Thickeners Market Size 2024-2028

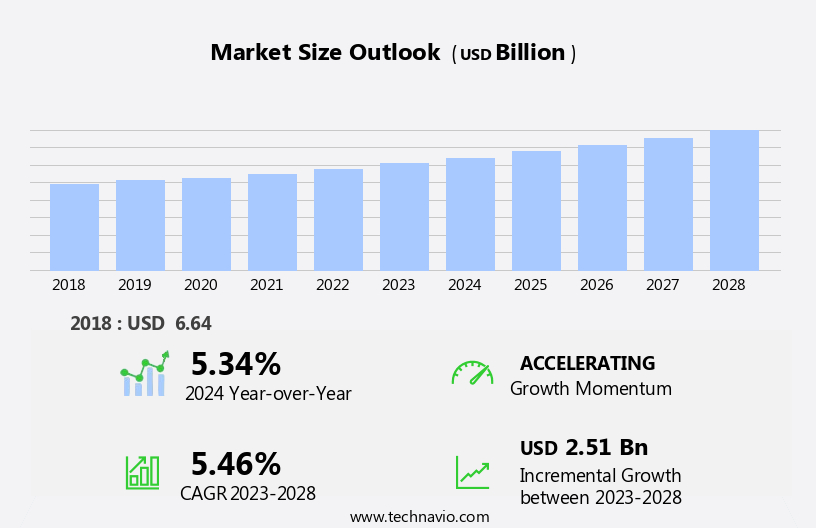

The thickeners market size is forecast to increase by USD 2.51 billion, at a CAGR of 5.46% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing demand for sustainable and natural thickeners in various industries. This shift in consumer preferences is leading manufacturers to invest heavily in research and development to produce eco-friendly and efficient thickening solutions. Technological advancements in thickener manufacturing are also playing a pivotal role in market expansion, enabling the production of high-performance thickeners with improved functionality and cost-effectiveness. However, the market faces challenges from the fluctuation in prices of raw materials used in thickener production. These price fluctuations can significantly impact the profitability of manufacturers and require strategic planning to mitigate risks and maintain competitiveness.

- Companies must closely monitor raw material prices and explore alternative sourcing strategies to ensure a steady supply and stable costs. To capitalize on market opportunities and navigate challenges effectively, businesses should focus on innovation, sustainability, and operational efficiency. By investing in R&D, optimizing production processes, and collaborating with suppliers, they can differentiate themselves and stay ahead of the competition.

What will be the Size of the Thickeners Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by the diverse applications across various sectors. These essential additives exhibit shear thinning behavior, allowing them to adjust their viscosity in response to applied shear stress. Food grade thickeners, such as guar gum, play a crucial role in viscosity modification, enhancing the texture and consistency of food products. In the pharmaceutical industry, thickeners are employed for emulsion stabilization, ensuring suspension stability and prolonging shelf life. Particle dispersion is another significant application, where thickeners facilitate the uniform distribution of solids in liquid thickeners.. Thixotropic properties enable thickeners to maintain their structure under rest conditions, preventing syneresis and ensuring product quality.

Pharmaceutical and industrial thickeners serve various purposes, including process optimization and rheological property control. Starch-based thickeners and cellulose derivatives are commonly used due to their cost-effectiveness and versatility. However, polymer thickening agents offer superior performance in terms of temperature and pH stability. The ongoing research and development efforts focus on enhancing the functionality of thickeners, such as improving flow behavior index, optimizing concentration effects, and mitigating ionic strength and temperature effects. The market is a dynamic and ever-evolving landscape, with continuous innovation and advancements shaping its future applications.

How is this Thickeners Industry segmented?

