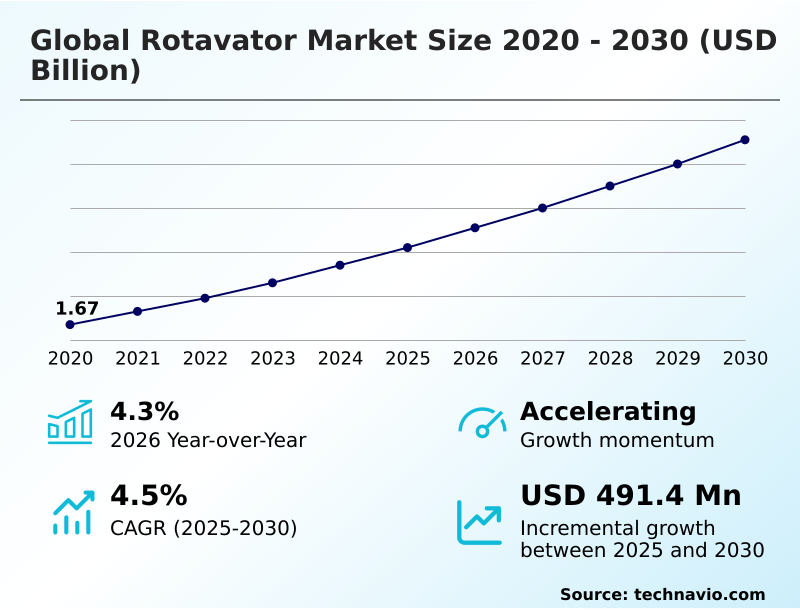

Rotavator Market Size 2026-2030

The rotavator market size is valued to increase by USD 491.4 million, at a CAGR of 4.5% from 2025 to 2030. Growing need for nutrient protection in agriculture fields will drive the rotavator market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 55.5% growth during the forecast period.

