Vietnam Semiconductors Market Size 2026-2030

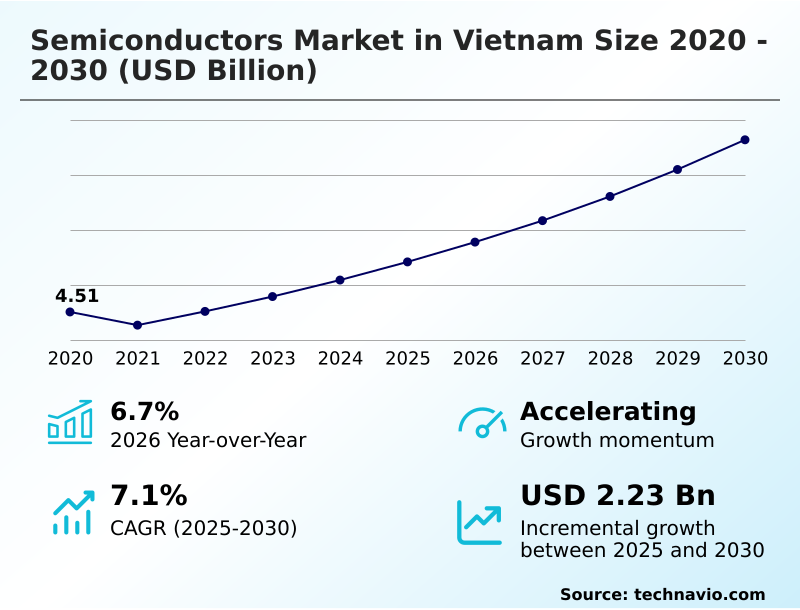

The Vietnam Semiconductors Market size was valued at USD 5.42 billion in 2025, growing at a CAGR of 7.1% during the forecast period 2026-2030.

Major Market Trends & Insights

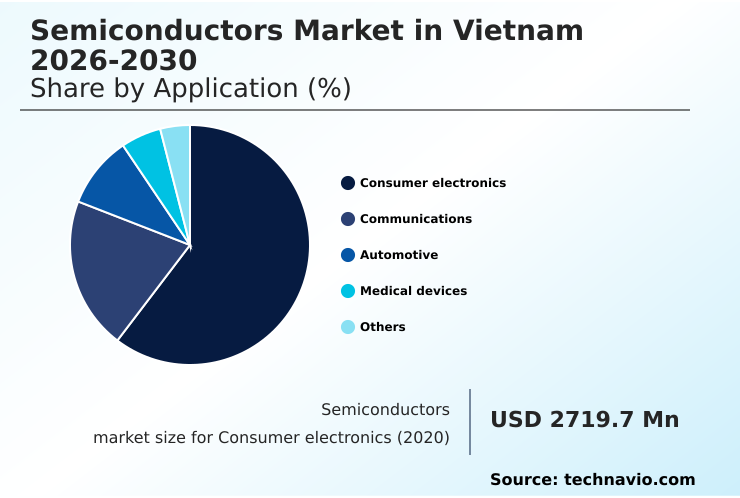

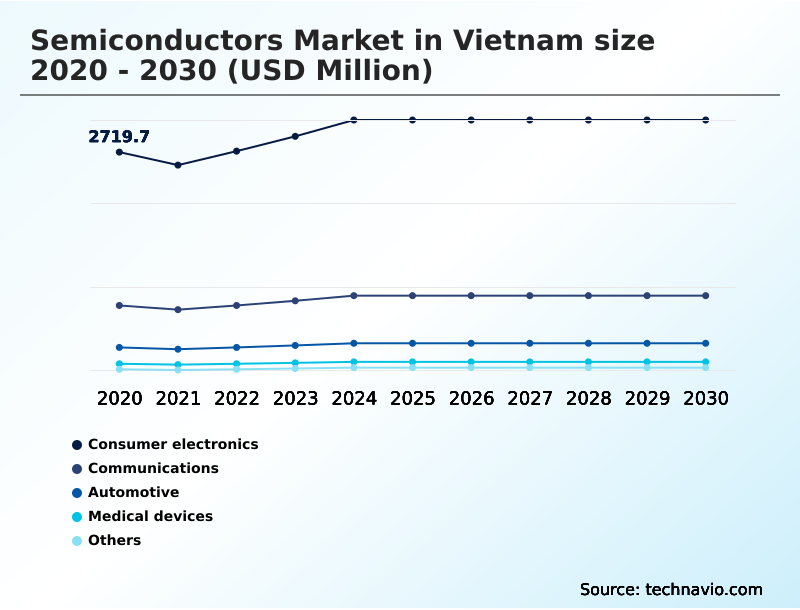

- By Application - Consumer electronics segment was valued at USD 3.10 billion in 2024