The thickeners industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Organic

- Inorganic

- End-user

- Building and construction

- Automotive

- Packaging

- Others

- Source

- Plant-Based (Guar Gum, Xanthan Gum)

- Animal-Based (Gelatin)

- Microbial

- Synthetic

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- UK

- Middle East and Africa

- UAE

- APAC

- China

- India

- Indonesia

- Japan

- Malaysia

- South Korea

- Thailand

- South America

- Brazil

- Rest of World (ROW)

- North America

By Type Insights

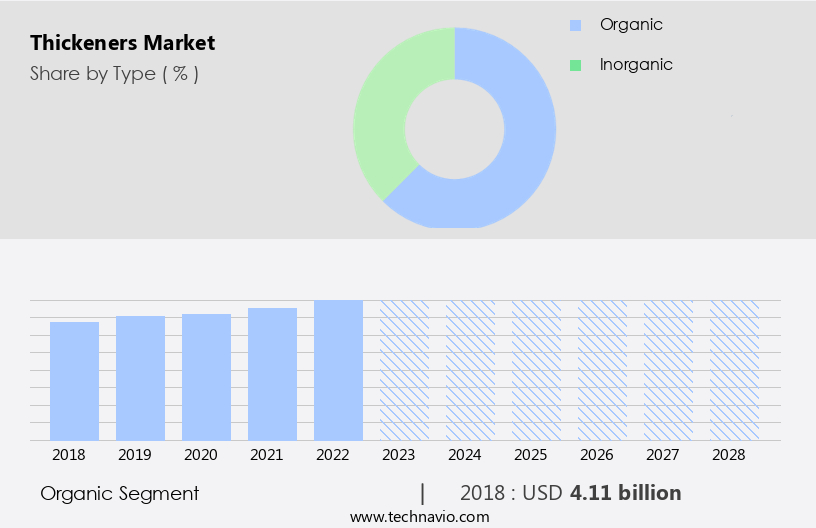

The organic segment is estimated to witness significant growth during the forecast period.

Organic thickeners, derived from natural sources such as cellulosic materials, polyacellulose, and polyurethanes, are gaining popularity due to their sustainability and reduced environmental impact. These materials can be processed and modified to achieve desirable rheological properties, making them suitable for various applications. Cellulosic ethers, like hydroxypropyl methylcellulose (HPMC) and carboxymethyl cellulose (CMC), are water-soluble polymers derived from cellulose. They are extensively used in industries for their ability to modify the viscosity and stability of liquids. HPMC and CMC exhibit thixotropic properties, which allow them to maintain a stable structure under rest but flow easily when agitated.

They are effective in preventing syneresis, a problem where a gel or suspension separates from the liquid. In food applications, these thickeners are used for viscosity modification and texture enhancement, particularly in the production of ice cream and sauces. Pharmaceutical industries rely on these thickeners for emulsion stabilization and suspension stability, ensuring the uniformity and quality of their products. In industrial applications, they are used for process optimization, improving flow behavior and reducing sedimentation. The thickening agents' performance is influenced by factors such as concentration, pH, temperature, and ionic strength. Starch-based thickeners and cellulose derivatives are other classes of organic thickeners that offer advantages such as cost-effectiveness and ease of use.

Xanthan gum, a microbial polysaccharide, is another popular thickener due to its high viscosity and shear thinning behavior, making it suitable for applications where a pourable consistency is required. Rheometer testing is used to evaluate the thickeners' performance, ensuring consistency and quality in various applications. Proper quality control testing is essential to maintain the desired rheological properties and shelf life extension.

The Organic segment was valued at USD 4.11 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