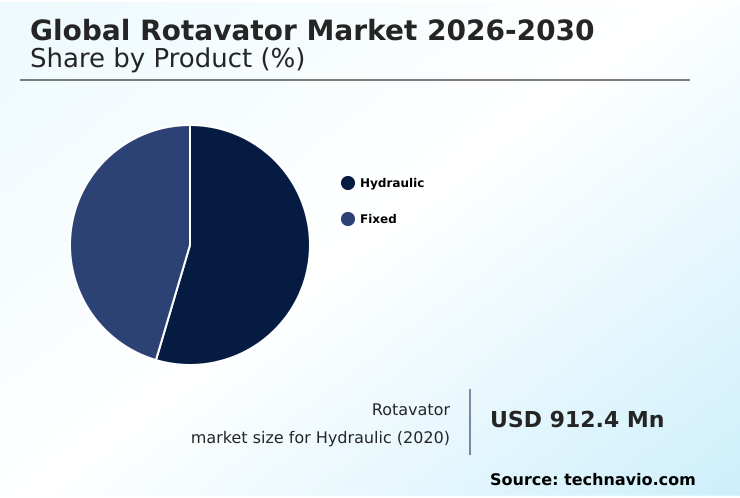

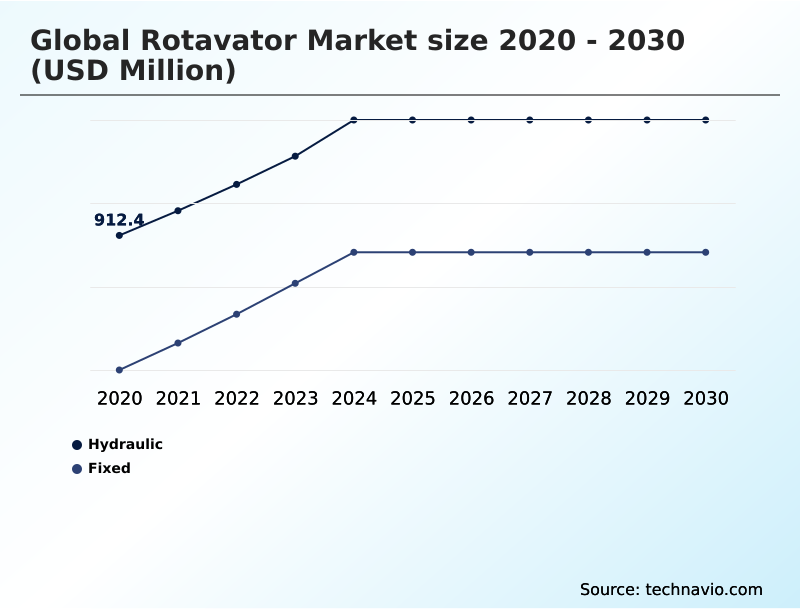

- By Product - Hydraulic segment was valued at USD 1.04 billion in 2024

- By Type - L type segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 838.7 million

- Market Future Opportunities: USD 491.4 million

- CAGR from 2025 to 2030 : 4.5%

Market Summary

- The rotavator market is fundamentally shaped by the global shift toward intensive farm mechanization and operational efficiency. As a tractor-mounted implement, the rotary tiller is critical for modern seedbed preparation, offering a single-pass tillage solution that significantly reduces time and fuel consumption compared to traditional methods.

- Key drivers include the need for effective crop residue incorporation and improved soil conditioning, which are vital for sustainable agriculture. The market is also seeing a trend toward automated features, such as automated depth adjustment and multi-speed gearbox options, which enhance precision and ease of use.

- For instance, a farming cooperative can leverage rotavators to shorten the turnaround time between harvesting one crop and sowing the next, effectively enabling an additional cropping cycle and boosting annual profitability. This is achieved by optimizing soil pulverization and aeration via the power take-off (PTO).

- However, the market faces challenges from the availability of alternative secondary tillage equipment and the high initial investment cost, which can be a barrier for smaller farming operations.

What will be the Size of the Rotavator Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Rotavator Market Segmented?

The rotavator industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Hydraulic

- Fixed

- Type

- L type

- C type

- Application

- Seedbed preparation

- Soil conditioning

- Crop residue management

- Horticulture

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- APAC

By Product Insights

The hydraulic segment is estimated to witness significant growth during the forecast period.

The hydraulic segment is integral to the rotavator market, addressing the demands of precision agriculture.

This technology, featuring a hydraulic offset, allows the tractor-mounted implement to perform inter-row cultivation with high accuracy, which is essential for vineyard cultivation and orchard floor management.

The design incorporates a side-shift mechanism for effective tillage depth control in hard-to-reach areas, reducing the need for manual labor. This capability not only supports sustainable farming by minimizing chemical use but also boosts productivity.

Adopting this tractor-implement system has been shown to enhance operational uptime by over 15% by preventing crop and equipment damage. The focus on specialized horticulture tillage makes this segment a key area of innovation and market value.

The Hydraulic segment was valued at USD 1.04 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 55.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Rotavator Market Demand is Rising in APAC Request Free Sample

The geographic landscape of the rotavator market is led by the APAC region, which accounts for over 55% of the incremental growth.

This dominance is fueled by government-backed farm mechanization initiatives in agricultural powerhouses like India and China, where the technology is essential for both wetland cultivation and dry-land farming.

In contrast, the North America market, contributing approximately 19% of growth, is characterized by demand for specialized implements used in high-value sectors such as vineyard cultivation and horticulture tillage.

The adoption of tractor-mounted implements is accelerating globally, driven by the need for efficient puddling operations and soil aeration.

Differences in tractor compatibility and regional soil types influence the demand for specific blade configurations and implement sizes across these key markets.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Optimizing agricultural productivity hinges on selecting the right equipment, making the choice between a hydraulic offset rotavator for vineyards and a heavy-duty rotavator for sugarcane residue a critical operational decision. The debate over L-type vs C-type rotavator blades is central to performance, directly influencing rotavator maintenance for blade longevity and the overall impact of rotavator on soil health.

