and laser technology, while combination therapy and individualized treatment plans further enhance treatment efficacy.

What are the market trends shaping the Rosacea Treatment Industry?

Rising demand for cosmetic procedures is the upcoming market trend.

- The market experiences growth due to the increasing demand for effective solutions to manage the symptoms of this inflammatory skin condition. Rosacea, which affects fair-skinned individuals, presents with signs and symptoms such as facial redness, flushing, papulopustular bumps, and visible blood vessels. These symptoms can lead to significant distress and impact self-confidence. First-line therapy for rosacea typically involves topical treatments, including antibiotics, alpha agonists, retinoids, and corticosteroids. However, for moderate to severe cases, laser therapies, such as vascular lasers and intense pulsed light (IPL) therapy, offer antimicrobial effects and target the underlying inflammation. Oral medications, including tetracyclines and isotretinoin, may be prescribed for more extensive cases.

- Rosacea can affect various areas of the body, including the nose, cheeks, forehead, chest, ears, and back. Triggers, such as heat, caffeine, stress, and mask-wearing, can exacerbate symptoms and lead to flare-ups. Other treatment types, such as topical agents, oral medications, and light therapies, may be used in combination for individualized treatment plans. The prevalence of rosacea increases with age, particularly In the geriatric population. Technological advancements in telemedicine and digital healthcare solutions enable remote consultations, follow-ups, monitoring, and monitoring, making rosacea treatment more accessible. However, strict regulations and regulatory hurdles, including authorization and safety concerns, may impact the market's growth.

What challenges does the Rosacea Treatment Industry face during its growth?

Side effects and safety concerns related to rosacea treatments is a key challenge affecting the industry growth.

- Rosacea, an inflammatory skin condition characterized by facial redness, visible blood vessels, and acne-like bumps, affects millions worldwide. Early diagnosis and appropriate treatment are crucial for managing symptoms and preventing progression to more severe stages like papulopustular rosacea and phymatous rosacea. Various treatment options exist, including topical agents, laser therapies, and oral medications. Topical treatments, such as antibiotics, alpha agonists, retinoids, and corticosteroids, offer antimicrobial effects and reduce inflammation. However, they may cause side effects like dryness, irritation, and hypersensitivity reactions, which can impact patient adherence and market growth. Systemic exposure to these medications can lead to side effects like flare-ups, mask-wearing, and heat or stress-induced exacerbations.

- Laser therapies, such as intense pulsed light and vascular lasers, provide long-term improvement but may carry risks like scarring and pigmentation changes. Oral medications, including tetracyclines and isotretinoin, offer more potent anti-inflammatory effects but can have significant side effects, including gastrointestinal issues, sun sensitivity, and potential birth defects. Safety concerns and regulatory hurdles associated with these treatments can also hinder market expansion. In the pandemic period, telemedicine and digital healthcare solutions have emerged as viable alternatives for rosacea patients, enabling remote consultations, follow-ups, monitoring, and technological advancements like novel oral drugs and combination therapies. The prevalence of rosacea among fair-skinned individuals and the rising geriatric population further fuel the demand for effective and safe rosacea treatments.

Exclusive Customer Landscape

The rosacea treatment market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the rosacea treatment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, rosacea treatment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Aclaris Therapeutics Inc.

- AKUMS

- Bausch Health Companies Inc.

- Croda International Plc

- Dermata Therapeutics Inc.

- Galderma SA

- Glenmark Pharmaceuticals Ltd.

- Hovione

- Journey Medical Corp.

- LEO Pharma AS

- Lupin Ltd.

- Maruho Co. Ltd.

- Mayne Pharma Group Ltd.

- Pfizer Inc.

- PruGen LLC

- Sol-Gel Technologies Ltd.

- Taro Pharmaceutical Industries Ltd.

- Teva Pharmaceutical Industries Ltd.

- Zydus Lifesciences Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Rosacea is an inflammatory skin condition characterized by facial redness, visible blood vessels, and acne-like bumps. The condition can manifest in various forms, including papulopustular rosacea, phymatous rosacea, and ocular rosacea. Rosacea affects individuals regardless of age or gender, but fair-skinned people are more susceptible. The market has experienced significant growth during the pandemic period due to increased awareness and the need for alternative treatment options. Systemic exposure to various triggers such as heat, stress, caffeine, and certain foods can exacerbate rosacea symptoms, leading to frequent flare-ups. The early diagnosis and treatment of rosacea are crucial to prevent progression and reduce the severity of symptoms.

Topical treatments, including alpha agonists, retinoids, and corticosteroids, are commonly used as first-line therapy for mild to moderate rosacea. These topical agents help reduce inflammation and improve the appearance of visible blood vessels. Light therapies, such as laser and intense pulsed light (IPL), are also effective in treating rosacea. These therapies offer antimicrobial effects and help reduce inflammation and redness. However, they require professional administration and can have side effects such as skin irritation and discoloration. Oral medications, including antibiotics and immunosuppressants, are used for more severe cases of rosacea. These medications can have significant side effects and require strict regulations and authorization for use.

Further, the market for rosacea treatments is diverse, with various treatment types and modes of administration. Topical preparations, oral medications, and light therapies are the most common treatment modalities. The use of telemedicine and digital healthcare solutions has become increasingly popular, allowing for remote consultations, follow-ups, and monitoring. Technological advancements have led to the development of novel oral drugs and laser technology, providing new treatment options for rosacea patients. However, safety concerns and adverse effects remain a significant challenge for the market. The prevalence of rosacea is increasing due to various factors, including the rising geriatric population and the use of masks, which can cause heat and friction on the skin.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

170 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.2% |

|

Market Growth 2024-2028 |

USD 744.29 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.75 |

|

Key countries |

US, Germany, UK, Russia, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Rosacea Treatment Market Research and Growth Report?

- CAGR of the Rosacea Treatment industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the rosacea treatment market growth of industry companies

We can help! Our analysts can customize this rosacea treatment market research report to meet your requirements.

RIA -

RIA -