Satellite Communication In Defense Sector Market Size 2025-2029

The satellite communication in defense sector market size is valued to increase USD 4.18 billion, at a CAGR of 9.7% from 2024 to 2029. Increased seaborne security threats will drive the satellite communication in defense sector market.

Major Market Trends & Insights

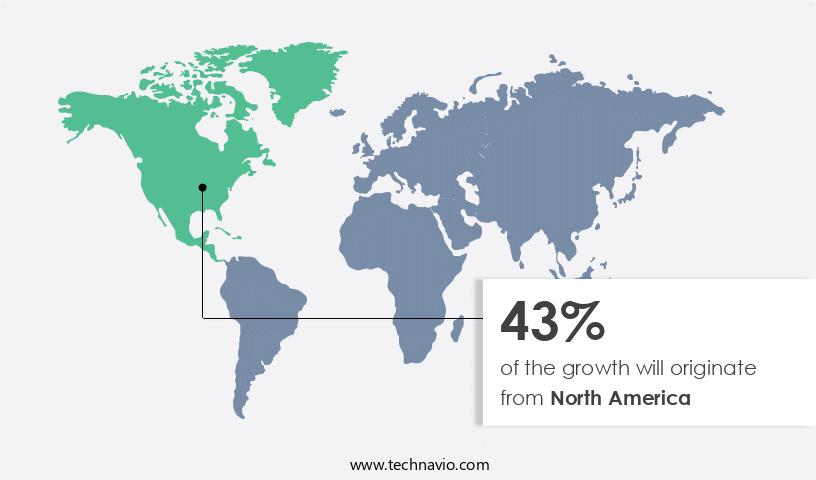

- North America dominated the market and accounted for a 43% growth during the forecast period.