- Modern implements offer cost-saving features in modern rotavators, with automated depth control in rotary tillers ensuring precise single pass tillage with rotavator. This automation can improve crop emergence uniformity by more than 10% compared to manually operated systems. When evaluating rotavator vs power tiller efficiency, factors such as fuel consumption and time savings become paramount.

- Furthermore, choosing rotavator for tractor horsepower ensures the entire system operates at peak efficiency. These implements are also increasingly used for mechanical weed control in organic farming. In specialized applications like rotavator for wetland paddy cultivation and general rotavator application in horticulture, the correct implement configuration is key to maximizing yield and adhering to certified rotavator safety standards.

What are the key market drivers leading to the rise in the adoption of Rotavator Industry?

- The increasing requirement for effective nutrient protection in agricultural fields to improve soil health and crop productivity is a primary driver for market growth.

- A primary market driver is the intensified focus on nutrient management and sustainable soil health.

- Rotavators enable effective crop residue incorporation and nutrient mixing, practices that improve soil conditioning and can increase nutrient availability by up to 20% compared to some zero-tillage alternatives.

- The consistent demand for high-quality seedbed preparation for both wetland cultivation and dry-land farming continues to fuel adoption.

- Concurrently, the increasing preference for implements with certified safety guards and an ISO-certified design is a significant driver, enhancing operator confidence and reducing operational risk.

- Efficient puddling operations in rice farming, facilitated by optimized rotary tiller blades powered by the power take-off (PTO), directly support the overarching goal of boosting agricultural productivity through better soil aeration and stubble management.

What are the market trends shaping the Rotavator Industry?

- The increasing global emphasis on agricultural mechanization is a significant trend, driving the adoption of efficient farm implements to enhance productivity and operational speed.

- Key market trends revolve around the integration of automation and cost-saving features into modern agricultural implements. The influx of automated depth adjustment and side-shift mechanism technologies is enhancing precision, particularly in horticulture tillage and orchard floor management. This level of farm mechanization improves fuel consumption efficiency by approximately 10-15% by optimizing the tractor horsepower requirement.

- Another significant trend is the focus on implement durability, with advanced wear-resistant blades and robust gearboxes extending the operational life of a tractor-implement system by up to 25%. This reduces long-term maintenance costs and minimizes operational time reduction.

- Ensuring tractor compatibility remains a priority for manufacturers, as seamless integration is crucial for maximizing the benefits of these advanced primary tillage tools and improving overall soil tilth.

What challenges does the Rotavator Industry face during its growth?

- The growing availability of and threat from substitute tillage products presents a significant challenge to the market's growth trajectory.

- A significant market challenge is the rising threat from substitute products, such as vertical tillage machines, which are often promoted as superior conservation tillage methods that prevent hard pan formation and can reduce surface compaction by 15% under certain conditions.

- Another headwind is the growing end-user preference for rental or pre-owned equipment, a trend that can suppress new unit sales by 10-20% in some regions by altering considerations around initial investment versus long-term maintenance costs.

- The recurring expense associated with the frequent replacement of rotary tiller blades, a necessary part of secondary tillage and topsoil manipulation, remains a barrier for many small-scale farmers. This issue influences purchasing decisions regarding the durability of components like the heavy-duty gearcase and the choice between L-type blades and C-type blades on any new agricultural implement.

