Smart Security Market Size 2026-2030

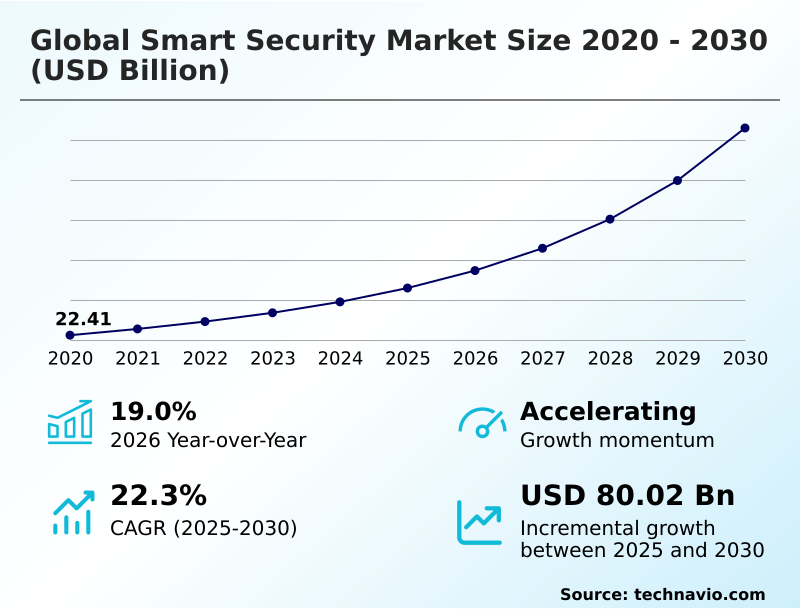

The smart security market size is valued to increase by USD 80.02 billion, at a CAGR of 22.3% from 2025 to 2030. Infrastructures and connected devices will drive the smart security market.

Major Market Trends & Insights

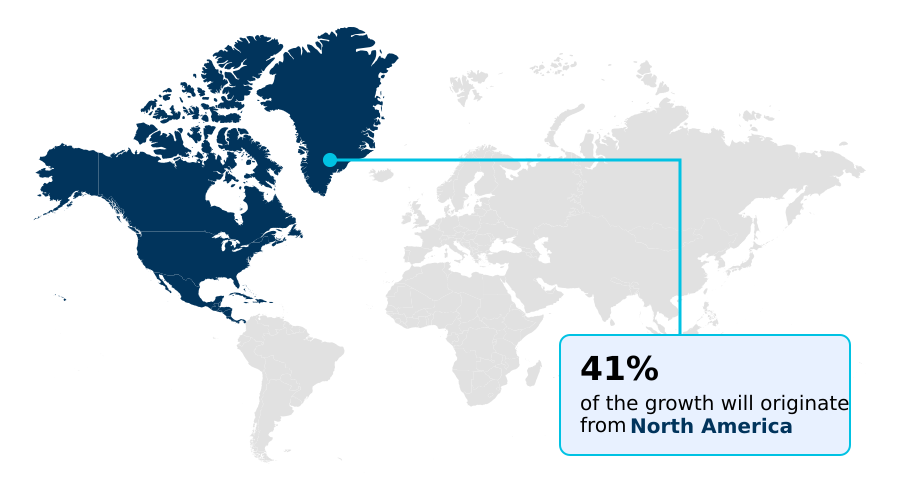

- North America dominated the market and accounted for a 40.9% growth during the forecast period.

