Transdermal Patches Market Size 2024-2028

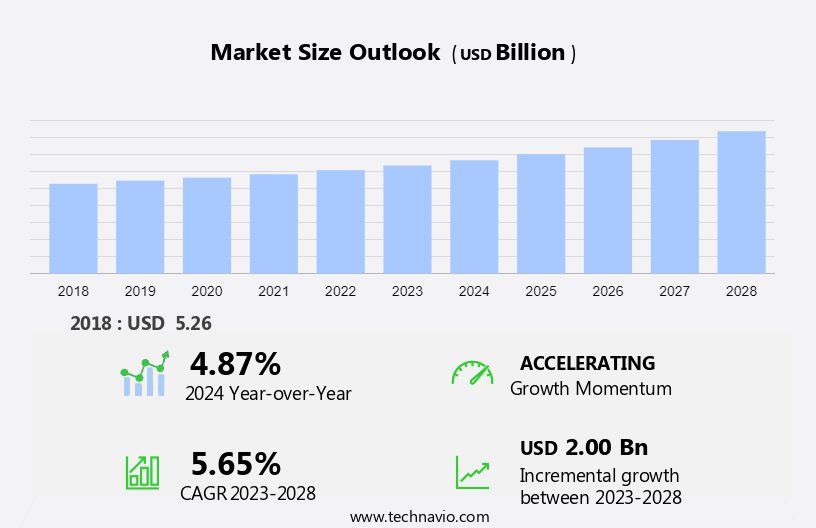

The transdermal patches market size is forecast to increase by USD 2.00 billion at a CAGR of 5.65% between 2023 and 2028. The market is experiencing significant growth due to the increasing demand for non-invasive drug delivery methods. This non-invasive approach offers several advantages, including improved patient compliance, consistent drug delivery, and reduced side effects. Another trend driving market growth is the development of microneedle patches, which enhance drug delivery efficiency by allowing drugs to penetrate deeper into the skin.

However, stringent regulatory approvals for transdermal drug delivery systems by government bodies pose a challenge to market growth. Regulatory agencies require extensive clinical trials and rigorous safety and efficacy testing, which can be time-consuming and costly. Despite these challenges, the market is expected to continue growing due to the numerous benefits offered by transdermal patches over traditional oral and injectable drug delivery methods.

Market Analysis

Transdermal patches are non-invasive medication delivery systems that provide controlled dosing and prolonged therapeutic effects for various chronic diseases and pain-related conditions. These patches work by delivering medication through the skin directly into the bloodstream, bypassing the digestive system. This method offers several advantages over traditional injections, including reduced healthcare facility costs, improved patient compliance, and fewer medication failures. Technological developments in transdermal patches have led to the creation of electronic and mechanical patches, which offer enhanced features such as real-time monitoring and programmable dosing. Analgesic patches are a common application of transdermal technology, providing effective pain management for conditions such as arthritis and diabetic neuropathy.

The elderly population, who often suffer from multiple chronic diseases, is a significant market for transdermal patches. Chronic diseases such as diabetes, hypertension, and pain-related conditions are major drivers for the growth of the market. The opioid epidemic has also fueled interest in non-invasive pain management methods, further boosting demand for transdermal patches. Adhesives and drug formulations are critical components of transdermal patches, and advancements in these areas are expected to drive innovation in the market. The market for transdermal patches is expected to grow significantly in the coming years, offering opportunities for manufacturers and investors in this space.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Pain management

- Central nervous system disorders

- Hormonal application

- Cardiovascular diseases

- Others

- End-user

- Homecare

- Hospitals and clinics

- Geography

- North America

- US

- Europe

- Germany

- UK

- Asia

- China

- Japan

- Rest of World (ROW)