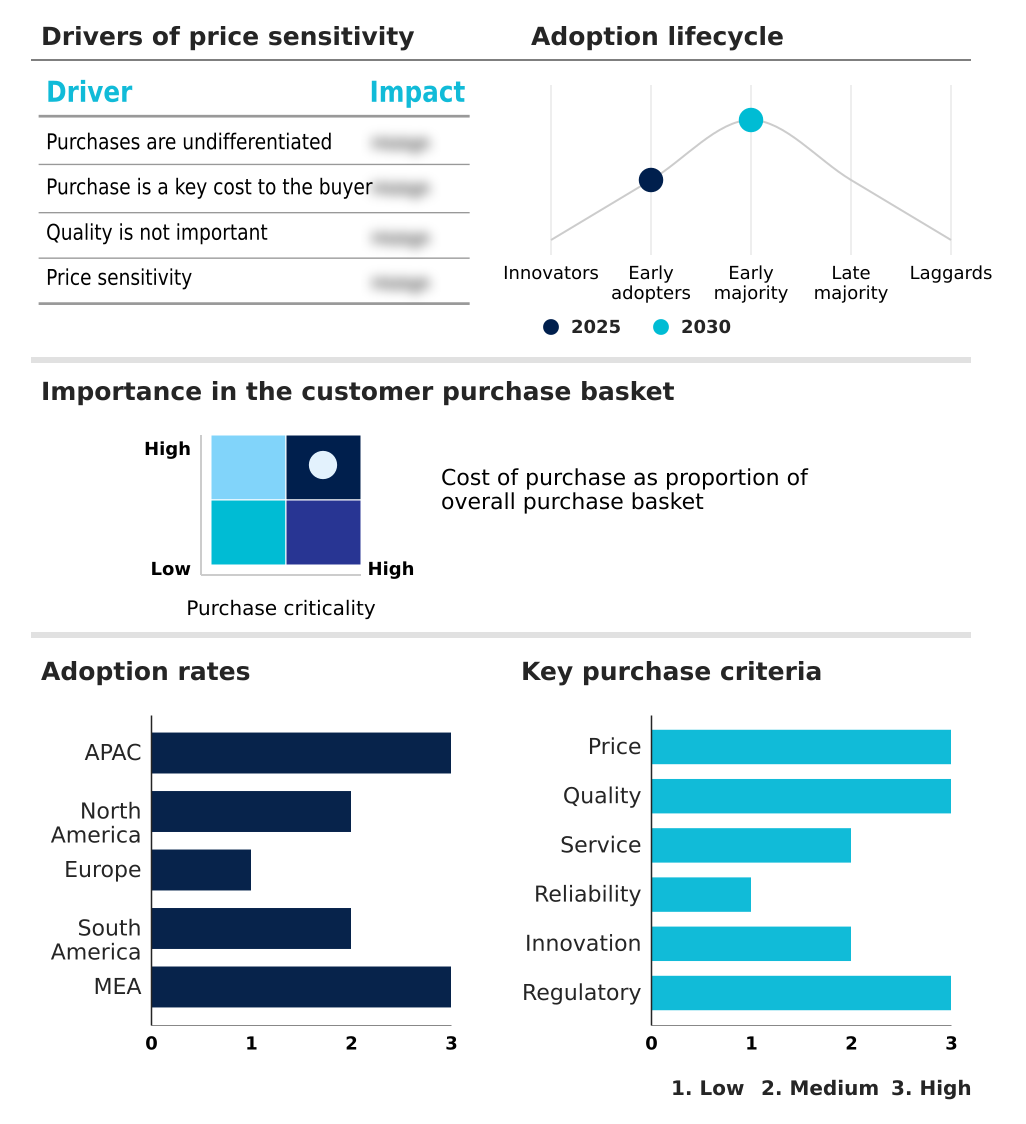

Exclusive Technavio Analysis on Customer Landscape

The rotavator market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the rotavator market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Rotavator Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, rotavator market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Action Construction Equipment Ltd. - A key portfolio includes advanced agricultural implements, featuring rotavators with hydraulic and multi-speed capabilities designed for enhanced operational efficiency in modern farming.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Action Construction Equipment Ltd.

- AGCO Corp.

- Beri Udyog Pvt. Ltd.

- CLAAS KGaA

- CNH Industrial NV

- Deere and Co.

- Greaves Cotton Ltd.

- Kubota Corp.

- KUHN SAS

- Landforce

- Mahindra and Mahindra Ltd.