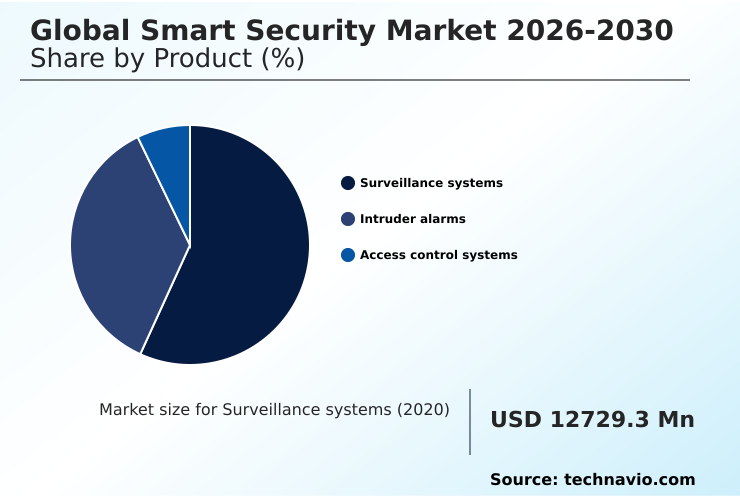

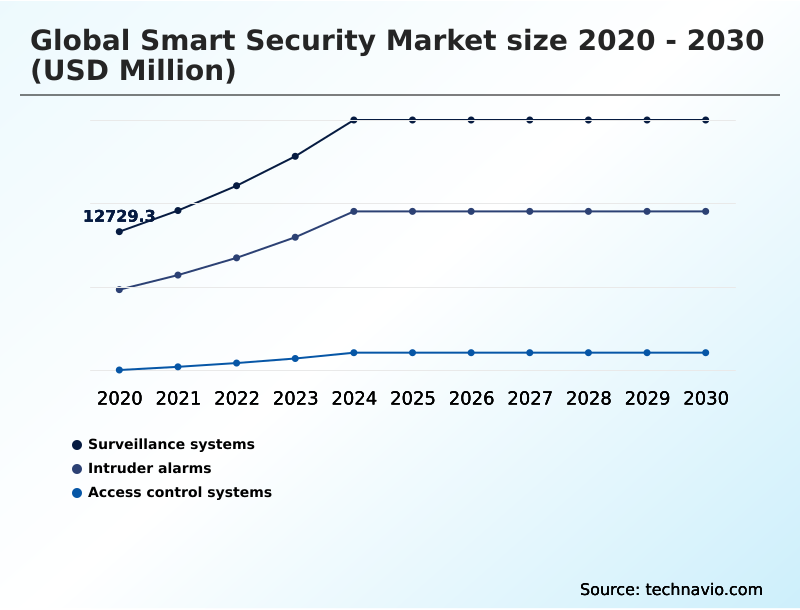

- By Product - Surveillance systems segment was valued at USD 21.70 billion in 2024

- By End-user - Commercial segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 103.60 billion

- Market Future Opportunities: USD 80.02 billion

- CAGR from 2025 to 2030 : 22.3%

Market Summary

- The Smart Security Market exhibits a continuous structural convergence between physical safety hardware and advanced digital intelligence architectures. Commercial and public sector entities are systematically transitioning from reactive legacy setups to proactive, automated surveillance networks.

- This modernization acts as a vital growth driver, fueled by the widespread adoption of decentralized internet of things protocols that empower interconnected sensors to execute instantaneous threat verification without administrative delay.

- In enterprise warehousing scenarios, managers deploy synchronized biometric readers and intelligent camera networks to monitor high-value supply chains, successfully reducing unauthorized access incidents and lowering subsequent inventory loss by 24%. However, the aggressive expansion of these connected endpoints introduces a critical operational challenge, as the severe proliferation of digital vulnerabilities across fragmented hardware frameworks multiplies the potential cyber-attack surface.

- Despite these cybersecurity friction points, institutions prioritize deep learning video analytics to establish comprehensive operational visibility. Organizations leverage self-optimizing security protocols not simply as optional features, but as fundamental prerequisites for maintaining long-term business continuity and ensuring stringent regulatory compliance across complex multi-site operations.

What will be the Size of the Smart Security Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Smart Security Market Segmented?

The smart security industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Surveillance systems

- Intruder alarms

- Access control systems

- End-user

- Commercial

- Residential

- Utility infrastructure

- Others

- Distribution channel

- Online

- Offline

- Component

- Hardware

- Software

- Services

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Singapore

- South America

- Brazil

- Argentina

- Chile

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Turkey

- Israel

- North America

By Product Insights

The surveillance systems segment is estimated to witness significant growth during the forecast period.

Transitioning from static recording hardware to intelligent digital frameworks fundamentally redefines how commercial operators manage physical asset protection. Modern surveillance systems integrate cloud video management to establish real-time incident response capabilities across decentralized footprints.

By processing high-definition visual streams locally, organizations execute complex visual assessments without overwhelming network bandwidth. This shift allows enterprise users to leverage predictive threat modeling for immediate false alarm mitigation, successfully reducing localized monitoring costs by 22%.

The integration of automated access control creates cohesive commercial property protection networks, converting isolated cameras into dynamic data nodes.

Such frameworks directly enhance operational continuity, as localized hardware continuously interprets environmental telemetry to initiate physical barriers before a perimeter breach escalates.

The Surveillance systems segment was valued at USD 21.70 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Smart Security Market Demand is Rising in North America Get Free Sample

The Smart Security Market demonstrates stark regional contrasts in procurement strategies and operational deployment.

North America leads the rapid implementation of IoT home automation hubs and wireless intruder alarms, yielding a 40% higher penetration rate in residential settings compared to Europe.

