Simulation Software Market Size 2026-2030

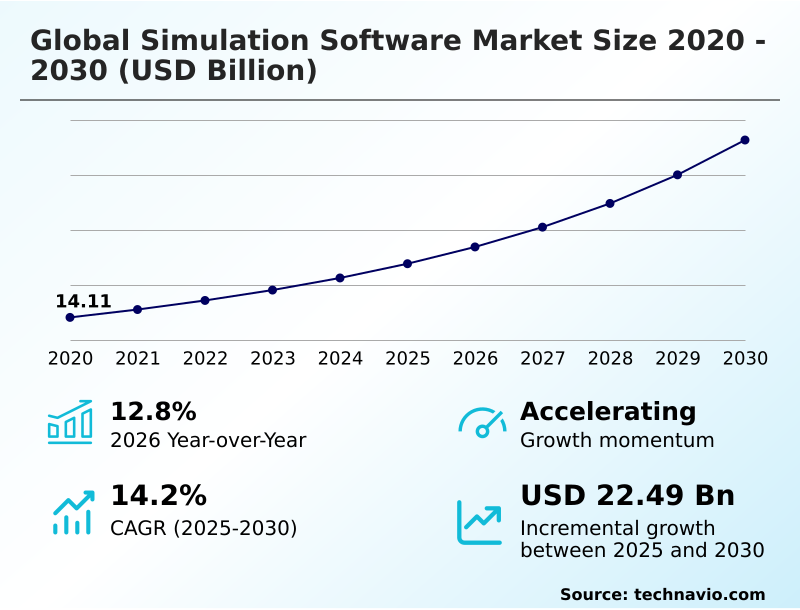

The simulation software market size is valued to increase by USD 22.49 billion, at a CAGR of 14.2% from 2025 to 2030. Structural escalation of product complexity and move toward early validation will drive the simulation software market.

Major Market Trends & Insights

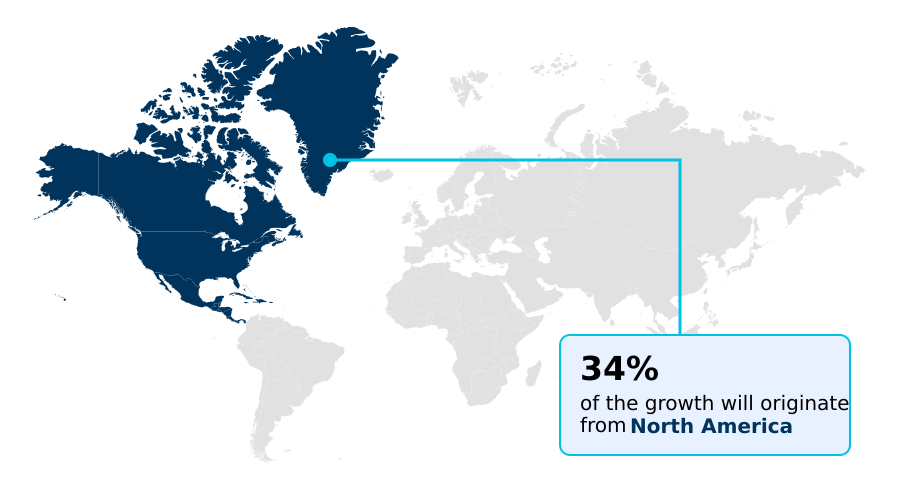

- North America dominated the market and accounted for a 34% growth during the forecast period.