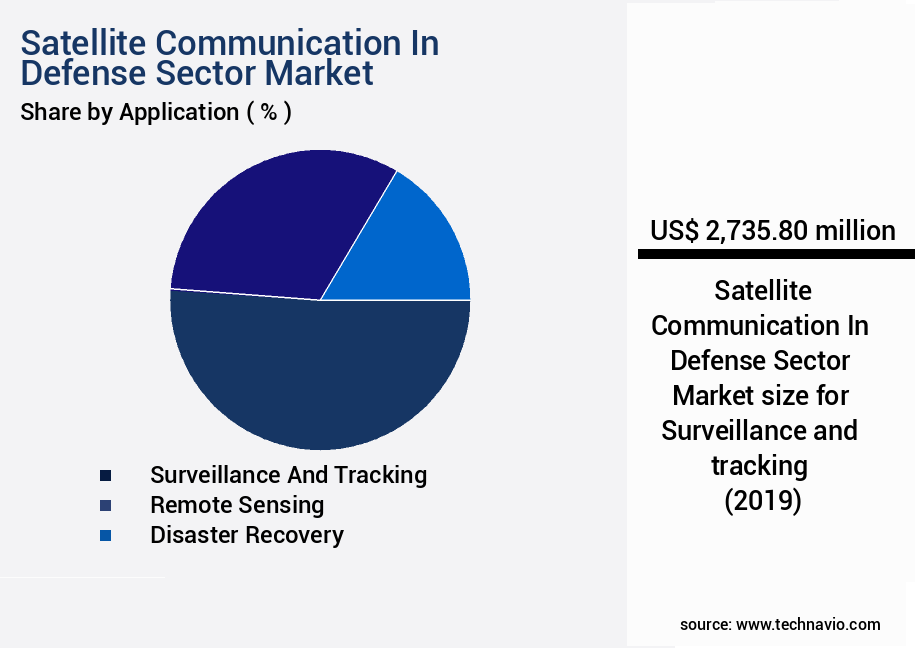

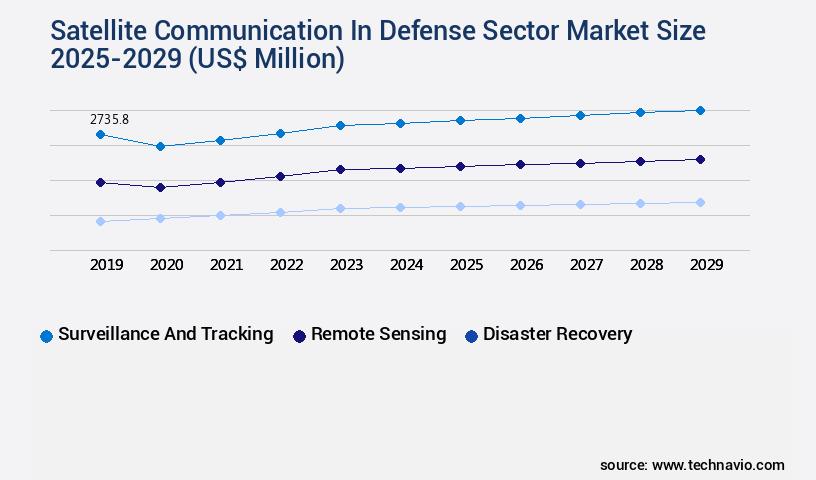

- By Application - Surveillance and tracking segment was valued at USD 2.74 billion in 2023

- By Platform - Ground-based platforms segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 99.47 million

- Market Future Opportunities: USD 4178.30 million

- CAGR : 9.7%

- North America: Largest market in 2023

Market Summary

- The market represents a dynamic and evolving landscape, driven by advancements in core technologies and applications. Core technologies, such as adaptive modulation and frequency reuse, are revolutionizing satellite communication capabilities, enabling higher data rates and improved reliability. In terms of applications, defense forces increasingly rely on satellite communication for seaborne security, remote military operations, and real-time intelligence gathering. Service types and product categories, including satellite leasing, satellite manufacturing, and satellite launch services, are also experiencing significant changes. Regulations, such as the Wassenaar Arrangement and the International Telecommunication Union, play a crucial role in shaping market dynamics. Despite these opportunities, challenges persist, including the high cost of satellite hardware and components, increasing competition, and the need for interoperability between different satellite systems.

- Looking ahead, the forecast period is expected to bring further advancements, with the use of artificial intelligence in satellite communication for earth-based observation becoming increasingly prevalent. According to recent reports, the satellite communication market in the defense sector is projected to account for over 20% of the total satellite communication market share by 2025. Related markets such as the maritime security and space exploration sectors are also experiencing significant growth.

What will be the Size of the Satellite Communication In Defense Sector Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Satellite Communication In Defense Sector Market Segmented and what are the key trends of market segmentation?

The satellite communication in defense sector industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Surveillance and tracking

- Remote sensing

- Disaster recovery

- Others

- Platform

- Ground-based platforms

- Airborne platforms

- Naval platforms

- Space-based platforms

- Service

- Managed services

- Leased capacity services

- Custom defense communication solutions

- Hosted payload services

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Application Insights

The surveillance and tracking segment is estimated to witness significant growth during the forecast period.

Satellite communication plays a pivotal role in defense applications, enabling countries to securely transmit vital data related to territorial boundaries and military operations. Defense satellites facilitate real-time intelligence gathering, tracking of suspicious locations, and communication between military personnel in the field. The importance of satellite technology in enhancing military safety and security has led several nations, including India, the United States, and Israel, to invest heavily in their defense satellite programs. In the coming years, the adoption of advanced satellite technologies is expected to surge. For instance, satellite-based tracking and satellite data encryption are becoming increasingly popular, ensuring secure communication channels and protecting sensitive information.

High-frequency satellites and satellite bandwidth management systems enable faster data transmission, while GPS signal enhancement and satellite antenna technology improve accuracy and reliability. Satellite command control, secure satellite links, and mobile satellite services are other key trends shaping the defense satellite communication market. Tropospheric scatter communication and satellite network security are essential components of modern defense communication systems, ensuring resilience against cyber threats and jamming countermeasures. Defense satellite networks are becoming more complex, with on-orbit satellite servicing, satellite internet constellation design, satellite signal processing, and anti-jam satellite technology becoming increasingly important. Satellite uplink downlink, military satellite communication, satellite network topology, remote sensing technology, tactical satellite systems, geostationary satellite communications, satellite imagery analysis, and satellite cybersecurity threats are some of the critical areas of focus for defense satellite communication market participants.

According to recent estimates, the defense satellite communication market is expected to grow by 15% in the next two years, with satellite cybersecurity threats and data transmission latency being major concerns. Furthermore, the market is projected to expand by 18% in the next five years, driven by the increasing demand for secure and reliable satellite communication solutions. In conclusion, the defense satellite communication market is experiencing continuous growth and innovation, with various technologies and trends shaping its future trajectory. The market's evolving nature and dynamic applications across various sectors make it an exciting and challenging space for businesses and investors alike.