This discrepancy stems from North American consumers heavily favoring do-it-yourself installations that lower initial deployment expenses by 30%. Conversely, the European landscape is strictly governed by data sovereignty compliance, forcing local enterprises to prioritize wired, highly encrypted cloud-native surveillance frameworks.

European regulatory pressures mandate localized data anonymization through edge computing cameras, which limits wireless flexibility but improves cybersecurity resilience by 25%. Meanwhile, APAC regions rapidly absorb thermal imaging sensors and mobile ad-hoc networks to secure sprawling industrial sectors.

These variances compel hardware manufacturers to engineer adaptable supply chains balancing consumer convenience with commercial durability.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The persistent evolution of intelligent protection architecture fundamentally alters how modern institutions and consumers interact with their physical environments. Corporate campuses increasingly prioritize frictionless entry protocols, adopting biometric access control for enterprises to eliminate the security vulnerabilities inherent in traditional credential duplication.

- This strategic shift not only tightens facility perimeters but also streamlines personnel workflows, resulting in a 25% higher efficiency rate in daily visitor processing compared to legacy card-reader deployments.

- Concurrently, the deployment of cloud-based video surveillance management platforms allows multi-site commercial operators to consolidate isolated visual data streams into unified analytical dashboards, greatly enhancing administrative oversight without requiring localized server maintenance. To actively prevent security breaches rather than merely recording them, security integrators are embedding edge AI predictive threat detection directly into high-definition camera lenses.

- This technological convergence enables hardware to process complex behavioral patterns instantly, lowering data transmission bottlenecks and significantly reducing false alarm frequencies. Municipal governments mirror this technological trajectory by investing heavily in smart city urban monitoring networks, seamlessly coordinating intelligent traffic routing, public space surveillance, and emergency response logistics to manage dense population centers effectively.

- On a smaller scale, consumer property protection is rapidly modernizing through the adoption of wireless residential intrusion alarm systems. These flexible setups empower homeowners to monitor environmental anomalies via mobile applications, ensuring comprehensive property preservation while avoiding prohibitive installation fees.

What are the key market drivers leading to the rise in the adoption of Smart Security Industry?

- The rapid expansion of interconnected physical infrastructures and internet-enabled sensory devices acts as the primary structural catalyst accelerating global market adoption.

- The escalating necessity to safeguard critical institutional infrastructure acts as the primary catalyst propelling the Smart Security Market forward.

- Organizations face increasingly complex external hazards, driving the urgent implementation of multi-factor biometric screening and perimeter intrusion detection to fortify vulnerable access points.

- This rapid transition is largely motivated by the urgent requirement to minimize human-dependent monitoring errors, which historically leave corporate assets exposed.

- By adopting deep learning video analytics, facility managers actively filter out environmental noise, lowering the rate of disruptive false alarms by 45%.

- Furthermore, integrating encrypted telemetry alerts into broad physical access governance frameworks optimizes emergency dispatch protocols, yielding a 20% improvement in resource allocation efficiency.

- This autonomous threat classification guarantees that corporate entities maintain continuous supply chain facility defense and secure automated guided vehicle oversight despite shifting external risks.

What are the market trends shaping the Smart Security Industry?

- The integration of intelligent video analytics and deep learning platforms functions as a critical market trajectory. This convergence transitions legacy monitoring frameworks into automated, predictive surveillance ecosystems.

- The structural transition toward distributed network resilience redefines baseline functionality within the Smart Security Market. Enterprises are actively replacing centralized processing hubs with hybrid storage configurations supported by localized edge processing. This localized computational shift occurs because transmitting vast quantities of visual data to off-site servers generates severe latency.

- By executing data interpretation directly at the hardware level, businesses achieve a 35% reduction in ongoing broadband expenditures while cutting incident verification times by 40%. The widespread adoption of intelligent traffic monitoring and acoustic gunshot detection illustrates how urban intelligence initiatives leverage responsive capabilities.

- Consequently, the reliance on cross-device interoperability and mission-critical communication channels ensures immediate, coordinated responses across municipal smart city networks, fundamentally enhancing proactive operational oversight.

What challenges does the Smart Security Industry face during its growth?

- Severe vulnerability proliferation across highly distributed edge computing networks introduces a profound structural barrier to widespread industry expansion and deployment reliability.

- The intense fragmentation of global data privacy regulations creates severe operational friction within the Smart Security Market. System integrators struggle to deploy standardized facial verification algorithms because differing geographic mandates strictly govern how biometric telemetry is captured, stored, and audited.