- North America

By Application Insights

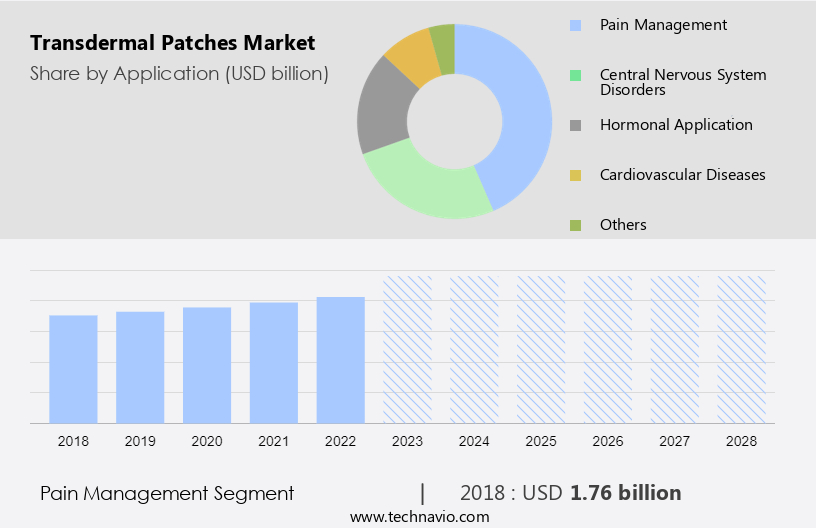

The pain management segment is estimated to witness significant growth during the forecast period. Transdermal patches represent a non-invasive, painless method for medication administration, particularly effective in managing chronic pain conditions. These patches, which deliver analgesic drugs through the skin and into the bloodstream, offer several advantages over traditional injections. Technological developments have led to advancements in adhesive performance, permeability, and skin barriers, ensuring effective drug delivery and minimizing skin irritation. The market for transdermal patches is experiencing growth due to the increasing prevalence of chronic illnesses, such as arthritis, neuropathic pain, and heart disease. Moreover, the opioid epidemic has fueled the demand for alternative, non-addictive pain management techniques. The multi-layer drug-in-adhesive segment is a significant contributor to the market, with various drugs, including opioids, NSAIDs, lidocaine, and antiretroviral drugs for HIV infection, being administered through this technology.

Further, the use of transdermal patches is not limited to pain management; they are also employed in contraceptive applications and for delivering medications to specific body areas, such as the abdomen, buttock, and upper torso, for individuals with a BMI of 30 kg/m2 or higher. The convenience and efficacy of transdermal patches make them an attractive alternative to oral-dosage forms, offering a more consistent dose of medicine and reducing healthcare facility costs.

Get a glance at the market share of various segments Request Free Sample

The Pain management segment accounted for USD 1.76 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

