Temperature Controlled Pharmaceutical Packaging Solutions Market Size and Growth Forecast 2025-2029

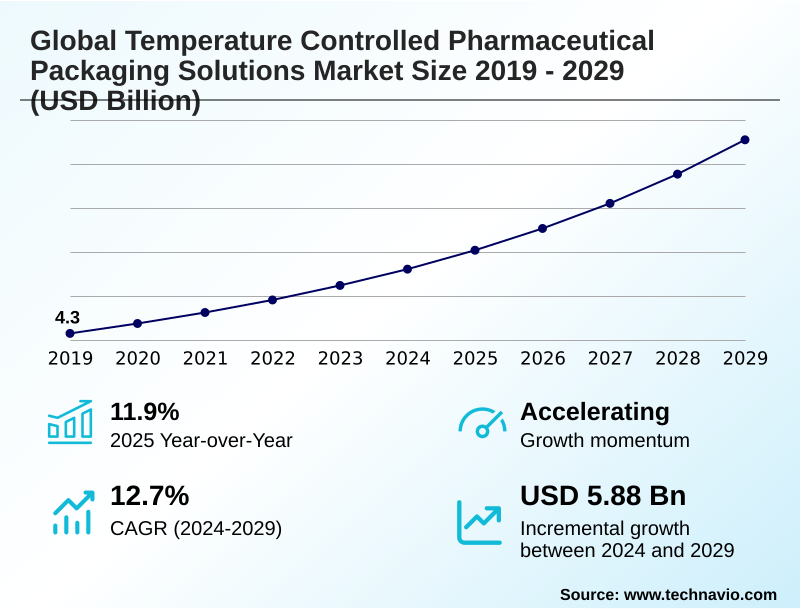

The Temperature Controlled Pharmaceutical Packaging Solutions Market size was valued at USD 7.22 billion in 2024 growing at a CAGR of 12.7% during the forecast period 2025-2029.