- Maschio Gaspardo S.p.A.

- Piara Singh and Sons

- Preet Agro Industries Pvt. Ltd.

- Sonalika International Tractors Ltd.

- Tirth Agro Technology Pvt. Ltd.

- Tractors and Farm Equipment Ltd.

- Yanmar Holdings Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Rotavator market

- In April 2025, CNH Industrial NV strengthened its presence in South America with the launch of new digital farming solutions and compatible implements, including advanced rotary tillers designed for the region's diverse agricultural needs.

- In February 2025, Kubota Corp. showcased enhanced interoperability between its latest utility tractors and specialized rear-mounted implements at the World Ag Expo, demonstrating advanced rotary tillers for specialty crop applications.

- In January 2025, Mahindra and Mahindra Ltd. reported a significant surge in its farm equipment sector sales, attributing the robust performance to strong demand for tractors and implements like rotavators, driven by favorable conditions for the Rabi crop harvest.

- In January 2025, Sonalika International Tractors Ltd. announced a strategic expansion of its heavy-duty farm implement portfolio, with a specific focus on exporting advanced rotavator series to European and American markets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Rotavator Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.5% |

| Market growth 2026-2030 | USD 491.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.3% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, South Africa, Saudi Arabia, UAE, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The rotavator market reflects a strategic pivot toward high-efficiency tillage solutions that address core operational and financial objectives. This tractor-mounted implement has become indispensable for achieving single-pass tillage, directly impacting cost-control measures. The integration of advanced components such as a multi-speed gearbox and durable, wear-resistant blades is critical, with newer implements demonstrating a reduction in maintenance needs by over 25%.

- Innovations in tillage depth control and hydraulic offset capabilities allow for precise soil conditioning and crop residue incorporation, which are essential for sustainable farming. The choice between C-type blades and L-type blades is tailored to specific soil types to optimize soil aeration and support mechanical weed control.

- Effective utilization of the power take-off (PTO) to power rotary tiller blades for soil pulverization is fundamental to superior seedbed preparation, enhancing both productivity and crop quality across both wetland cultivation and dry-land farming scenarios.

What are the Key Data Covered in this Rotavator Market Research and Growth Report?

-

What is the expected growth of the Rotavator Market between 2026 and 2030?

-

USD 491.4 million, at a CAGR of 4.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Hydraulic, and Fixed), Type (L type, and C type), Application (Seedbed preparation, Soil conditioning, Crop residue management, Horticulture, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing need for nutrient protection in agriculture fields, Growing threat from substitute products

-

-

Who are the major players in the Rotavator Market?

-

Action Construction Equipment Ltd., AGCO Corp., Beri Udyog Pvt. Ltd., CLAAS KGaA, CNH Industrial NV, Deere and Co., Greaves Cotton Ltd., Kubota Corp., KUHN SAS, Landforce, Mahindra and Mahindra Ltd., Maschio Gaspardo S.p.A., Piara Singh and Sons, Preet Agro Industries Pvt. Ltd., Sonalika International Tractors Ltd., Tirth Agro Technology Pvt. Ltd., Tractors and Farm Equipment Ltd. and Yanmar Holdings Co. Ltd.

-

Market Research Insights

- Market dynamics are increasingly shaped by a focus on maximizing agricultural output through advanced implements. The adoption of rotavators with automated side-shift mechanisms can improve operational efficiency in horticulture tillage by up to 25% compared to manual adjustments. Furthermore, the integration of certified safety guards and ISO-certified designs reduces equipment downtime and enhances operator safety, contributing to better overall performance.

- Transitioning from conventional primary tillage to rotavator-based secondary tillage practices can lower fuel consumption efficiency by over 15%, directly impacting operational time reduction. These advancements in agricultural machinery influence purchasing decisions, with a growing emphasis on implement durability and compatibility with existing tractor horsepower requirements to optimize soil tilth and stubble management.

We can help! Our analysts can customize this rotavator market research report to meet your requirements.