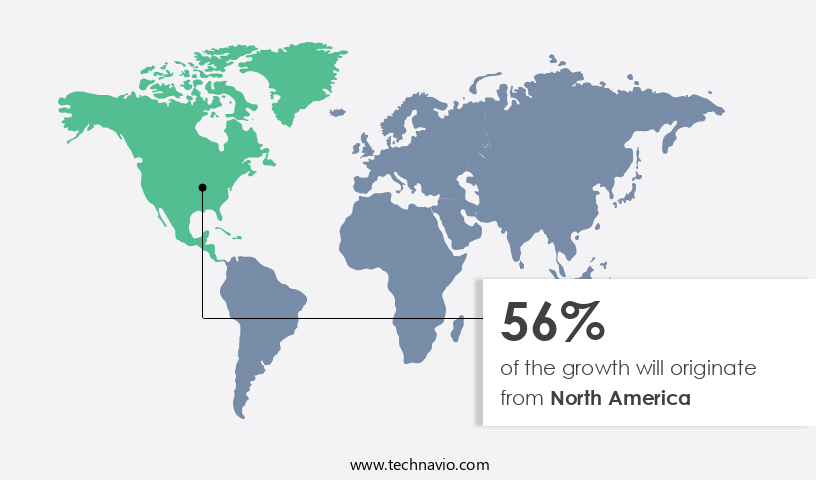

North America is estimated to contribute 56% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market is witnessing significant growth, particularly in the treatment of chronic diseases and conditions such as cancer, diabetes, hypertension, and pain-related conditions. North America is a leading region in this market, driven by the increasing prevalence of these conditions in the elderly population. Transdermal patches offer controlled dosing and prolonged therapeutic effects, making them an attractive delivery mechanism for various drug formulations. In North America, the US is the largest market contributor, with Canada and Mexico following suit. The demand for transdermal patches is increasing due to their convenience and effectiveness in managing chronic diseases. Nicotine transdermal patches are also gaining popularity in the region due to the growing number of smokers. Adhesive technology plays a crucial role in ensuring the effective and secure application of transdermal patches. Overall, the market is expected to expand steadily in the coming years, driven by the rising prevalence of chronic diseases and the need for alternative, effective, and convenient drug delivery mechanisms.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Growing demand for non-invasive drug delivery methods is the key driver of the market. The market is witnessing significant growth due to the increasing preference for non-invasive drug delivery methods, particularly in managing chronic illnesses. These patches offer a painless and convenient alternative to traditional injections and oral-dosage forms, making them an attractive option for patients and healthcare providers. Technological developments in transdermal patches have led to advancements in formulation issues, adhesive performance, and permeability, ensuring effective medication delivery through the skin and into the bloodstream. The opioid epidemic has further fueled the demand for non-addictive pain management techniques, making transdermal patches an essential tool in pain relief. However, challenges such as skin irritation and skin barriers remain, prompting drug delivery companies to innovate and develop multi-layer drug-in-adhesive segments to address these concerns.

Transdermal patches are being used to deliver various medications, including analgesics, antiretroviral drugs for HIV infection, and heart disease treatments. The market for these patches is expanding to cover various application sites, including the abdomen, buttock, and upper torso, and is expected to continue growing with technological advances in electronic and mechanical patches. The non-invasive and painless method of drug administration offered by transdermal patches is particularly appealing to individuals with a Body Mass Index (BMI) of 30 kg/m2 or higher, who may find it difficult to adhere to conventional medication regimens.

Market Trends

The development of microneedle patches for enhanced drug delivery efficiency is the upcoming trend in the market. Transdermal patches have emerged as a popular non-invasive method for medication delivery, particularly for managing chronic illnesses such as pain and hormonal imbalances. These patches, which adhere to the skin, deliver medication directly into the bloodstream, bypassing the digestive system and offering a painless, consistent dose. Technological developments in transdermal patch technology have led to the creation of advanced analgesic patches, which address formulation issues and improve adhesive performance, reducing skin irritation. Microneedle patches represent a significant trend in this market, with their ability to penetrate the skin's outer layer and create temporary micropores, enhancing drug delivery efficiency. This non-invasive method is especially beneficial for patients with conditions like HIV infection or heart disease, where traditional injections may not be an option due to healthcare facility costs or medication failure.

The multi-layer drug-in-adhesive segment of the market is expected to grow significantly due to its ability to deliver both small and large molecules, including antiretroviral drugs and vaccines, which may have limited permeability through the intact skin. The development of electronic and mechanical microneedle patches further expands the scope of transdermal therapy, offering potential solutions for various chronic conditions. However, challenges such as BMI limitations and application site selection remain, necessitating ongoing research and innovation in this field.

Market Challenge

Stringent regulatory approvals for transdermal drug delivery systems by government bodies is a key challenge affecting the market growth. Transdermal patches represent a non-invasive method for medication administration, particularly useful for managing chronic illnesses such as pain and hormonal imbalances. These patches, which deliver medication through the skin and into the bloodstream, offer several advantages over traditional injections, including painless application and elimination of healthcare facility costs. Analgesic patches, for instance, are widely used for pain management techniques, addressing formulation issues and skin irritation concerns associated with oral-dosage forms and opioid epidemic. Technological developments have significantly advanced transdermal patch technology, enabling the creation of multi-layer drug-in-adhesive segments, enhancing permeability and overcoming skin barriers. The market for these patches includes various applications, including heart disease, HIV infection, and contraception.