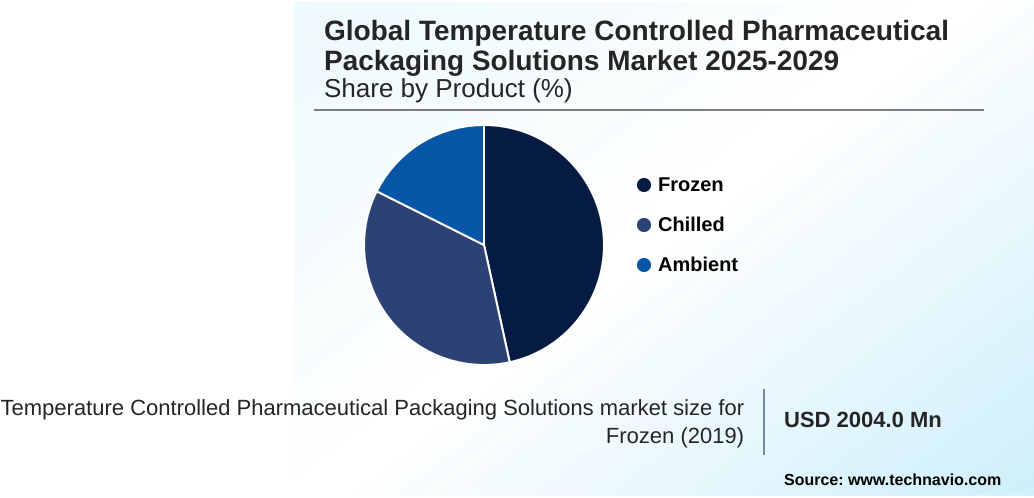

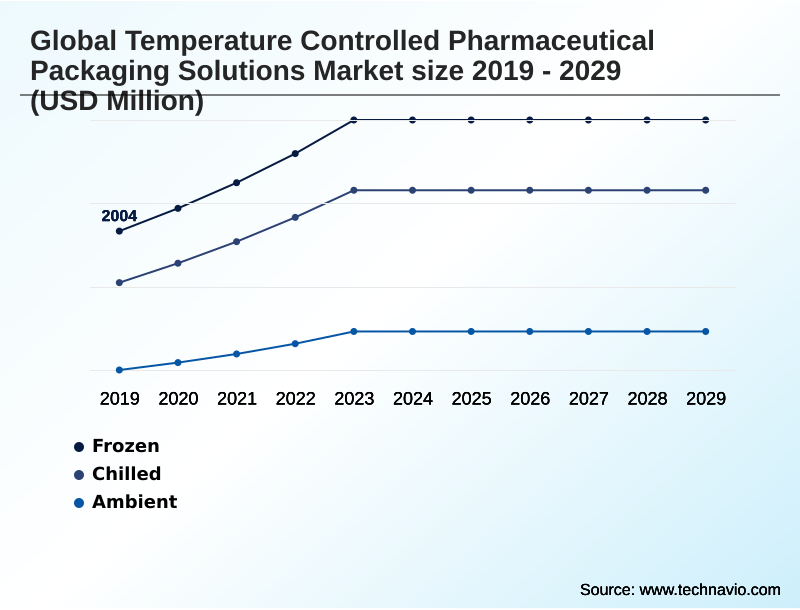

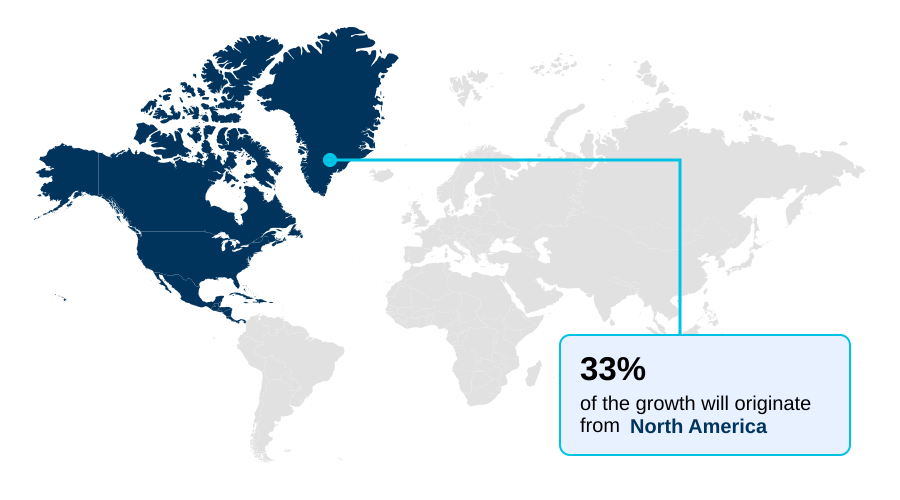

North America accounts for 32.9% of incremental growth during the forecast period. The Frozen segment by Product was valued at USD 3.00 billion in 2023, while the Passive systems segment holds the largest revenue share by Type.

The market is projected to grow by USD 8.80 billion from 2019 to 2029, with USD 5.88 billion of the growth expected during the forecast period of 2024 to 2029.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Temperature Controlled Pharmaceutical Packaging Solutions Market Overview

The temperature controlled pharmaceutical packaging solutions market is expanding, driven by the proliferation of biologics and advanced treatments requiring strict thermal control. Maintaining supply chain integrity for these products is paramount, with a significant portion of North America's market activity, contributing to 32.9% of the incremental growth, linked to advanced clinical trial logistics. In a typical scenario, a biopharmaceutical firm transporting cell therapies leverages validated shipping solutions integrated with IoT data loggers for real-time temperature excursion monitoring. This deployment of cold chain visibility platforms ensures compliance with Good Distribution Practices (GDP) and has been shown to reduce product loss rates during transit significantly. The industry's year-over-year growth of 11.9% is further supported by the rising adoption of reusable packaging systems, as decision-makers weigh the total cost of ownership against single-use alternatives to meet both operational and sustainability goals.

Drivers, Trends, and Challenges in the Temperature Controlled Pharmaceutical Packaging Solutions Market

The increasing complexity of pharmaceutical products is fundamentally shaping procurement decisions for temperature-controlled packaging. For instance, the logistics for vaccines and biologics demand robust solutions, with decision-makers conducting detailed cost-benefit analyses of reusable vs single-use shippers. Reusable cold chain packaging solutions offer a lower total cost of ownership over time, a crucial factor for large-scale distribution.