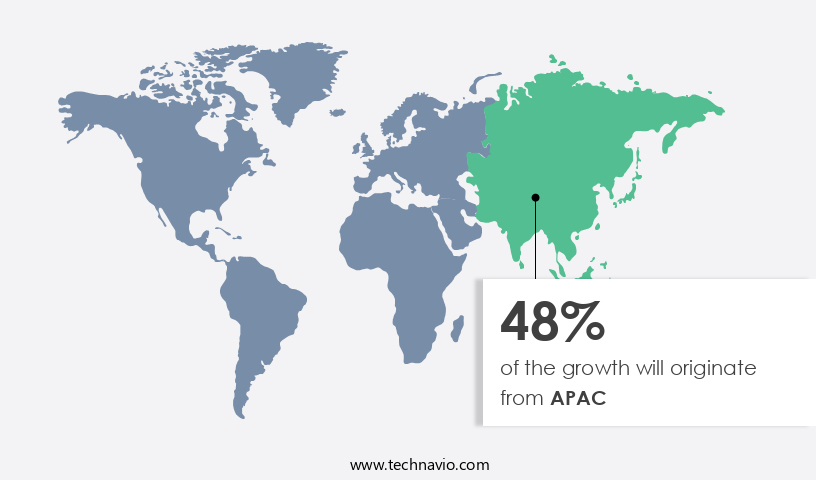

APAC is estimated to contribute 48% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the dynamic and evolving market for thickeners, various entities play significant roles in shaping trends and driving demand. Yield stress measurement and rheological properties are crucial factors influencing the selection and application of thickeners in industries. PH effects and concentration can impact the consistency coefficient and viscosity modification. Thixotropic properties and syneresis prevention are essential for maintaining desired texture and preventing separation in applications. Application methods vary, with quality control testing ensuring product consistency and compliance. Shear thinning behavior is a critical consideration for industrial thickeners, while food grade thickeners are essential for the food industry. Thickeners enhance performance and functionality in various sectors, including pharmaceuticals for emulsion stabilization, suspension stability, and shelf life extension.

Process optimization through the use of starch-based thickeners, cellulose derivatives, and polymer thickening agents is a focus for manufacturers. Ionic strength and temperature effects can impact thickener performance, necessitating careful consideration. Xanthan gum properties, including gelation mechanism and storage stability, are vital for specific applications. In the APAC region, population growth and urbanization fuel demand for thickeners in industries such as textiles, paints, and coatings. Rising disposable incomes and consumer spending on automobile, building, and construction sectors further boost demand. Rapid industrial development in countries like China and India, particularly in paints and coatings, textiles, and adhesives, underlines the importance of thickeners in regional growth.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Thickeners Industry?

- The market's growth is primarily attributed to the rising demand for sustainable and natural thickeners, making their use a key market trend.

- The market is witnessing significant growth due to the increasing demand for sustainable alternatives in various industries, particularly in paints and coatings. Natural thickeners, derived from renewable resources such as plants, starches, or cellulose, are gaining popularity due to their biodegradable and environmentally friendly properties. These alternatives offer comparable or superior performance to traditional thickeners derived from petrochemical sources. Strict regulations, such as the REACH regulation, which aims to ensure the safe use of chemicals while protecting human health and the environment, have prompted manufacturers to seek greener alternatives. The rheological properties of thickeners, including yield stress measurement, consistency coefficient, and thixotropic properties, significantly impact the performance of paints and coatings.

- Concentration effects and pH effects are also crucial factors in determining the suitability of thickeners for specific applications. Syneresis prevention is another essential consideration in the selection of thickeners. Application methods and quality control testing are vital aspects of the market, ensuring the consistent production of high-quality products. Understanding the rheological properties and their effects on the final product is crucial for manufacturers to optimize their formulations and meet the evolving demands of consumers and regulations.

What are the market trends shaping the Thickeners Industry?

- The trend in the market points towards advancements in thickener manufacturing technology. This sector is experiencing significant growth and innovation.

- Advancements in technology are driving the evolution of thickeners, particularly in the extraction processes for natural options. Innovations such as enzymatic extraction and advanced filtration technologies are enhancing efficiency and reducing costs. Academic institutions and research laboratories are at the forefront of this research, investigating enzymatic mechanisms for plant cell wall degradation and optimizing enzyme formulations for efficient extraction of pectin and other valuable compounds from citrus peels. These advancements result in improved product consistency, larger-scale production, and cost savings, making natural thickeners increasingly competitive with synthetic alternatives.

- Furthermore, advancements in material science and biotechnology are leading to the creation of new thickener types with specialized functionalities, such as shear thinning behavior, particle dispersion, viscosity modification, emulsion stabilization, suspension stability, and shelf life extension. These technological advancements underscore the dynamic nature of the market and its potential for continued growth.

What challenges does the Thickeners Industry face during its growth?

- The volatility in the pricing of raw materials utilized in the production of thickeners poses a significant challenge to the industry's growth trajectory.

