Skin Packaging Market Size 2026-2030

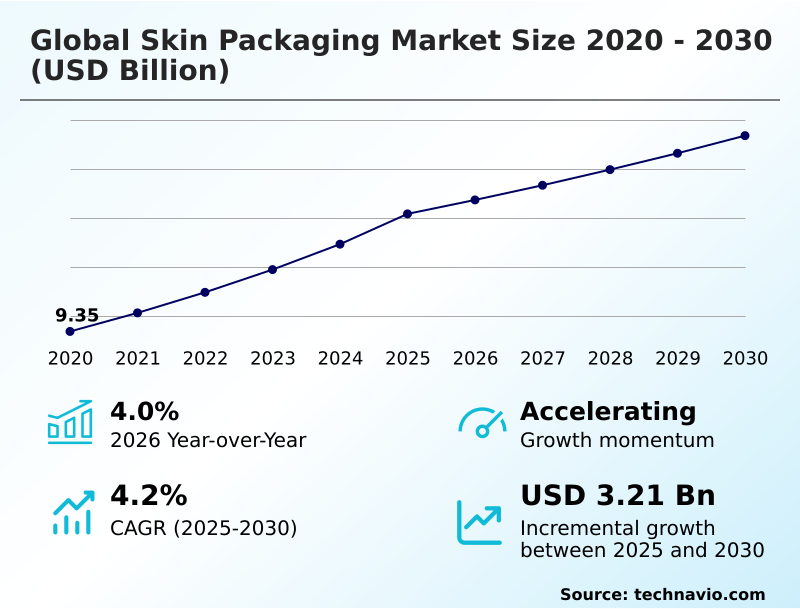

The skin packaging market size is valued to increase by USD 3.21 billion, at a CAGR of 4.2% from 2025 to 2030. Escalating global food waste reduction will drive the skin packaging market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 48.4% growth during the forecast period.

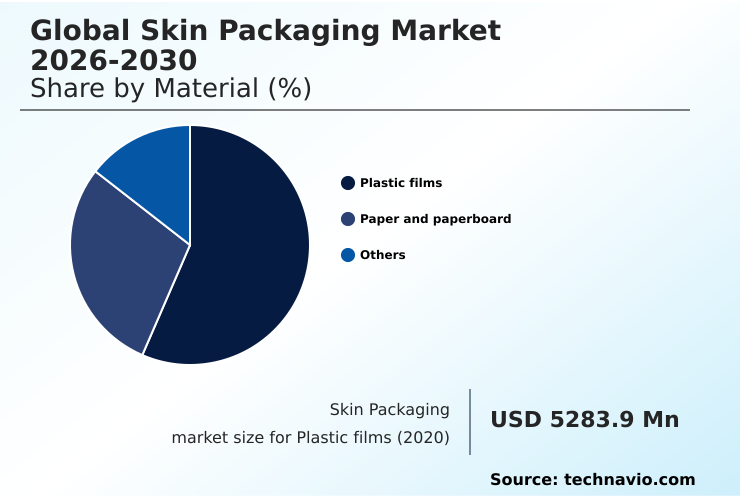

- By Material - Plastic films segment was valued at USD 7.40 billion in 2024

- By Type - Non-carded skin packaging segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 8.01 billion

- Market Future Opportunities: USD 3.21 billion

- CAGR from 2025 to 2030 : 4.2%

Market Summary

- The skin packaging market is defined by its use of vacuum and heat technology to create a protective, form-fitting seal around products. This process, involving thermoforming machines and high barrier films, is critical for extending the freshness of perishable goods by creating an anaerobic environment that slows spoilage.

- Key applications are found in the packaging of case-ready proteins, medical devices, and industrial goods, where product shelf life extension and a tamper-evident seal are paramount. A major driver is the global focus on food waste reduction, as this technology can significantly prolong the viability of fresh foods.

- Concurrently, the industry is navigating a transition toward sustainable packaging materials, with a focus on monomaterial films and paper-based substrates to align with circular economy principles. For instance, a food processor can optimize its supply chain efficiency by adopting automated packaging lines, which improve seal integrity and reduce contamination risks, thereby cutting product loss rates.

- However, challenges persist, including the high capital machinery investment and the complexities of recycling coextruded multilayer films, which tempers the pace of adoption for smaller enterprises.

What will be the Size of the Skin Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Skin Packaging Market Segmented?

The skin packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

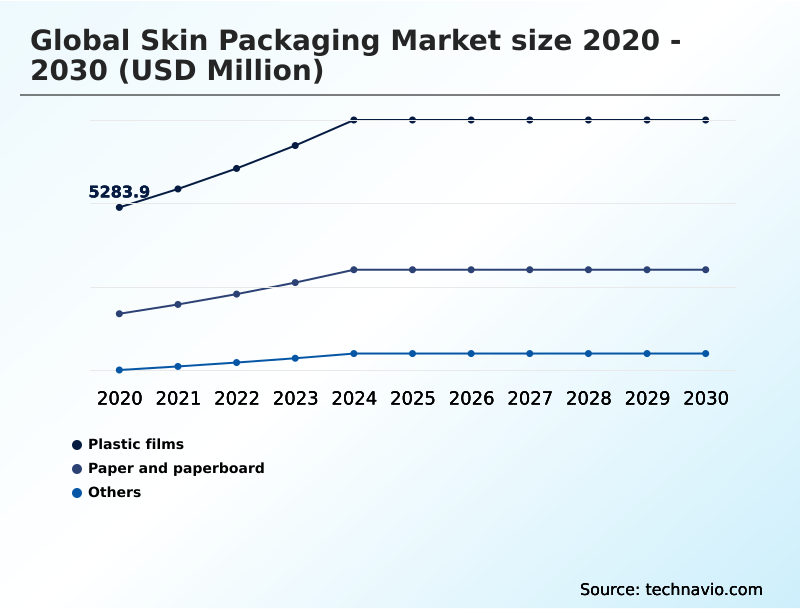

- Material

- Plastic films

- Paper and paperboard

- Others

- Type

- Non-carded skin packaging

- Carded skin packaging

- Application

- Industrial goods

- Food

- Medical devices

- Durable consumer goods

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Material Insights

The plastic films segment is estimated to witness significant growth during the forecast period.

The plastic films segment is integral to the skin packaging market, defined by its sophisticated multi-layer structures and exceptional barrier properties. The production of these coextruded multilayer films, often incorporating materials like ethylene vinyl alcohol (EVOH), utilizes advanced coextrusion technology.

This creates thin, robust materials essential for the vacuum skin packaging process. A primary driver is the need for product shelf life extension in the fresh protein sector, where creating an anaerobic environment is key.

Innovations in material science innovation are leading to thinner high barrier films, which can reduce plastic volume by over 20% without compromising puncture resistance or seal integrity.

This shift addresses environmental concerns, a key aspect of new product development, while maintaining performance for food contact materials and supporting circular economy principles.

The Plastic films segment was valued at USD 7.40 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 48.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Skin Packaging Market Demand is Rising in APAC Get Free Sample

The geographic landscape reveals a market led by APAC, which accounts for 48.4% of the incremental growth, driven by modernization in cold chain logistics and rising demand for case-ready proteins.

In contrast, North America and Europe, while mature, are shaped by stringent food safety regulations and a focus on supply chain efficiency and plastic waste reduction. This has spurred the adoption of paper-based substrates and lightweight packaging design.

Operational efficiencies are a key differentiator; for example, North American firms have leveraged robotic product loading to achieve a 15% increase in throughput on automated packaging lines.

This highlights a global divergence where emerging regions prioritize food preservation and access, while developed markets concentrate on sustainability and advanced operational cost management, influencing new product development across the board.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the skin packaging market hinges on a complex cost-benefit analysis of automated packaging lines versus manual systems and a nuanced evaluation of material choices. The benefits of paper-based substrates in skin packaging, which enhance retail shelf appeal and align with sustainability goals, must be weighed against the superior performance of high barrier films in specific applications.

- For instance, a key consideration is the comparison of high barrier films vs modified atmosphere packaging, where skin packs often provide better product visibility and a 15-20% reduction in package volume, impacting logistics costs. For companies targeting the premium fresh protein market, investing in monomaterial films for fresh protein packaging is critical for meeting recyclability mandates.

- Adopting skin packaging for durable consumer goods or for sterile medical device applications requires a different set of technical specifications focused on puncture resistance and a tamper-evident seal.

- Ultimately, the role of skin packaging in reducing food waste and extending shelf life of seafood with skin packaging provides a strong ROI, but this is tempered by recycling challenges of coextruded multilayer films and the impact of raw material price on packaging costs.

- Enhancing brand differentiation with skin packaging, therefore, requires a holistic strategy that aligns technology, material science, and market positioning.

What are the key market drivers leading to the rise in the adoption of Skin Packaging Industry?

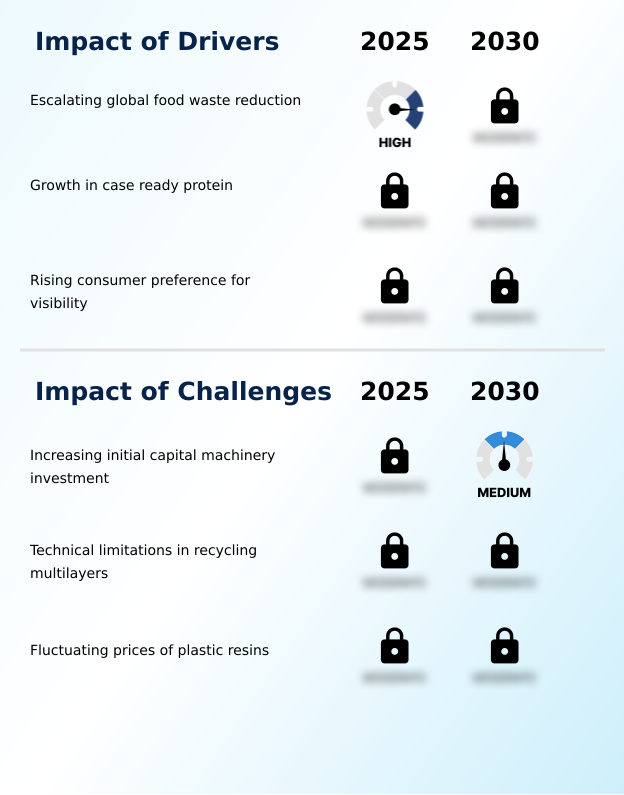

- The escalating need for global food waste reduction serves as a key driver for the market's growth.

- Market growth is significantly driven by the urgent need for food waste reduction and shifting consumer preferences.

- Skin packaging's ability to create an anaerobic environment extends the freshness of case-ready proteins by up to 20 days, directly addressing the 1.3 billion tons of food wasted globally each year.

- The growth in case-ready protein, which has seen adoption rates increase by over 15% in some regions, relies on the technology’s leak-proof seal and premium product presentation.

- Furthermore, modern consumer purchasing behavior prioritizes transparency, and the high clarity of vacuum skin packaging allows for a vertical retail display that enhances retail shelf appeal.

- This alignment with demand for clean label products and enhanced food safety continues to propel market expansion across the food and beverage industry.

What are the market trends shaping the Skin Packaging Industry?

- The adoption of paper-based substrates is an emerging trend, aiming to replace traditional plastic trays and reduce plastic content in retail environments.

- Key market trends are centered on sustainability and operational efficiency. The adoption of paper-based substrates and monomaterial films is accelerating, driven by consumer demand and regulations aimed at plastic waste reduction. This shift in material science innovation improves the recyclability of food contact materials.

- Concurrently, the integration of automated packaging lines and robotic product loading is transforming manufacturing, with some facilities reporting a 25% increase in throughput. These systems enhance seal integrity and support a hygienic packaging design. The development of sustainable high barrier film innovations, including thinner coextruded multilayer films and those with post-consumer recycled content, helps in reduced material usage.

- These trends collectively push the industry toward achieving circular economy principles while maintaining premium product presentation and supply chain efficiency.

What challenges does the Skin Packaging Industry face during its growth?

- The high initial capital investment required for machinery presents a key challenge affecting industry growth.

- The market faces significant challenges, primarily related to cost and sustainability. The high capital machinery investment required for advanced thermoforming machines, often exceeding $150,000 per line, creates a substantial barrier for smaller enterprises. Another major hurdle is the recycling infrastructure challenges associated with coextruded multilayer films, as current systems struggle to process these materials effectively.

- This technical limitation hinders plastic waste reduction efforts. Furthermore, the industry contends with raw material price volatility, with resin prices fluctuating by as much as 20% annually. This unpredictability complicates operational cost management and puts pressure on the profitability of flexible packaging solutions and rigid food trays, impacting overall supply chain efficiency.

Exclusive Technavio Analysis on Customer Landscape

The skin packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the skin packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Skin Packaging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, skin packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adapa Group - Analysis of vendors providing integrated solutions, from vacuum skin packaging films to flexible packaging solutions, which are crucial for the food and beverage industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adapa Group

- Amcor Plc

- Belco Packaging Systems Inc.

- Coveris Management GmbH

- Crawford Packaging

- Dow Chemical Co.

- Faerch AS

- G. Mondini SpA

- KM Packaging Services Ltd.

- KP Holding GmbH and Co. KG

- Mondi Plc

- MULTIVAC SE and Co. KG

- ProAmpac Holdings Inc.

- Rohrer Corp.

- Sealed Air Corp.

- SEALPAC International BV

- Starview Packaging Machinery Inc

- ULMA Packaging Ltd.

- Winpak Ltd.

- Zed Industries Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Skin packaging market

- In January, 2025, Winpak Ltd. announced the launch of a new sustainable film line specifically engineered for vacuum skin packaging applications.

- In February, 2025, Berry Global Group Inc. introduced a new range of high barrier circular films designed specifically for vacuum skin packaging that utilize a high percentage of recycled content.

- In March, 2025, Mondi Plc expanded its portfolio of paper-based solutions by introducing a new functional barrier paper designed as a substrate for vacuum skin packaging of fresh food.

- In May, 2025, MULTIVAC SE and Co. KG demonstrated a new high-speed thermoforming system designed for non-carded skin applications that significantly reduces film trim waste during the production process.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Skin Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 298 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.2% |

| Market growth 2026-2030 | USD 3205.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.0% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Turkey, Egypt, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The skin packaging market's evolution is fundamentally tied to advances in material science and process engineering. The core technology, vacuum skin packaging, relies on the interplay between high barrier films and sophisticated thermoforming machines or tray sealing machines to achieve a leak-proof seal and superior product shelf life extension.

- Innovations are focused on developing monomaterial films and sustainable packaging materials to address circular economy principles without sacrificing performance metrics like puncture resistance and seal integrity. For boardroom-level strategy, the decision to invest in automated packaging lines with robotic product loading directly impacts operational costs and food safety compliance.

- Adopting these systems can extend the freshness of case-ready proteins by up to twenty days compared to traditional methods. The industry is also seeing a move towards paper-based substrates and peelable lidding films, enhancing premium product presentation for a vertical retail display.

- This shift requires a deep understanding of substrate adhesion and the properties of food contact materials like ethylene vinyl alcohol (EVOH) to maintain an anaerobic environment.

What are the Key Data Covered in this Skin Packaging Market Research and Growth Report?

-

What is the expected growth of the Skin Packaging Market between 2026 and 2030?

-

USD 3.21 billion, at a CAGR of 4.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Material (Plastic films, Paper and paperboard, and Others), Type (Non-carded skin packaging, and Carded skin packaging), Application (Industrial goods, Food, Medical devices, and Durable consumer goods) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Escalating global food waste reduction, Increasing initial capital machinery investment

-

-

Who are the major players in the Skin Packaging Market?

-

Adapa Group, Amcor Plc, Belco Packaging Systems Inc., Coveris Management GmbH, Crawford Packaging, Dow Chemical Co., Faerch AS, G. Mondini SpA, KM Packaging Services Ltd., KP Holding GmbH and Co. KG, Mondi Plc, MULTIVAC SE and Co. KG, ProAmpac Holdings Inc., Rohrer Corp., Sealed Air Corp., SEALPAC International BV, Starview Packaging Machinery Inc, ULMA Packaging Ltd., Winpak Ltd. and Zed Industries Inc.

-

Market Research Insights

- Market dynamics are shaped by a strategic focus on packaging process optimization and brand differentiation strategy. The adoption of case-ready proteins has grown by over 15%, driving demand for solutions that enhance retail shelf appeal and support premium market positioning. This aligns with consumer purchasing behavior favoring transparency and quality.

- However, significant recycling infrastructure challenges persist, with less than 10% of multilayer films being effectively recycled, creating pressure for material science innovation and sustainable sourcing. This dynamic forces operational cost management to balance performance with end-of-life product management. Consequently, new product development is increasingly geared toward hygienic packaging design that also addresses e-commerce packaging requirements and evolving food safety regulations.

We can help! Our analysts can customize this skin packaging market research report to meet your requirements.

RIA -

RIA -