- By End-user - Memory segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 3.14 billion

- Market Future Opportunities 2025-2030: USD 2.23 billion

- CAGR from 2025 to 2030 : 7.1%

Market Summary

- The semiconductors market in Vietnam is characterized by its strategic pivot toward higher-value activities within the global electronics supply chain, even as it navigates structural limitations.

- In a typical operational scenario, a local firm specializing in outsourced semiconductor assembly and test (OSAT) might handle the backend operations for a multinational fabless company, but the critical wafer fabrication, often accounting for over 70% of the chip's value, occurs offshore.

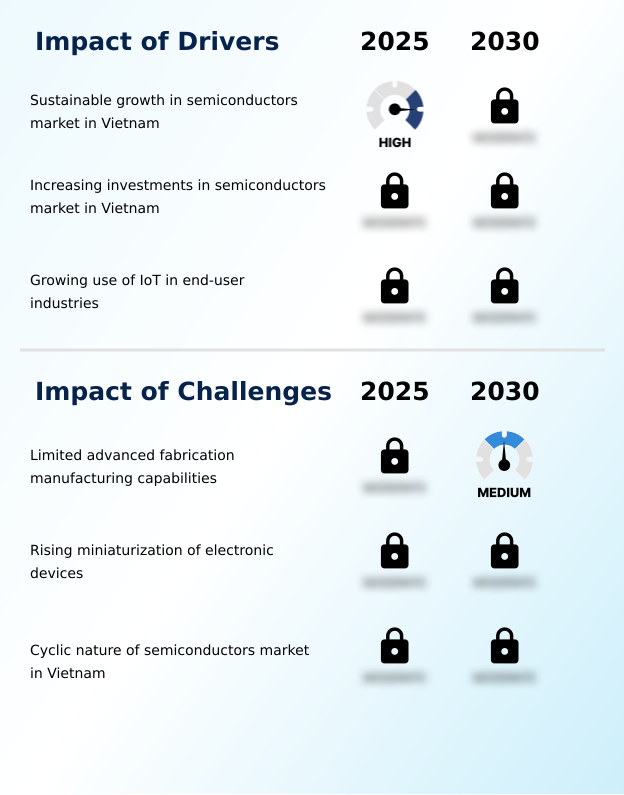

- The growing use of IoT in end-user industries is a primary driver, compelling a shift toward ultra-low-power (ULP) processors and embedded control systems. For instance, the adoption of Industry 4.0 increases the demand for IoT devices, which require ICs with characteristics such as ultra-low leakage.

- However, a significant challenge remains the limited domestic capacity for advanced fabrication, particularly for nodes below 28nm. This dependency on foreign foundries impacts production lead times and exposes the local industry to global supply chain volatility.

What will be the Size of the Vietnam Semiconductors Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Vietnam Semiconductors Market Segmented?

The vietnam semiconductors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Consumer electronics

- Communications

- Automotive

- Medical devices

- Others

- End-user

- Memory

- Foundry

- IDM

- Device

- PMICs

- Microchips

- RFID

- Geography

- APAC

How is the Vietnam Semiconductors Market Segmented by Application?

The consumer electronics segment is estimated to witness significant growth during the forecast period.

The consumer electronics segment, representing over 60% of demand, is defined by rapid product cycles and the need for high-performance, low-power components.

In this sector, the integration of a system-on-chip (SoC) can lead to a 15% reduction in device footprint, a critical factor for smartphones and wearables.

The demand for enhanced mobile photography, for instance, drives innovation in CMOS image sensors and dedicated signal processors, requiring sophisticated power management IC (PMIC) solutions to maintain battery life.

Consequently, manufacturers prioritize power efficiency optimization and low-latency communication capabilities to meet consumer expectations for seamless connectivity and extended use, directly influencing design choices in IC design and backend operations.

The Consumer electronics segment was valued at USD 3.10 billion in 2024 and showed a gradual increase during the forecast period.