For instance, antiretroviral drugs for HIV infection are increasingly being delivered through transdermal patches to improve patient compliance and reduce the frequency of injections. Despite these benefits, the market faces regulatory challenges. Strict approval processes by government bodies, such as the FDA, necessitate rigorous testing, including biomechanical testing, animal testing, and clinical trials, to ensure safety and efficacy. This lengthy and costly process may delay market entry and limit the potential growth of transdermal patches, particularly for drug delivery companies seeking first-mover advantage. However, the advantages of non-invasive methods and the ongoing technological advances continue to drive the market forward.

These patches are applied to various body parts, including the abdomen, buttock, and upper torso, and are available in electronic, mechanical, and adhesive forms. The adhesive patch, in particular, has gained popularity due to its ease of use and effectiveness. Despite the challenges, the market is expected to grow, driven by the increasing prevalence of chronic illnesses and the need for painless, convenient medication administration methods. However, addressing issues related to adhesive performance, skin irritation, and drug delivery efficiency remains crucial for market expansion.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Boehringer Ingelheim International GmbH: The company offers transdermal patches through its Skinfusion transdermal delivery system such as Twirla AG200-15, AG200-ER (SmP), AG200-ER and AG890.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alvogen Iceland ehf

- Endo International Plc

- Hisamitsu Pharmaceutical Co. Inc.

- IontoPatch

- Johnson and Johnson Services Inc.

- Lead Chemical Co. Ltd.

- Luye Pharma Group Ltd.

- Medherant Ltd.

- Mundipharma International Ltd.

- Nitto Denko Corp.

- Novartis AG

- Purdue Pharma LP

- Sparsha Pharma International Pvt. Ltd.

- Teva Pharmaceutical Industries Ltd.

- Viatris Inc.

- AdhexPharma SAS

- Agile Therapeutics Inc.

- Bayer AG

- Evernow Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Transdermal patches are non-invasive medication delivery systems that provide an alternative to traditional injections for managing chronic illnesses. These patches work by delivering a consistent dose of medication through the skin and into the bloodstream. Analgesic patches are one of the most common types of transdermal patches, used for pain management. Technological developments in transdermal patch technology have led to advancements in drug delivery, adhesive performance, and permeability, making them a popular choice for patients. The opioid epidemic has led to a growing demand for non-addictive pain management techniques, further fueling the growth of the market. However, formulation issues, skin irritation, and skin barriers are some challenges facing the industry.

Drug delivery companies are investing in research and development to improve the efficacy and safety of transdermal patches. The multi-layer drug-in-adhesive segment is expected to dominate the market due to its ability to deliver multiple drugs simultaneously. Transdermal patches are used to administer various medications, including antiretroviral drugs for HIV infection, heart disease medications, and contraceptives. Transdermal patches can be applied to various body parts such as the abdomen, buttock, and upper torso. The non-invasive and painless method of medication administration is particularly beneficial for patients with a Body Mass Index (BMI) of 30 kg/m2 or higher, who may find it difficult to take oral-dosage forms. Technological advances in electronic and mechanical transdermal patches are also expected to drive market growth.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

159 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.65% |

|

Market growth 2024-2028 |

USD 2.00 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.87 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 56% |

|

Key countries |

US, Germany, UK, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Alvogen Iceland ehf, Boehringer Ingelheim International GmbH, Endo International Plc, Hisamitsu Pharmaceutical Co. Inc., IontoPatch, Johnson and Johnson Services Inc., Lead Chemical Co. Ltd., Luye Pharma Group Ltd., Medherant Ltd., Mundipharma International Ltd., Nitto Denko Corp., Novartis AG, Purdue Pharma LP, Sparsha Pharma International Pvt. Ltd., Teva Pharmaceutical Industries Ltd., Viatris Inc., AdhexPharma SAS, Agile Therapeutics Inc., Bayer AG, and Evernow Inc. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -