Superalloys Market Size 2026-2030

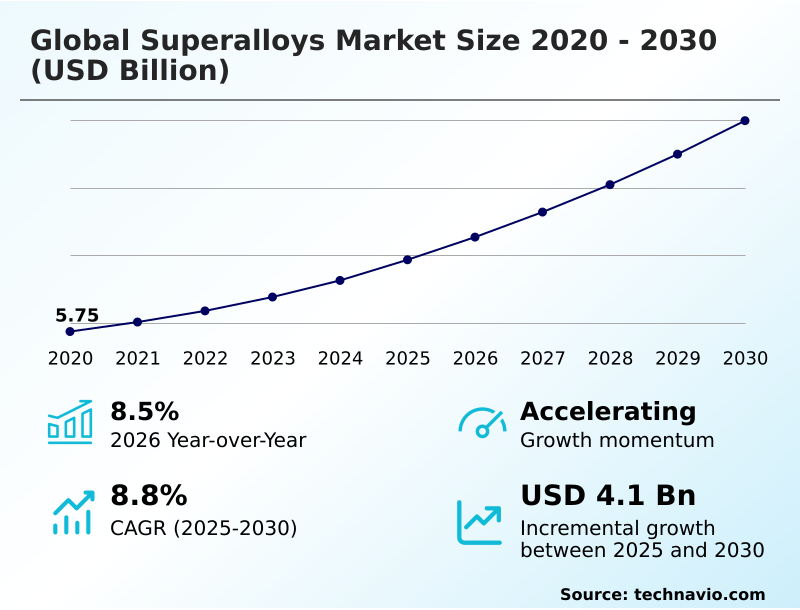

The superalloys market size is valued to increase by USD 4.10 billion, at a CAGR of 8.8% from 2025 to 2030. Resurgence in aerospace defense and commercial aviation fleet modernization will drive the superalloys market.

Major Market Trends & Insights

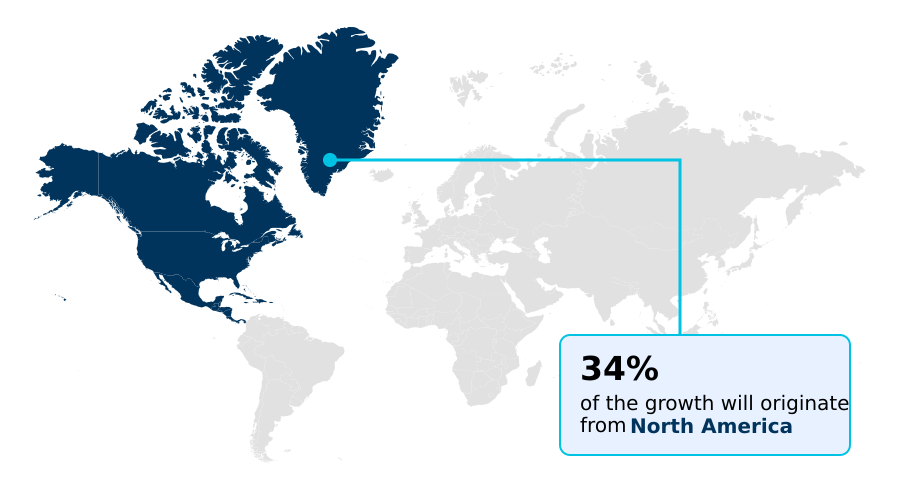

- North America dominated the market and accounted for a 33.5% growth during the forecast period.

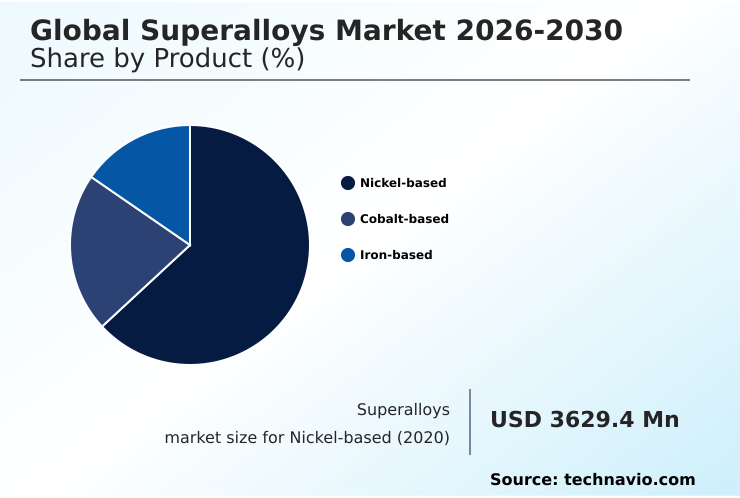

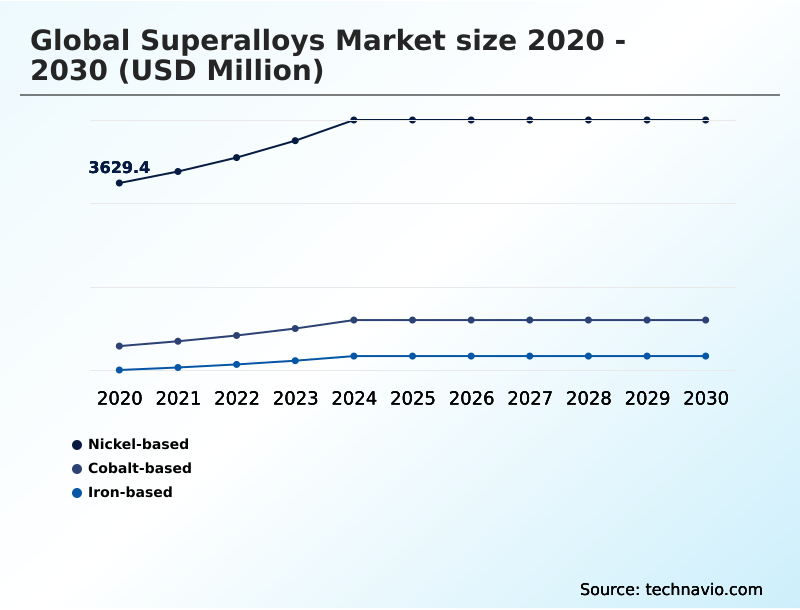

- By Product - Nickel-based segment was valued at USD 4.55 billion in 2024

- By Form Factor - Forged superalloys segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 6.22 billion

- Market Future Opportunities: USD 4.10 billion

- CAGR from 2025 to 2030 : 8.8%

Market Summary

- The superalloys market is defined by a class of metallic materials engineered for superior mechanical strength and stability in extreme thermal environments. Primary demand stems from the aerospace and energy sectors, where materials like nickel-based superalloys and cobalt-based superalloys are essential for the hot-section components of jet engines and industrial gas turbines.

- A key driver is the pursuit of higher thermodynamic efficiency, which requires engines to operate at hotter temperatures, thereby increasing the need for materials with exceptional creep resistance and oxidation resistance. A major trend reshaping the industry is the adoption of additive manufacturing and powder metallurgy, which enables the creation of complex, lightweight parts and reduces material waste.

- For instance, a manufacturer developing new turbine blades must navigate not only the technical qualification of a new wrought alloy but also the geopolitical raw material risk affecting metals like cobalt. This involves significant investment in both R&D and supply chain resilience to ensure production continuity.

- These dynamics are pushing innovation in high-entropy alloys and advanced processing techniques like single-crystal casting to meet future performance demands.

What will be the Size of the Superalloys Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Superalloys Market Segmented?

The superalloys industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Nickel-based

- Cobalt-based

- Iron-based

- Form factor

- Forged superalloys

- Cast superalloys

- Powder metallurgy superalloys

- Application

- Aerospace

- Power generation

- Industrial

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Product Insights

The nickel-based segment is estimated to witness significant growth during the forecast period.

Nickel-based superalloys command a dominant market position, driven by their indispensable role in high-temperature material engineering.

Their exceptional mechanical strength stems from a combination of solid-solution strengthening and the precipitation of a crucial intermetallic phase known as the gamma prime phase, which significantly enhances creep resistance.

This makes them essential for hot-section components in modern jet engines, particularly the high-pressure turbine components like turbine blades that operate under extreme thermal stress.

The continuous push for fuel-efficient engine development relies on these materials to enable higher operating temperatures, directly contributing to thermodynamic efficiency improvement.

Advanced designs incorporate intricate engine component cooling channels, which, combined with superior alloy properties, extend component lifecycles by over 20% in demanding aerospace applications.

The Nickel-based segment was valued at USD 4.55 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Superalloys Market Demand is Rising in North America Get Free Sample

The geographic landscape of the superalloys market is led by North America, which accounts for over 33% of global market activity, driven by a robust aerospace industrial base requiring stringent aerospace material certification for critical rotating parts.

Europe follows, with a strong focus on advanced R&D in areas like advanced coating technologies and materials for nuclear reactor components.

The APAC region is poised for the fastest expansion, with its industrial base growing at a rate 5% higher than mature regions, fueled by indigenous aerospace programs and energy infrastructure projects.

Across these regions, the demand for cobalt-based superalloys and iron-based superalloys is growing for specialized applications.

Advanced processes like directionally solidified casting and hot isostatic pressing are becoming more widespread to improve the oxidation resistance and performance of components used in demanding thermal management systems.

Market Dynamics

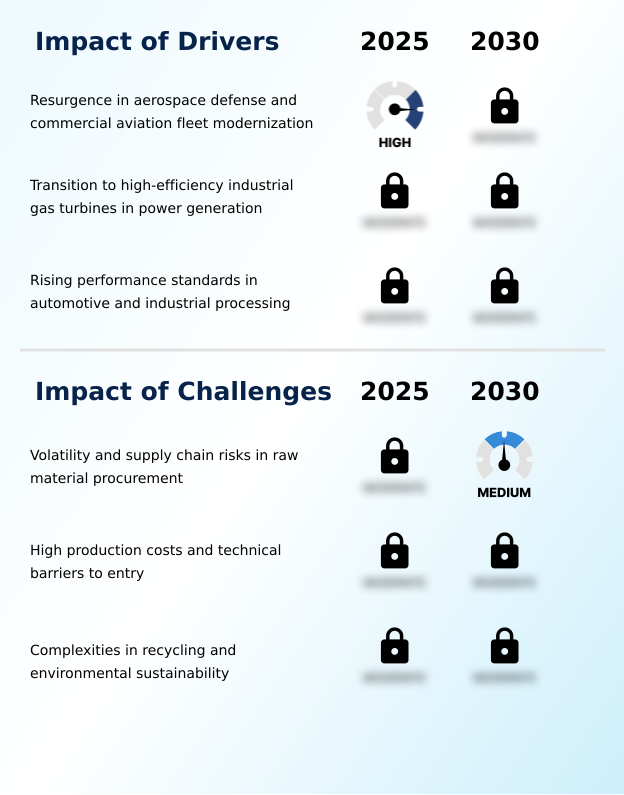

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in high-performance engineering are increasingly focused on complex material and process tradeoffs. The debate over nickel-based vs cobalt-based superalloys continues, with choices depending on specific requirements for corrosion resistance and thermal stability. The rise of additive manufacturing of turbine blades is challenging traditional forged vs cast superalloy properties, offering new design freedoms but also introducing new qualification hurdles.

- For next-generation applications, the focus is shifting toward pioneering materials and methods. The potential of high-entropy alloys for fusion reactors and specialized superalloys for hydrogen fuel turbines represents the forward edge of materials science. Concurrently, the industry is addressing practical challenges, such as the machining challenges of superalloys and defining optimal hot isostatic pressing process parameters to ensure part integrity.

- Understanding the gamma prime phase strengthening mechanism remains crucial for alloy development, especially for enhancing creep resistance at high temperatures. The push for a circular economy intensifies the need for viable recycling processes for superalloy scrap, which can improve raw material cost stability by a factor of two compared to relying on volatile primary markets.

- This is vital for sectors developing superalloys for sour gas service and materials for hypersonic flight, where both performance and supply chain security are paramount.

What are the key market drivers leading to the rise in the adoption of Superalloys Industry?

- A key market driver is the resurgence in aerospace defense modernization programs and the comprehensive renewal of commercial aviation fleets worldwide.

- Market growth is primarily fueled by the performance demands of the aerospace and energy sectors.

- The development of next-generation jet engines and industrial gas turbines, which operate at temperatures 15% higher than previous models, requires materials with superior thermal stability and mechanical strength.

- This has spurred demand for advanced wrought alloy products and innovative hot-gas path components.

- The mechanism of precipitation hardening is being refined to enhance the performance of propulsion system materials, contributing directly to fuel-efficient engine development and overall thermodynamic efficiency improvement.

- This enables a 10% increase in energy output in modern power generation turbine materials. Demand is also growing in the automotive sector for high-performance automotive turbocharger alloys and lightweight structural materials to meet stringent efficiency standards.

What are the market trends shaping the Superalloys Industry?

- The accelerated adoption of additive manufacturing and powder metallurgy signifies a pivotal upcoming trend. This shift is fundamentally altering component design, production capabilities, and material utilization across the industry.

- Key market trends are centered on manufacturing innovation and sustainability. The shift from traditional investment casting and forging processes to additive manufacturing is enabling the creation of components with intricate internal engine component cooling channels, improving thermal efficiency by over 15%.

- This adoption of powder metallurgy also helps produce near-net-shape components, reducing material waste by up to 60% compared to conventional methods. In parallel, a focus on sustainable superalloy production is driving the development of a circular economy in metallurgy. This is leading to advanced next-generation alloy development, including new intermetallic phase chemistries and advanced alloy compositions.

- Innovations in single-crystal casting continue to push the boundaries of what is possible in material innovation for engines, enhancing performance for the most demanding applications.

What challenges does the Superalloys Industry face during its growth?

- A significant challenge affecting market growth arises from the price volatility and logistical risks inherent in the global supply chain for critical raw materials.

- The market faces significant challenges related to supply chain stability and manufacturing costs. The geopolitical raw material risk associated with key elements creates price volatility, where costs can fluctuate by as much as 40% in a single year, complicating financial planning.

- Establishing effective closed-loop recycling programs is a major hurdle, with current processes for reverted scrap struggling to achieve high yields, meaning less than 30% of end-of-life material is reclaimed into high-value products. The high cost of advanced processes like vacuum induction melting and vacuum arc remelting acts as a barrier to entry.

- Furthermore, the threat from substitutes like ceramic matrix composites and titanium aluminides is growing in niche applications, compelling innovation in conventional alloys to maintain superior corrosion resistance and performance in high-pressure environments, particularly for deep-water oil exploration materials.

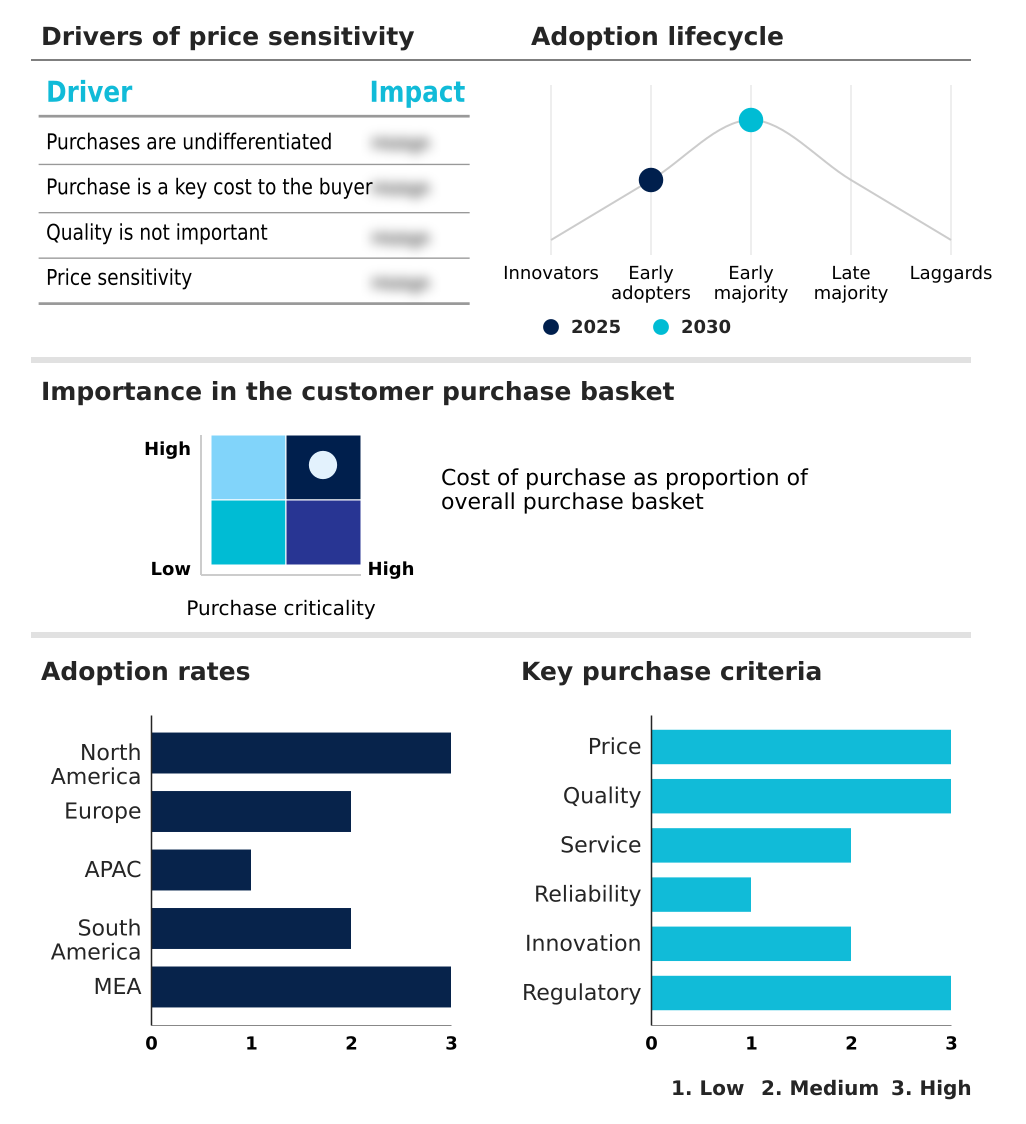

Exclusive Technavio Analysis on Customer Landscape

The superalloys market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the superalloys market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Superalloys Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, superalloys market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acerinox SA - Delivers advanced nickel- and cobalt-based superalloys, forged products, and powder metals engineered for critical jet engine and defense system applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acerinox SA

- Allegheny Technologies Inc.

- Alleima AB

- AMETEK Inc.

- Aperam SA

- Aubert and Duval

- Baosteel Group Corp.

- CANNON MUSKEGON Corp.

- Carpenter Technology Corp.

- Daido Steel Co. Ltd.

- Doncasters Group Ltd.

- Fushun Special Steel Co.,LTD

- Howmet Aerospace Inc.

- IHI Corp.

- MetalTek International

- Precision Castparts Corp.

- Proterial Ltd.

- Rolled Alloys Inc.