- The market faces price challenges due to the volatile nature of raw materials used in their production. Raw materials, which include natural polymers, synthetic polymers, gums, and chemical compounds, are subject to price fluctuations caused by various factors such as supply-demand dynamics, geopolitical tensions, weather conditions, and currency fluctuations. For example, natural thickeners like xanthan gum and starch-based thickeners are derived from plants and are susceptible to price fluctuations due to factors like crop yields, weather conditions affecting harvests, and changes in agricultural practices. In addition, process optimization is crucial in the thickeners industry to mitigate these price fluctuations.

- Factors such as the flow behavior index, ionic strength effects, and temperature effects significantly impact viscosity control. Polymer thickening agents, such as cellulose derivatives and xanthan gum, play a vital role in maintaining the desired viscosity in various industries, including food and beverage, pharmaceuticals, and oil and gas. Understanding these factors and their impact on thickener production is essential for market participants to effectively manage their supply chains and maintain profitability.

Exclusive Customer Landscape

The thickeners market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the thickeners market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, thickeners market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Akzo Nobel NV - The company specializes in providing advanced thickeners, including Polibrid 705E, for the water-based paint and coatings industry. This thickener enhances product viscosity and texture, contributing significantly to the performance and quality of various coatings applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Akzo Nobel NV

- Altana AG

- Andritz AG

- Archer Daniels Midland Co.

- Arkema Group

- Ashland Inc.

- Axalta Coating Systems Ltd.

- BASF SE

- Berkshire Hathaway Inc.

- Clariant International Ltd.

- Dow Chemical Co.

- DuPont de Nemours Inc.

- Eastman Chemical Co.

- Henkel AG and Co. KGaA

- J M Huber Corp.

- Nouryon Chemicals Holding BV

- PPG Industries Inc.

- RAG Stiftung

- Standard Industries Inc.

- Sumitomo Chemical Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Thickeners Market

- In January 2024, DuPont Nutrition & Biosciences announced the launch of its new line of renewable thickeners, Danisco Danisco® PureSolve HM, in collaboration with Danisco A/S. This innovative product line offers improved texture and stability in various food and beverage applications, catering to the growing demand for clean-label and sustainable solutions (DuPont Press Release, 2024).

- In March 2024, Ashland Global Holdings Inc. And Ingredion Incorporated entered into a strategic partnership to expand their offerings in the market. The collaboration combines Ashland's specialty chemicals expertise with Ingredion's broad portfolio of plant-based texturizers, creating a comprehensive range of solutions for food, beverage, and industrial applications (Ashland Press Release, 2024).

- In May 2024, BASF SE completed the acquisition of Solvay's European dispersions business, including its thickeners division. This strategic move significantly expanded BASF's portfolio in the market, strengthening its position in the European market and providing access to Solvay's advanced technologies and customer base (BASF Press Release, 2024).

- In February 2025, the European Commission approved the use of microbial thickeners in food applications, marking a significant regulatory milestone for the market. This approval opens up new opportunities for manufacturers to develop and market innovative, sustainable, and cost-effective thickening solutions for the European food industry (European Commission Press Release, 2025).

Research Analyst Overview

- The market encompasses a range of polymer solutions, including colloidal suspensions and particle size distributions, that significantly influence the binder properties of various industries. Understanding thickener compatibility and chemical structure is crucial for optimizing pumping characteristics and ensuring regulatory compliance. Environmental impact and surface chemistry are increasingly important considerations, as are electrostatic interactions, hydrogen bonding, and rheology characterization. Application techniques, such as film formation and cost-effectiveness analysis, are essential for selecting the most appropriate thickener.

- Molecular weight distribution and hydrophobic interactions play a role in adhesive properties, while steric stabilization and safety data sheets are vital for ensuring safety and performance evaluation. Regulatory bodies continue to prioritize thickener selection based on interaction forces and flow rate optimization.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Thickeners Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

184 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.46% |

|

Market growth 2024-2028 |

USD 2.51 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.34 |

|

Key countries |

US, Malaysia, Indonesia, Germany, UK, South Korea, France, Canada, Brazil, Thailand, UAE, Mexico, China, Japan, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Thickeners Market Research and Growth Report?

- CAGR of the Thickeners industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the thickeners market growth of industry companies

We can help! Our analysts can customize this thickeners market research report to meet your requirements.

RIA -

RIA -