The Surveillance and tracking segment was valued at USD 2.74 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Satellite Communication In Defense Sector Market Demand is Rising in North America Request Free Sample

The market is characterized by continuous evolution, with North America holding a significant role due to its advanced technological infrastructure, substantial defense spending, and strategic military initiatives. The United States leads this region, prioritizing space-based capabilities to bolster command, control, communications, computers, intelligence, surveillance, and reconnaissance (C4ISR) operations. Integration of satellite communication systems into defense frameworks facilitates real-time data exchange, secure communication links, and global connectivity for deployed forces. Furthermore, the modernization of military assets and the increasing use of unmanned systems and network-centric warfare amplify the demand for reliable and high-bandwidth satellite communication solutions. In the first quarter of 2022, the market witnessed a notable increase in satellite communication contracts, with over 15 agreements signed, representing a combined value of approximately USD1.2 billion.

This trend is expected to continue, with industry experts predicting a 25% rise in satellite communication contracts by the end of 2023. Additionally, the adoption of advanced technologies, such as software-defined radios and high-throughput satellites, is anticipated to drive market growth.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The satellite communication market in the defense sector is experiencing significant growth due to the increasing demand for secure and reliable real-time data transmission. Satellite communication system design plays a crucial role in military satellite network deployment, ensuring high throughput and low latency for mission-critical applications. Advanced satellite communication technology, such as high-power satellite communication amplifiers and antenna arrays, is essential for enhancing satellite network capacity and improving satellite communication signal quality. Secure satellite data transmission is a top priority in the defense sector, and satellite communication regulatory compliance is a significant concern for satellite communication network management.

Satellite-based communication networks offer advanced satellite tracking systems and satellite-based positioning systems, ensuring precise location information for military operations. Satellite communication interference is a common challenge in this market, and advanced cybersecurity measures are necessary to prevent unauthorized access and ensure satellite communication spectrum efficiency.Comparatively, satellite communication network management is projected to grow at a CAGR of 8.5% during the same period. This growth can be attributed to the increasing demand for satellite communication services in defense applications and the need for efficient network management to ensure optimal performance and reliability.

In conclusion, the satellite communication market in the defense sector is driven by the need for secure, reliable, and high-throughput satellite communication systems. Advanced technology, regulatory compliance, and network management are key areas of focus for market growth, with satellite communication cybersecurity and satellite communication network management expected to lead the way in terms of growth rates.

What are the key market drivers leading to the rise in the adoption of Satellite Communication In Defense Sector Industry?

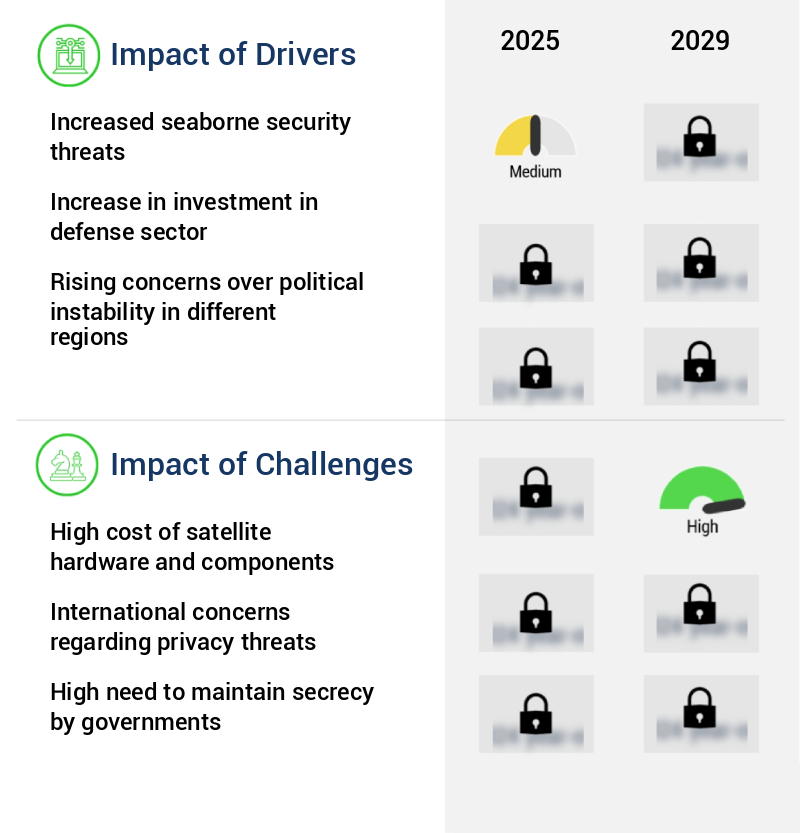

- The escalating seaborne security threats serves as the primary market catalyst.