The expansion of cell and gene therapies necessitates specialized packaging solutions for cell and gene therapies that can maintain cryogenic temperatures, often requiring active temperature controlled cargo containers for air freight. These systems provide precise thermal management, which is critical for complying with the EU's Good Distribution Practices (GDP) guidelines.

In contrast, for less sensitive products or shorter transit routes, passive temperature controlled shipping systems offer a cost-effective and reliable alternative.

A key operational scenario involves a logistics manager for a global pharmaceutical firm selecting validated packaging for clinical trial logistics; for a cross-continental shipment of a high-value biologic, an active container is chosen, while for regional distribution of a stable vaccine, a pre-qualified passive shipper is deemed sufficient, demonstrating a tiered approach to risk management and cost control.

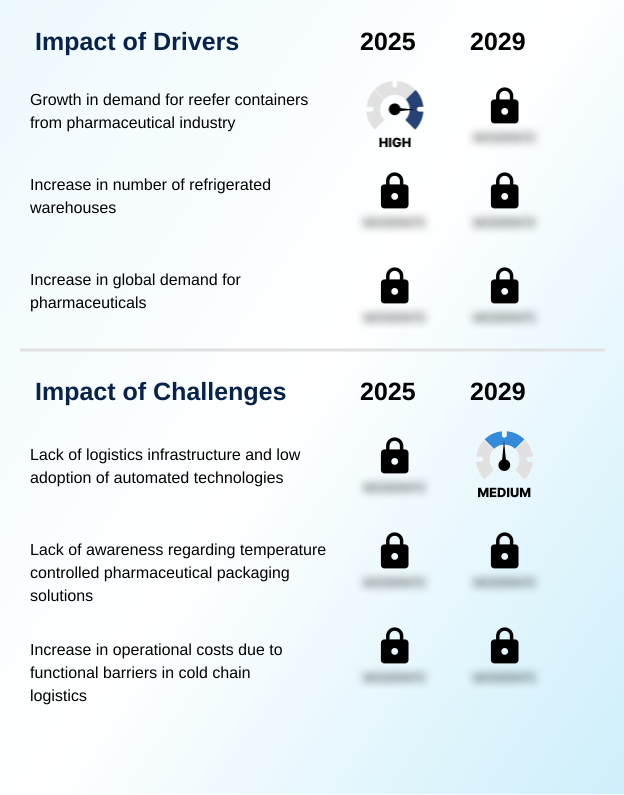

Primary Growth Driver: The increasing demand for reefer containers from the pharmaceutical industry is a significant driver for the market.

The primary driver of market growth is the expanding pipeline of biologic drugs and other temperature-sensitive pharmaceuticals, which require stringent cold chain logistics to maintain efficacy.

The transport of these products, including the recent surge in GLP-1 agonists, necessitates reliable solutions that adhere to global Good Distribution Practices (GDP) standards.

This demand has led to significant investments in logistics infrastructure, such as the expansion of reefer container fleets by major shipping lines. For instance, one such expansion added over 13,000 new units to enhance capacity for biologic drug transport.

The complexity of moving these high-value products across global supply chains makes validated, temperature-controlled packaging an essential component of modern pharmaceutical distribution.

Emerging Market Trend: Market participants are increasingly focusing on traditional growth strategies, particularly mergers and acquisitions. This approach is used to expand product portfolios and enhance geographic reach.

A significant trend shaping the market is the strategic consolidation through mergers and acquisitions, enabling companies to broaden their portfolios of reusable packaging systems and expand their global footprint. This inorganic growth strategy is complemented by a strong industry-wide push toward sustainable cold chain packaging to address environmental concerns and meet corporate responsibility goals.

This shift is driving innovation in materials and design, aligning with environmental management standards such as ISO 14001. As a result, there is growing demand for solutions that not only ensure supply chain integrity but also support a circular economy.

The focus on sustainability is becoming a key differentiator among vendors and a critical factor in procurement decisions for logistics and pharmaceutical partners.

Key Industry Challenge: Inadequate logistics infrastructure and the slow adoption of automated technologies present a key challenge to market growth.

A primary market restraint is the inadequate logistics infrastructure and high operational costs in many emerging economies, which complicates the last-mile cold chain. Reports indicate that up to 20% of temperature-sensitive products are damaged due to broken cold chains in these regions, leading to significant financial losses and patient risk.

The lack of robust cold chain visibility platforms makes temperature excursion monitoring difficult, hindering compliance with standards like the BRC Global Standard for Packaging Materials.

The high initial investment required for advanced automated technologies and qualified packaging presents a significant barrier for smaller domestic logistics providers, slowing the modernization of the supply chain and limiting the market's full growth potential in these key geographic areas.

Explore Full Market Dynamics Analysis Request Free Sample

Temperature Controlled Pharmaceutical Packaging Solutions Market Segmentation

The temperature controlled pharmaceutical packaging solutions industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

Product Segment Analysis

The frozen segment is estimated to witness significant growth during the forecast period.

The frozen segment is critical for safeguarding product efficacy during extended transit, particularly for therapies requiring cryogenic temperatures. Operational priorities center on advanced thermal insulation and active temperature regulation to comply with evolving regulatory frameworks like Good Distribution Practices (GDP).

Innovations in phase change materials and vacuum insulation panels are utilized to minimize temperature excursions and preserve the integrity of high-value formulations.

This segment, which accounted for a substantial portion of the market in 2024, sees continuous development in modular and scalable ultra-low temperature shipping solutions.

These advancements are essential for supporting last-mile delivery and ensuring performance consistency for temperature-sensitive pharmaceuticals across global supply chains, reinforcing the segment’s integral role in sustaining product accessibility.

The Frozen segment was valued at USD 3.00 billion in 2023 and showed a gradual increase during the forecast period.

Temperature Controlled Pharmaceutical Packaging Solutions Market by Region: North America Leads with 32.9% Growth Share

North America is estimated to contribute 32.9% to the growth of the global market during the forecast period.

The geographic landscape is led by North America, which accounts for approximately 32.9% of the market's incremental growth, driven by its advanced healthcare infrastructure and high concentration of pharmaceutical R&D.

The US market, in particular, benefits from initiatives like the Pharmaceutical Supply Chain Security Act (PSCSA), which bolsters demand for secure and traceable clinical trial logistics.

Meanwhile, APAC is the fastest-growing region, with countries like China and India expanding their pharmaceutical manufacturing capabilities, creating significant demand for multi-modal transport validation and compliant packaging solutions.

Europe, with Germany as a key market, remains a significant contributor, focusing on sustainable cold chain packaging and adherence to stringent EU Good Distribution Practices.

These regional dynamics highlight a global market where regulatory compliance in shipping and robust infrastructure are key differentiators.

Customer Landscape Analysis for the Temperature Controlled Pharmaceutical Packaging Solutions Market

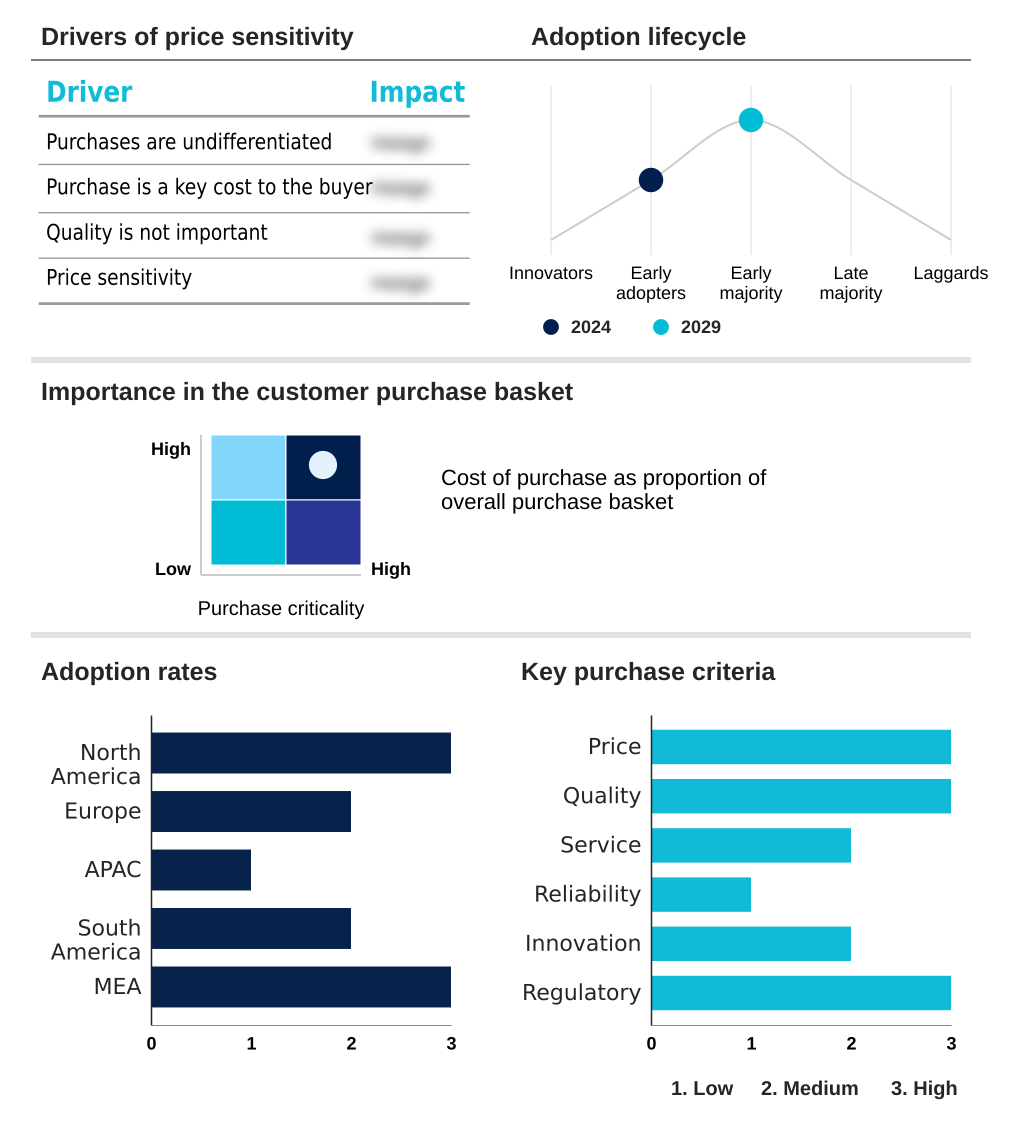

The temperature controlled pharmaceutical packaging solutions market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the temperature controlled pharmaceutical packaging solutions market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Temperature Controlled Pharmaceutical Packaging Solutions Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the temperature controlled pharmaceutical packaging solutions market industry.

Aeris Dynamics - Vendors provide advanced, qualified shipping containers and logistics services, ensuring the integrity and efficacy of temperature-sensitive pharmaceuticals and biologics throughout the global supply chain.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aeris Dynamics

- American Aerogel

- Cencora Inc.

- Cold Chain Technologies

- Cryo Store B.V.

- CSafe Global

- DGP Intelsius Ltd.

- DoKaSch GmbH

- DS Smith Plc

- Envirotainer AB

- FUCHS SE

- Hazgo

- Inmark Global Holdings LLC.

- Integreon Global

- Pelican Products Inc.

- Rapid Aid Corp.

- Sofrigam

- Sonoco Products Co.

- va Q tec Thermal Solutions GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Temperature Controlled Pharmaceutical Packaging Solutions Market

- In January 2025, CSafe completes its acquisition of Kalibox, a French manufacturer of passive temperature-controlled packaging, to expand its product portfolio and European geographic footprint.

- In March 2025, Hapag-Lloyd announces the full deployment of 13,420 new reefer containers, including 1,000 units with controlled-atmosphere technology, to enhance its capacity for transporting sensitive goods like pharmaceuticals.

- In November 2024, Cryoport Inc. initiates a strategic partnership with Syneos Health to provide its full suite of temperature-controlled logistics solutions for decentralized and direct-to-patient clinical trials.