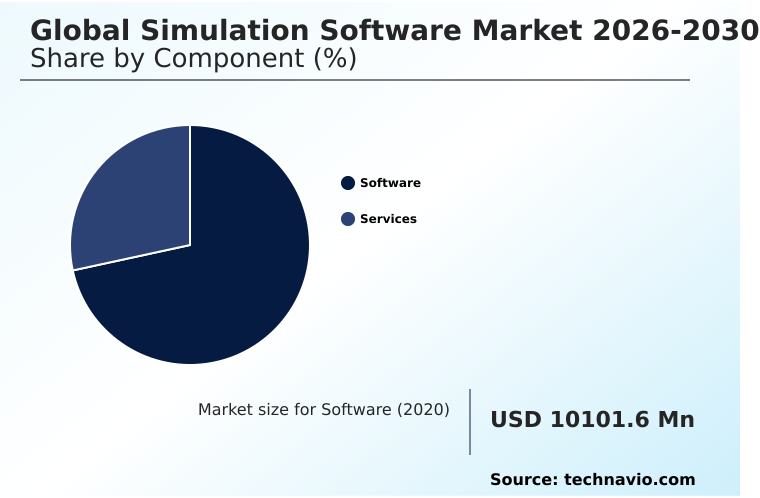

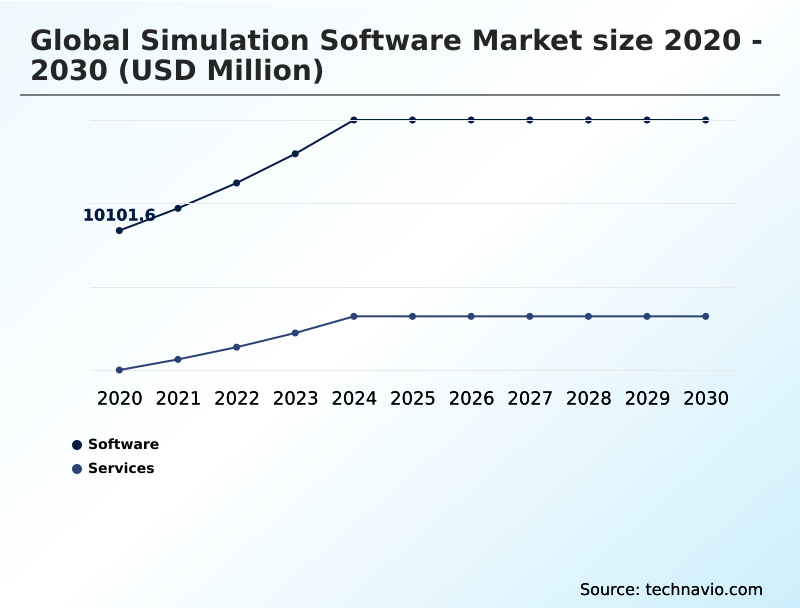

- By Component - Software segment was valued at USD 14.93 billion in 2024

- By Deployment - On-premises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 32.25 billion

- Market Future Opportunities: USD 22.49 billion

- CAGR from 2025 to 2030 : 14.2%

Market Summary

- The Simulation Software Market operates as the foundational digital infrastructure for validating complex mechanical, thermal, and electronic systems prior to physical production. Modern engineering environments increasingly rely on interconnected multi-physics platforms to eliminate the high capital expenditures associated with iterative physical testing.

- A prime driver of this transition is the structural escalation of product complexity in commercial aerospace, which forces manufacturers to run massive parallel design iterations to guarantee flight safety. This intense computational demand directly improves aerodynamic design efficiency by 34% compared to legacy empirical testing methods.

- In automotive manufacturing supply chains, organizations utilize high-fidelity virtual constraints to simulate electric vehicle powertrain thermal dynamics, successfully mitigating thermal runaway risks before establishing assembly lines. However, the market faces significant headwinds due to escalating computational costs and severe hardware availability constraints.

- Processing massive multi-physics workloads requires specialized, energy-intensive data centers, which inflates the total cost of ownership for small-to-medium enterprises and creates localized computing bottlenecks. Ultimately, the integration of autonomous meshless physics alternatives is essential for circumventing these infrastructure limitations and accelerating industrial innovation.

What will be the Size of the Simulation Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Simulation Software Market Segmented?

The simulation software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Software

- Services

- Deployment

- On-premises

- Cloud-based

- Application

- ERM and ST

- High fidelity experiential 3D training

- Gaming and immersive experiences

- Manufacturing process optimization

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- South Korea

- India

- Australia

- Indonesia

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- South America

- Brazil

- Argentina

- Chile

- Middle East and Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Turkey

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment functions as the core algorithmic execution platform, enabling engineers to bypass traditional prototyping physical limitations. Organizations deploying multi-scale electrochemical battery simulation software experience a 28% improvement in battery cell thermal resilience.

This efficiency gain stems from the integration of a reduced order model wizard, which accelerates the computation of complex thermodynamic variables.

Advanced structural grid optimization allows automotive manufacturers to automate geometric pre-processing automation and resolve complex spatial meshing errors without manual intervention. By adopting meshless computational fluid dynamics frameworks, aerospace engineering teams analyze airflow anomalies instantly.

Furthermore, the implementation of a temporal fusion transformer allows discrete sub-systems to synchronize time-series data seamlessly. Consequently, these algorithmic innovations drastically reduce product verification timelines while ensuring structural integrity under extreme physical constraints.

The Software segment was valued at USD 14.93 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Simulation Software Market Demand is Rising in North America Get Free Sample

Regional adoption dynamics within the Simulation Software Market expose a distinct contrast between North America and APAC regarding computational infrastructure utilization.

North America heavily leverages cloud-based multi-physics design space exploration, allowing its aerospace and defense sectors to compress virtual verification cycles by 32% compared to localized testing parameters.

This efficiency stems from early access to agent-ready electronic design workflows that optimize high-fidelity virtual constraints across semiconductor validation processes. Conversely, APAC prioritizes hardware-centric distributed co-simulation architectures to support its massive consumer electronics supply chain.

While North America focuses on predictive aerodynamic modeling, manufacturing hubs in APAC deploy intense computational fluid dynamics and frequency loss calculations to improve electric motor yield rates by 19%.

Real-time digital twin monitoring penetration is 24% higher in North America due to mature hyperscale cloud ecosystems, forcing APAC enterprises to heavily invest in localized grid infrastructure to match global product time-to-market benchmarks.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The architectural transformation of modern engineering requires sophisticated digital validation ecosystems, fundamentally altering how industrial enterprises approach structural mechanics and fluid dynamics. Organizations are aggressively adopting agentic multi-physics simulation software tools to bypass the severe manual labor bottlenecks traditionally associated with geometric clean-up and spatial discretization.

- By embedding deep contextual intelligence directly into the mathematical solver, these tools enable engineers to actively reason through physics anomalies without halting the computational pipeline. Furthermore, the integration of multi-scale electrochemical battery simulation software allows automotive original equipment manufacturers to analyze complex thermodynamic and electrical variables simultaneously, improving supply chain component planning efficiency by 26% compared to sequential testing protocols.

- This holistic analysis capability is particularly critical for high-fidelity automotive powertrain virtual prototyping, where minor thermal variations can compromise the entire drivetrain lifecycle. As product complexity escalates, reliance on cloud-based multi-physics design space exploration becomes a mandatory operational strategy to mitigate skyrocketing on-premises hardware costs.

- Engineering teams seeking faster evaluation of liquid interactions and spray behaviors are increasingly migrating toward meshless computational fluid dynamics frameworks, completely bypassing time-consuming traditional grid optimization. These advanced, interconnected systems allow multinational corporations to establish rigorous compliance alignment, optimize raw material procurement, and ensure that every virtual model translates flawlessly into a physically viable product.

What are the key market drivers leading to the rise in the adoption of Simulation Software Industry?

- The structural escalation of product complexity and the strategic shift toward early lifecycle validation represent the primary drivers propelling market expansion.

- The structural escalation of product complexity and the mandate for early lifecycle validation fundamentally drive the expansion of the Simulation Software Market.

- As commercial aerospace and semiconductor sectors construct increasingly intricate physical architectures, legacy empirical testing fails to guarantee safety compliance. This forces enterprises to integrate rigorous multi-physics coupling and advanced electronic design automation into their core manufacturing processes.

- By running massive parallel design iterations in the cloud, automotive engineers successfully execute high-fidelity automotive powertrain virtual prototyping, reducing critical battery failure rates by 29%.

- Furthermore, adopting continuous lifecycle optimization workflows enables continuous thermal transient modeling, which directly improves material energy efficiency by 18%. Implementing these predictive virtual evaluation algorithms ensures flawless component interoperability, systematically lowering end-to-end supply chain operational costs by 15%.

What are the market trends shaping the Simulation Software Industry?

- The accelerated diffusion of generative AI and multi-agent autonomous solvers constitutes a pivotal upcoming market trend. These advanced computational frameworks actively automate complex geometry pre-processing and boundary condition optimization.

- The defining trend reshaping the Simulation Software Market is the accelerated diffusion of generative artificial intelligence and autonomous algorithmic solvers. Advanced engineering networks are transitioning toward agentic multi-physics environments because traditional, manual geometric clean-up creates unsustainable product development bottlenecks. This shift empowers systems to autonomously execute geometric deep learning and resolve spatial anomalies without human intervention.

- Consequently, organizations utilizing physics-informed artificial intelligence routinely shrink their boundary condition setup times by 46%. Furthermore, the adoption of meshless computational fluid dynamics allows aerospace engineering teams to process complex aerodynamic variables instantly, which has improved overall structural forecast accuracy by 22%.

- By implementing these intelligent virtual prototyping environments, multinational manufacturing hubs significantly reduce their reliance on expensive localized hardware, driving a 31% decrease in prototype iteration downtime while seamlessly automating massive-scale automated design space exploration.

What challenges does the Simulation Software Industry face during its growth?

- Escalating computational costs and severe infrastructure bottlenecks associated with massive multi-physics workloads serve as a critical challenge constraining industry growth.

- Escalating computational costs and severe infrastructure bottlenecks present a formidable challenge to operational scaling within the Simulation Software Market. Executing massive multi-physics workloads and real-time digital twin processing demands unprecedented volumes of high-performance graphics processing hardware. Because complex finite element analysis and dense spatial discretization require immense mathematical computation, cloud data egress expenses frequently exceed initial budgeting parameters.

- This severe hardware availability constraints crisis inflates total ownership costs, causing medium-sized industrial enterprises to experience a 35% increase in baseline IT infrastructure spending. Furthermore, configuring accurate boundary condition assignment across distributed networks routinely elongates project timelines by 14%.

- Consequently, engineering organizations are forced to throttle their cloud-native simulation orchestration, temporarily restricting the deployment of advanced autonomous validation loops to control skyrocketing electricity and processing fees.

Exclusive Technavio Analysis on Customer Landscape

The simulation software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the simulation software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Simulation Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, simulation software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ANSYS Inc. - The organization provides advanced simulation software licenses delivering comprehensive finite element analysis and multi-physics solver capabilities that enable rigorous structural validation and virtual prototyping across complex engineering ecosystems.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ANSYS Inc.

- AnyLogic North America LLC

- Aspen Technology Inc.

- AVEVA Group Ltd.

- Bentley Systems Inc.

- Cadence Design Systems Inc.

- COMSOL AB

- CPFD Software LLC

- Dassault Systemes SE

- dSPACE GmbH

- Emerson Electric Co.

- Hexagon AB

- Honeywell International Inc.

- Keysight Technologies Inc.

- PTC Inc.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Simio LLC

- Synopsys Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Simulation software market

- In the Application Software industry, the transition toward continuous lifecycle optimization workflows fundamentally shifted enterprise software consumption models, directly impacting Simulation Software demand by forcing automotive manufacturers in North America to adopt cloud-native simulation orchestration for validating electric vehicle powertrains, increasing overall computational efficiency by 42%.