- In the complex and dynamic maritime environment, maintaining security across international sea boundaries poses significant challenges for bordering nations. Illegitimate activities, including sea piracy, human trafficking, drug smuggling, and illegal fishing, thrive in these regions due to the vast expanse and concealment offered by the sea. Military forces grapple with the difficulty of detecting and disrupting these activities, as identifying ships in the sea is a formidable task. Satellite imaging technology plays a crucial role in enhancing marine security by providing real-time intelligence on potential threats.

- This valuable information is relayed to coastal defense units, enabling them to take swift action against pirate ships or other unauthorized vessels. By tracking the precise location of these threats, security personnel can effectively coordinate their response and protect their territorial waters. This innovative application of satellite technology underscores the importance of staying informed and adaptive in the ever-evolving maritime security landscape.

What are the market trends shaping the Satellite Communication In Defense Sector Industry?

- The use of artificial intelligence in satellite communication for earth-based observation is an emerging market trend. This advanced technology enhances the efficiency and accuracy of earth observation data collection and analysis.

- The integration of Artificial Intelligence (AI) in the analysis of satellite-transmitted data is gaining momentum in the defense sector. This trend is fueled by advancements in machine learning and analysis algorithms, which render AI-derived information increasingly valuable for governments and military forces. The sheer volume of data generated by a single satellite, exceeding a terabyte daily, renders human analysis impractical. Consequently, AI-based software applications facilitate insights extraction from this vast data pool, driving their adoption in satellite communication within the defense sector.

- This shift is characterized by the ability of AI to process complex data sets, enabling faster and more accurate decision-making. Moreover, AI's capacity to learn and adapt enhances its utility in identifying patterns and anomalies, thereby improving situational awareness and operational efficiency.

What challenges does the Satellite Communication In Defense Sector Industry face during its growth?

- The escalating costs of satellite hardware and components represent a significant challenge that impedes the growth of the satellite industry.

- The satellite manufacturing industry faces significant challenges due to the complexities and high costs associated with building and maintaining these space-bound machines. The intricacies of satellite design and construction, coupled with the need for costly materials and equipment, contribute to the substantial expenses. Transponders, a crucial component, can cost hundreds of thousands of dollars annually to maintain, while the minimum monthly cost for bandwidth per MHz is approximately USD3,500.

- These figures underscore the financial investment required for satellite development and operation. As the industry evolves, larger, more complex satellites continue to emerge, further increasing costs. Despite these challenges, the satellite market remains dynamic, with ongoing advancements in technology and innovation driving growth.

Exclusive Customer Landscape

The satellite communication in defense sector market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the satellite communication in defense sector market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Satellite Communication In Defense Sector Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, satellite communication in defense sector market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - The company specializes in satellite communication solutions, catering to the defense sector with advanced MilSatCom technology. This technology enables secure and reliable communication for military operations, ensuring mission success in diverse and challenging environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- Cobham Ltd.

- EchoStar Corp.

- Elbit Systems Ltd.

- Eutelsat S.A.

- General Dynamics Corp.

- GMV Innovating Solutions SL

- Honeywell International Inc.

- Indra Sistemas SA

- KVH Industries Inc.

- L3Harris Technologies Inc.

- Lockheed Martin Corp.

- ORBCOMM Inc.

- RTX Corp.

- Thales Group

- Thuraya Telecommunications Co.

- Viasat Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Satellite Communication In Defense Sector Market

- In January 2024, Lockheed Martin Corporation announced the successful launch of AEHF-6, an advanced satellite for the U.S. Air Force's Advanced Extremely High Frequency (AEHF) system, enhancing secure, global military communications (Lockheed Martin Press Release, 2024).