- Sunflag Iron and Steel Co. Ltd

- voestalpine AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Superalloys market

- In August 2025, IMDEA Materials Institute introduced a scalable methodology to control microstructure in LPBF-processed nickel-based superalloys, boosting industrial adoption of additive manufacturing for high-temperature uses.

- In July 2025, Hindustan Aeronautics Ltd. (HAL) awarded a superalloy procurement contract valued at approximately $70 million to Mishra Dhatu Nigam Ltd. (MIDHANI) to support its manufacturing programs.

- In January 2025, the U.S. National Science Foundation announced a new processing technique that allows superalloys to maintain exceptional wear resistance at near-forging temperatures, expanding their operational range.

- In October 2025, Karlsruher Institut fur Technologie (KIT) unveiled a new chromium molybdenum silicon alloy demonstrating high-temperature ductility and oxidation resistance, positioning it as a potential alternative to nickel-based superalloys.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Superalloys Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 298 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.8% |

| Market growth 2026-2030 | USD 4102.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The superalloys market is fundamentally driven by the relentless pursuit of performance in extreme environments. Materials are defined by their processing route, from vacuum induction melting and vacuum arc remelting of raw materials to produce ingots, which are then subjected to forging processes or used in investment casting.

- The evolution toward powder metallurgy and advanced methods like single-crystal casting, equiaxed casting, and directionally solidified casting allows for the creation of near-net-shape components with optimized properties. The core technical challenge is balancing mechanical strength with thermal stability, creep resistance, and both corrosion resistance and oxidation resistance.

- This is achieved through microstructural control, involving precipitation hardening via the gamma prime phase or carbide precipitation, and solid-solution strengthening with refractory metals. Applications for these materials, from turbine blades in jet engines and industrial gas turbines to sour-service alloys and hot-gas path components, are expanding.

- For boardroom consideration, the strategic pivot to additive manufacturing is critical; while capital-intensive, it can shorten the development-to-deployment cycle for new components by up to 40%, a decisive competitive advantage. This contrasts with legacy investments in producing wrought alloy or managing reverted scrap.

What are the Key Data Covered in this Superalloys Market Research and Growth Report?

-

What is the expected growth of the Superalloys Market between 2026 and 2030?

-

USD 4.10 billion, at a CAGR of 8.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Nickel-based, Cobalt-based, and Iron-based), Form Factor (Forged superalloys, Cast superalloys, and Powder metallurgy superalloys), Application (Aerospace, Power generation, and Industrial) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Resurgence in aerospace defense and commercial aviation fleet modernization, Volatility and supply chain risks in raw material procurement

-

-

Who are the major players in the Superalloys Market?

-

Acerinox SA, Allegheny Technologies Inc., Alleima AB, AMETEK Inc., Aperam SA, Aubert and Duval, Baosteel Group Corp., CANNON MUSKEGON Corp., Carpenter Technology Corp., Daido Steel Co. Ltd., Doncasters Group Ltd., Fushun Special Steel Co.,LTD, Howmet Aerospace Inc., IHI Corp., MetalTek International, Precision Castparts Corp., Proterial Ltd., Rolled Alloys Inc., Sunflag Iron and Steel Co. Ltd and voestalpine AG

-

Market Research Insights

- The market is shaped by a dynamic interplay between performance demands and operational sustainability. The development of advanced coating technologies extends the service life of hot-section components by up to 30%, a crucial factor for aerospace material certification.

- Simultaneously, the push toward net-zero carbon emission goals is accelerating R&D into lightweight structural materials, which has already led to a 15% reduction in the weight of certain propulsion system materials without compromising performance. This focus on material innovation for engines addresses both fuel-efficient engine development and the need for durable automotive turbocharger alloys.

- As companies refine their thermal management systems, they are also navigating complex geopolitical raw material risk, balancing material sourcing with performance requirements for next-generation systems.

We can help! Our analysts can customize this superalloys market research report to meet your requirements.

RIA -

RIA -