What are the key Drivers, Trends, and Challenges in the Vietnam Semiconductors Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the semiconductors market in Vietnam 2026-2030 are increasingly influenced by the need to balance cost-effective manufacturing with technological advancement. For instance, selecting the right low-power IoT microcontroller involves a trade-off analysis where power consumption is weighed against processing capability, affecting device battery life by as much as 50%.

- This choice is critical for applications in smart cities and industrial automation. Similarly, the implementation of advanced semiconductor packaging techniques is essential for miniaturization, a key trend in consumer electronics. As devices become more complex, high-performance computing chiplet integration becomes a vital strategy to manage thermal output and improve yield, rather than relying on a single monolithic die.

- In the automotive sector, the design of semiconductors for automotive ADAS must meet stringent safety and reliability standards, such as ISO 26262. This requirement drives the development of specialized processors and sensors.

- Concurrently, the rollout of 5G necessitates sophisticated 5G RF front-end module design to handle higher frequencies and data rates, pushing the boundaries of current material science and manufacturing processes. These interconnected technology choices shape the competitive dynamics and operational realities across the industry.

What are the key market drivers leading to the rise in the adoption of Vietnam Semiconductors Industry?

- Sustainable growth in the semiconductors market in Vietnam is a key driver, underpinned by expanding electronics production and strategic investments.

- The rapid expansion of the Internet of Things (IoT) is a significant driver for the semiconductors market in Vietnam, creating a surge in demand for ultra-low-power (ULP) processors and specialized sensors.

- As industries adopt Industry 4.0 principles, the need for connected devices in factory automation and logistics is projected to increase chip demand in this sub-segment by over 25%.

- These applications require embedded control systems that can operate for years on a single battery, driving innovation in power efficiency optimization and sleep-state management.

- This proliferation of IoT devices directly fuels the growth of the fabless manufacturing model, as companies focus on designing specialized intellectual property (IP) cores for niche applications, subsequently relying on foundry services for mass production, thereby stimulating the entire value chain.

What are the market trends shaping the Vietnam Semiconductors Industry?

- The growing adoption of low-cost communication devices, driven by accessible technology and expanding network coverage, is a significant upcoming trend. This movement accelerates the integration of IoT and smart technologies across various consumer and industrial sectors.

- A primary trend in the semiconductors market in Vietnam is the adoption of advanced packaging technologies to overcome the physical limits of Moore's Law. This shift, which has been shown to improve interconnect density by up to 20%, is enabling the creation of more powerful and efficient devices without shrinking transistors further.

- Technologies such as system in package (SiP) and chiplet design are becoming mainstream, allowing for the integration of multiple heterogeneous dies into a single component. This modular approach accelerates development time and improves manufacturing yield by allowing different process nodes to be combined.

- For businesses, this means a faster time-to-market for complex products like AI accelerators and 5G baseband processors, directly impacting their competitiveness and ability to innovate in high-growth sectors.

What challenges does the Vietnam Semiconductors Industry face during its growth?

- Limited domestic capabilities in advanced fabrication manufacturing present a key challenge, constraining growth in the high-value segments of the industry.

- A critical challenge for the semiconductors market in Vietnam is the structural gap in advanced wafer fabrication capabilities, which limits the country to primarily backend operations. The inability to produce advanced logic nodes, such as those using FinFET or gate-all-around (GAA) architectures, means that over 90% of high-value front-end manufacturing is outsourced.

- This dependency creates significant supply chain vulnerabilities and lengthens product development cycles by 4-6 weeks compared to regions with integrated design and fabrication facilities. Furthermore, the rising miniaturization of electronics demands sophisticated yield management and thermal management solutions, increasing the technical barriers and capital investment required, which local firms struggle to meet without substantial foreign partnership.

Exclusive Technavio Analysis on Customer Landscape

The vietnam semiconductors market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the vietnam semiconductors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Vietnam Semiconductors Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, vietnam semiconductors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amkor Technology Inc. - Key offerings include advanced semiconductor services, focusing on solutions like advanced packaging, wafer-level technologies, and comprehensive test services.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amkor Technology Inc.

- Coherent Corp.

- CT Semiconductor

- FPT Semiconductor JSC

- Infineon Technologies AG

- Intel Corp.

- Microchip Technology Inc.

- NVIDIA Corp.

- NXP Semiconductors NV

- ON Semiconductor Corp.

- Qualcomm Inc.

- Renesas Electronics Corp.