- In September 2024, Pelican Products Inc. launches its new CoolPall Flex PCM line, a series of reusable shippers designed to improve sustainability in the transport of biologic drugs.

Research Analyst Overview: Temperature Controlled Pharmaceutical Packaging Solutions Market

Boardroom decisions are increasingly focused on the total cost of ownership of cold chain assets, weighing the high CAPEX of reusable packaging systems against the recurring OPEX of single-use shippers. This evaluation is critical as the market shifts toward more sustainable and efficient biologic drug transport.

The integrity of temperature-sensitive pharmaceuticals relies on sophisticated thermal packaging, with passive cooling systems that use advanced phase change materials and vacuum insulation panels dominating market share. However, for high-value cell and gene therapy logistics requiring precise cryogenic temperatures, active cooling systems are indispensable. Compliance with standards like ASTM D4169 for shipping container performance is a non-negotiable vendor qualification criterion.

As such, procurement managers are prioritizing validated shipping solutions that integrate real-time data loggers for temperature excursion monitoring, providing an auditable trail for regulatory bodies and ensuring supply chain integrity from production to patient.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Temperature Controlled Pharmaceutical Packaging Solutions Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 251 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.7% |

| Market growth 2025-2029 | USD 5882.4 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 11.9% |

| Key countries | US, Canada, Germany, UK, France, Italy, China, India, Japan, Brazil, Argentina, Saudi Arabia, UAE and South Africa |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Temperature Controlled Pharmaceutical Packaging Solutions Market: Key Questions Answered in This Report

-

What is the expected growth of the Temperature Controlled Pharmaceutical Packaging Solutions Market between 2025 and 2029?

-

The Temperature Controlled Pharmaceutical Packaging Solutions Market is expected to grow by USD 5.88 billion during 2025-2029, registering a CAGR of 12.7%. Year-over-year growth in 2025 is estimated at 11.9%%. This acceleration is shaped by growth in demand for reefer containers from pharmaceutical industry, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Frozen, Chilled, and Ambient), Type (Passive systems, and Active systems), End-user (Pharmaceuticals, Vaccines and biologics, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa). Among these, the Frozen segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2019-2023 and forecasts through 2029 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, South America and Middle East and Africa. North America is estimated to contribute 32.9% to market growth during the forecast period. Country-level analysis includes US, Canada, Germany, UK, France, Italy, China, India, Japan, Brazil, Argentina, Saudi Arabia, UAE and South Africa, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is growth in demand for reefer containers from pharmaceutical industry, which is accelerating investment and industry demand. The main challenge is lack of logistics infrastructure and low adoption of automated technologies, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2025 and 2029 with comparative analysis.

-

-

Who are the major players in the Temperature Controlled Pharmaceutical Packaging Solutions Market?

-

Key vendors include Aeris Dynamics, American Aerogel, Cencora Inc., Cold Chain Technologies, Cryo Store B.V., CSafe Global, DGP Intelsius Ltd., DoKaSch GmbH, DS Smith Plc, Envirotainer AB, FUCHS SE, Hazgo, Inmark Global Holdings LLC., Integreon Global, Pelican Products Inc., Rapid Aid Corp., Sofrigam, Sonoco Products Co. and va Q tec Thermal Solutions GmbH. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Temperature Controlled Pharmaceutical Packaging Solutions Market Research Insights

Market dynamics are increasingly shaped by the need for multi-modal transport validation to ensure supply chain integrity across complex global routes. As the APAC market demonstrates accelerated growth compared to Europe, with regional CAGRs of 13.1% and 12.3% respectively, logistics providers are investing in advanced insulation materials and cold chain qualification to manage diverse climatic conditions.

Compliance with mandates such as Good Distribution Practices (GDP) necessitates robust temperature management, particularly for patient-centric logistics where direct-to-patient shipments bypass traditional distribution hubs. An operational focus on secure logistics for high-value drugs is driving the adoption of real-time temperature tracking technologies, providing auditable proof of product stability from the manufacturing site to the point of administration.

We can help! Our analysts can customize this temperature controlled pharmaceutical packaging solutions market research report to meet your requirements.

RIA -

RIA -