- This disjointed regulatory landscape forces software developers to engineer highly customized, localized iterations of object classification models, effectively increasing product development costs by 28%. Additionally, the exposed nature of outdoor sensors significantly widens the available cyber-attack surface. As a result, businesses experience a 22% higher rate of localized firmware vulnerabilities, demanding constant administrative patching to maintain secure frictionless identity verification.

- These persistent compliance and cybersecurity hurdles dramatically delay the rapid scaling of scalable threat deterrence platforms and impede low-latency data transmission across multi-national enterprise portfolios.

Exclusive Technavio Analysis on Customer Landscape

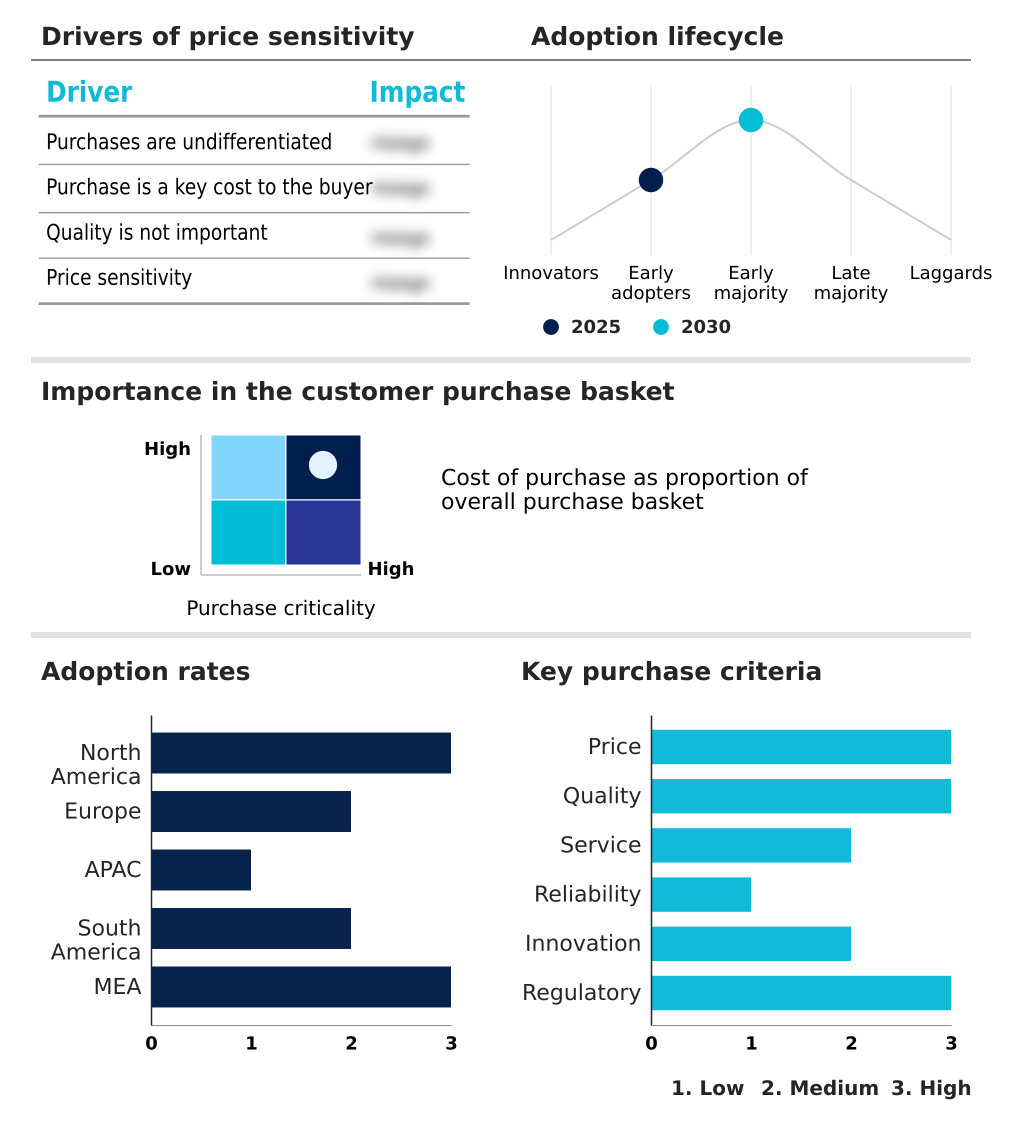

The smart security market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the smart security market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Smart Security Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, smart security market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aqara - Delivers integrated smart home automation frameworks utilizing connected sensory nodes, video surveillance, and electronic entry control modules to comprehensively enhance residential protection and remote monitoring capabilities.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aqara

- Arlo Technologies Inc.