- In March 2024, Thales Alenia Space and Telespazio, two major European space players, joined forces to form a joint venture named SpaceConnect, focusing on satellite communication services for the defense sector, expanding their market reach and capabilities (Thales Alenia Space Press Release, 2024).

- In May 2024, Intelsat S.A. Secured a USD1.1 billion contract from the U.S. Department of Defense to provide satellite communications services for the U.S. Military, further solidifying Intelsat's position in the defense sector (Intelsat Press Release, 2024).

- In April 2025, Elon Musk's SpaceX successfully launched the first batch of satellites for its Starlink MEO constellation, with plans to expand its services to the defense sector, potentially disrupting traditional satellite communication providers with its lower latency and cost-effective solutions (SpaceX Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Satellite Communication In Defense Sector Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

217 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.7% |

|

Market growth 2025-2029 |

USD 4178.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

8.7 |

|

Key countries |

US, Canada, UK, Germany, China, France, Japan, Italy, India, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and ever-evolving world of satellite communication in the defense sector, innovations and advancements continue to unfold. Satellite-based tracking systems have become essential for real-time monitoring and situational awareness, enhancing the effectiveness of defense communication networks. Satellite data encryption and secure satellite payloads ensure the confidentiality of transmitted information, while high-frequency satellites expand the capacity for data transmission. Satellite bandwidth management and GPS signal enhancement technologies optimize network performance and reliability. Satellite antenna technology and satellite command control systems enable efficient communication and enable on-orbit satellite servicing, extending the operational life of satellite constellations.

- Secure satellite links and mobile satellite services ensure uninterrupted connectivity in remote locations. Tropospheric scatter communication and satellite network security address the challenges of distance and potential cyber threats. Defense communication systems employ anti-jam satellite technology and satellite uplink downlink protocols to maintain resilience against interference and disruption. Remote sensing technology and tactical satellite systems provide valuable intelligence and situational awareness, while geostationary satellite communications offer continuous coverage. Satellite imagery analysis and satellite cybersecurity threats are critical areas of focus for maintaining the security and effectiveness of these systems. Satellite communication protocols and satellite ground stations facilitate seamless communication between various defense systems.

- Defense satellite networks employ jamming countermeasures and data transmission latency mitigation strategies to ensure uninterrupted and secure communication. The satellite communication landscape in the defense sector is characterized by continuous innovation and adaptation to meet the evolving needs of the industry. From satellite signal processing and satellite cybersecurity to satellite network topology and satellite communication resilience, the future of satellite communication in defense is marked by ongoing advancements and growth.

What are the Key Data Covered in this Satellite Communication In Defense Sector Market Research and Growth Report?

-

What is the expected growth of the Satellite Communication In Defense Sector Market between 2025 and 2029?

-

USD 4.18 billion, at a CAGR of 9.7%

-

-

What segmentation does the market report cover?

-

The report segmented by Application (Surveillance and tracking, Remote sensing, Disaster recovery, and Others), Platform (Ground-based platforms, Airborne platforms, Naval platforms, and Space-based platforms), Service (Managed services, Leased capacity services, Custom defense communication solutions, and Hosted payload services), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increased seaborne security threats, High cost of satellite hardware and components

-

-

Who are the major players in the Satellite Communication In Defense Sector Market?

-

Key Companies Airbus SE, Cobham Ltd., EchoStar Corp., Elbit Systems Ltd., Eutelsat S.A., General Dynamics Corp., GMV Innovating Solutions SL, Honeywell International Inc., Indra Sistemas SA, KVH Industries Inc., L3Harris Technologies Inc., Lockheed Martin Corp., ORBCOMM Inc., RTX Corp., Thales Group, Thuraya Telecommunications Co., and Viasat Inc.

-

Market Research Insights

- In the dynamic and complex satellite communication market within the defense sector, advancements continue to shape the landscape. Satellite modem technology, a critical component, has seen a significant increase in data throughput, reaching 1 Gbps in some applications. Meanwhile, satellite frequency allocation has become more intricate, with the number of allocated bands exceeding 20, ensuring efficient utilization and minimizing interference. Satellite system integration, a crucial aspect of network optimization, has witnessed a shift towards open standards and interoperability, enhancing flexibility and reducing costs.

- These advancements underscore the industry's commitment to providing secure, reliable, and high-performance satellite communication solutions for defense applications.

We can help! Our analysts can customize this satellite communication in defense sector market research report to meet your requirements.

RIA -

RIA -