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- STMicroelectronics NV

- Synopsys Inc.

- Taiwan Semiconductor Co. Ltd.

- Texas Instruments Inc.

- Toshiba Corp.

- Viettel Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Semiconductors industry, the strategic push to diversify global chip manufacturing has led to a 15% increase in planned investments for new front-end manufacturing facilities outside of traditional hubs, directly impacting supply chain resilience for the semiconductors market in vietnam 2026-2030 by creating new regional backend operations.

- Accelerated adoption of advanced driver-assistance systems (ADAS) in the automotive sector now requires automotive-grade sensor fusion algorithms and radiation-hardened components, increasing demand for specialized foundry services and ICs from the semiconductors market by over 30%.

- The expansion of 5G infrastructure and the development of non-terrestrial networks are creating a surge in demand for high-performance RF chips and baseband processors, requiring new design for manufacturability (DFM) approaches in the semiconductors market to manage signal integrity.

- Stringent new environmental regulations on industrial manufacturing are mandating the use of high-purity chemicals and advanced water recycling systems, increasing the operational cost of wafer fabrication for the semiconductors market in vietnam 2026-2030 by an estimated 5-8%.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Vietnam Semiconductors Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 198 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.1% |

| Market growth 2026-2030 | USD 2226.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.7% |

| Key countries | Vietnam |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The semiconductors market in Vietnam ecosystem is a complex network where raw material suppliers provide high-purity silicon and chemicals to foundries and integrated device manufacturers (IDMs), which perform wafer fabrication. This ecosystem supports a 7.1% year-over-year growth momentum. Fabless companies, which focus on IC design, rely on electronic design automation (EDA) software and intellectual property (IP) cores before outsourcing production.

- The output, including components like power management IC (PMIC) and network-on-chip, is then handled by firms specializing in backend operations for assembly and testing, a segment where Vietnam holds a significant regional share. These finished chips are distributed to OEMs in consumer electronics and automotive industries, which together account for over 70% of end-user consumption.

- Government bodies and trade associations influence the market through investment incentives and workforce development programs aimed at enhancing local capabilities.

What are the Key Data Covered in this Vietnam Semiconductors Market Research and Growth Report?

-

What is the expected growth of the Vietnam Semiconductors Market between 2026 and 2030?

-

The Vietnam Semiconductors Market is expected to grow by USD 2.23 billion during 2026-2030, registering a CAGR of 7.1%. Year-over-year growth in 2026 is estimated at 6.7%%. This acceleration is shaped by sustainable growth in semiconductors market in vietnam, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Consumer electronics, Communications, Automotive, Medical devices, and Others), End-user (Memory, Foundry, and IDM), Device (PMICs, Microchips, and RFID) and Geography (APAC). Among these, the Consumer electronics segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC. Country-level analysis includes Vietnam, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is sustainable growth in semiconductors market in vietnam, which is accelerating investment and industry demand. The main challenge is limited advanced fabrication manufacturing capabilities, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Vietnam Semiconductors Market?

-

Key vendors include Amkor Technology Inc., Coherent Corp., CT Semiconductor, FPT Semiconductor JSC, Infineon Technologies AG, Intel Corp., Microchip Technology Inc., NVIDIA Corp., NXP Semiconductors NV, ON Semiconductor Corp., Qualcomm Inc., Renesas Electronics Corp., Robert Bosch GmbH, Samsung Electronics Co. Ltd., STMicroelectronics NV, Synopsys Inc., Taiwan Semiconductor Co. Ltd., Texas Instruments Inc., Toshiba Corp. and Viettel Group. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape of the semiconductors market in Vietnam is intensifying, with over 15 major international firms establishing significant operational footprints. Key vendors are actively shaping the market through strategic investments and technological advancements. For instance, Intel Corp. is expanding its assembly and test facilities, representing the largest US tech investment in the country, while Samsung Electronics Co. Ltd.

- focuses on advanced packaging technologies like system in package (SiP). These actions are a direct response to the growing demand for higher integration and miniaturization, particularly from the consumer electronics and automotive sectors. This trend drives innovation in wafer-level packaging and 3D integration.

- However, the entire ecosystem faces the persistent challenge of developing a sufficiently skilled engineering workforce capable of supporting these advanced manufacturing processes, which can slow the adoption of next-generation technologies.

We can help! Our analysts can customize this vietnam semiconductors market research report to meet your requirements.

RIA -

RIA -