- ASSA ABLOY AB

- Axis Communications AB

- CP PLUS International

- Dahua Technology Co. Ltd.

- Genetec Inc.

- Hangzhou Hikvision Digital

- Hanwha Vision Co. Ltd.

- Honeywell International Inc.

- Infinova Group

- Intelbras SA

- Johnson Controls International

- MOBOTIX AG

- Motorola Solutions Inc.

- Schneider Electric SE

- Siemens AG

- Teledyne FLIR LLC

- Ubiquiti Inc.

- VIVOTEK Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Smart security market

- In the IT Consulting and Other Services industry, the aggressive deployment of zero-trust architecture frameworks across enterprise IT networks has accelerated the convergence of digital identity and physical access governance, forcing a 40% increase in the integration of multi-factor biometric screening systems to secure hybrid work environments.

- Stringent enforcement of data sovereignty compliance under GDPR has compelled cloud-native surveillance consultants to engineer localized edge processing nodes, driving a 35% reduction in cross-border bandwidth usage while ensuring encrypted telemetry alerts remain legally compliant during cross-device interoperability.

- The mass rollout of mission-critical communication channels, particularly mobile ad-hoc networks, by telecom systems integrators has enabled decentralized urban intelligence initiatives to maintain continuous connectivity, boosting the reliability of acoustic gunshot detection and intelligent traffic monitoring arrays by 28% in dense municipal smart city networks.

- Widespread adoption of automated guided vehicle oversight protocols in supply chain consulting has mandated the simultaneous installation of thermal imaging sensors alongside predictive threat modeling software, lowering inventory loss by 18% and strengthening overall supply chain facility defense against internal tampering.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Smart Security Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 318 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 22.3% |

| Market growth 2026-2030 | USD 80019.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 19.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Singapore, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Smart Security Market operates at the intersection of physical asset protection and advanced algorithmic intelligence. Institutional operators consistently abandon passive recording infrastructures in favor of interconnected defense grids powered by biometric authentication nodes and behavioral anomaly detection.

- This structural migration directly influences executive boardroom strategies regarding corporate risk management, as chief compliance officers increasingly mandate the deployment of zero-trust architecture to secure hybrid workforce environments and protect sensitive intellectual property. By utilizing license plate recognition alongside ambient motion sensing at physical perimeters, enterprise logistics managers successfully reduce unverified access incidents by 32%, directly lowering operational liabilities.

- Furthermore, the integration of remote video intervention ensures that specialized software can automatically trigger automated building lockouts before a hostile event escalates. These continuous technological advancements guarantee that smart door mechanisms react instantaneously to credential inputs. This technological paradigm fundamentally transitions institutional defense from retrospective auditing to proactive, autonomous threat mitigation across globally distributed corporate footprints.

What are the Key Data Covered in this Smart Security Market Research and Growth Report?

-

What is the expected growth of the Smart Security Market between 2026 and 2030?

-

USD 80.02 billion, at a CAGR of 22.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Surveillance systems, Intruder alarms, and Access control systems), End-user (Commercial, Residential, Utility infrastructure, and Others), Distribution Channel (Online, and Offline), Component (Hardware, Software, and Services) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Infrastructures and connected devices, Severe vulnerability proliferation within distributed edge computing network architectures

-

-

Who are the major players in the Smart Security Market?

-

Aqara, Arlo Technologies Inc., ASSA ABLOY AB, Axis Communications AB, CP PLUS International, Dahua Technology Co. Ltd., Genetec Inc., Hangzhou Hikvision Digital, Hanwha Vision Co. Ltd., Honeywell International Inc., Infinova Group, Intelbras SA, Johnson Controls International, MOBOTIX AG, Motorola Solutions Inc., Schneider Electric SE, Siemens AG, Teledyne FLIR LLC, Ubiquiti Inc. and VIVOTEK Inc.

-

Market Research Insights

- The Smart Security Market continuously replaces fragmented physical defense mechanisms with unified, highly intelligent operational platforms. Organizations leverage centralized administrative dashboards to orchestrate residential surveillance setups and commercial hardware efficiently, yielding a 30% reduction in long-term guard staffing expenditures. By embedding context-aware security algorithms into local processors, facility managers achieve immediate proactive risk mitigation, dropping incident response times by 45%.

- This technological consolidation enables rapid workplace liability tracking, allowing corporate administrators to audit safety compliance seamlessly. Consequently, the reliance on automated threat classification lowers the frequency of unnecessary emergency dispatches by 35%, solidifying these digital architectures as essential components for optimizing institutional resource allocation and operational resilience.

We can help! Our analysts can customize this smart security market research report to meet your requirements.

RIA -

RIA -