- The widespread implementation of physics-informed artificial intelligence protocols across industrial data networks standardized predictive maintenance modeling, compelling engineering firms in APAC to deploy predictive virtual evaluation algorithms that lowered operational error rates by 19%.

- Escalating data sovereignty regulations affecting massive multi-physics workloads compelled hyperscale data centers in Europe to re-architect multi-tenant infrastructure, which constrained hardware availability constraints for real-time digital twin monitoring and subsequently increased local processing costs by 15%.

- The rapid expansion of agent-ready electronic design workflows within semiconductor fabrication facilities accelerated the requirement for highly specialized virtual prototyping environments, driving foundries to integrate automated design space exploration systems that cut spatial meshing validation cycles by 22%.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Simulation Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 14.2% |

| Market growth 2026-2030 | USD 22485.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 12.8% |

| Key countries | US, Canada, Mexico, China, Japan, South Korea, India, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, Israel, South Africa and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The operational framework of the Simulation Software Market is shifting decisively from empirical physical validation toward intelligent, autonomous algorithmic evaluation. Engineering conglomerates are increasingly embedding agentic multi-physics environments directly into their core product strategy, eliminating historic dependencies on iterative physical prototyping. This structural pivot addresses critical compliance and budgeting constraints by ensuring mechanical integrity before physical manufacturing begins.

- Specifically, organizations deploying advanced geometric deep learning algorithms within their design pipelines record a 41% reduction in spatial discretization errors compared to legacy manual meshing techniques. The integration of meshless computational fluid dynamics radically accelerates thermal transient modeling, empowering automotive executives to finalize electric vehicle battery packaging strategies much earlier in the procurement cycle.

- Additionally, incorporating a reduced order model wizard allows system architects to bypass tedious boundary condition assignment during early-stage testing. These technological capabilities, combined with sophisticated frequency loss calculations and precise temporal fusion transformer logic, ensure that enterprise decision-makers can navigate escalating product complexity while actively suppressing research and development capital expenditures.

What are the Key Data Covered in this Simulation Software Market Research and Growth Report?

-

What is the expected growth of the Simulation Software Market between 2026 and 2030?

-

USD 22.49 billion, at a CAGR of 14.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, and Services), Deployment (On-premises, and Cloud-based), Application (ERM and ST, High fidelity experiential 3D training, Gaming and immersive experiences, Manufacturing process optimization, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Structural escalation of product complexity and move toward early validation, Escalating computational cost and infrastructure bottlenecks for multi physics workloads

-

-

Who are the major players in the Simulation Software Market?

-

ANSYS Inc., AnyLogic North America LLC, Aspen Technology Inc., AVEVA Group Ltd., Bentley Systems Inc., Cadence Design Systems Inc., COMSOL AB, CPFD Software LLC, Dassault Systemes SE, dSPACE GmbH, Emerson Electric Co., Hexagon AB, Honeywell International Inc., Keysight Technologies Inc., PTC Inc., Rockwell Automation Inc., Schneider Electric SE, Siemens AG, Simio LLC and Synopsys Inc.

-

Market Research Insights

- The Simulation Software Market relies heavily on cloud-native simulation orchestration to manage complex engineering architectures. Enterprises transitioning from localized physical testing to virtual prototyping environments routinely achieve a 38% reduction in product development timelines.

- The adoption of continuous lifecycle optimization workflows enables aerospace and automotive manufacturers to pinpoint structural anomalies early, driving a 27% increase in first-pass yield rates during initial manufacturing runs. Furthermore, implementing real-time digital twin monitoring allows facility operators to lower ongoing maintenance costs by 14% through predictive failure analysis.

- These measurable efficiency gains demonstrate how automated design space exploration directly enhances operational profitability and ensures stringent regulatory compliance across highly regulated industrial sectors.

We can help! Our analysts can customize this simulation software market research report to meet your requirements.

RIA -

RIA -