Transparent Barrier Packaging Film Market Size 2026-2030

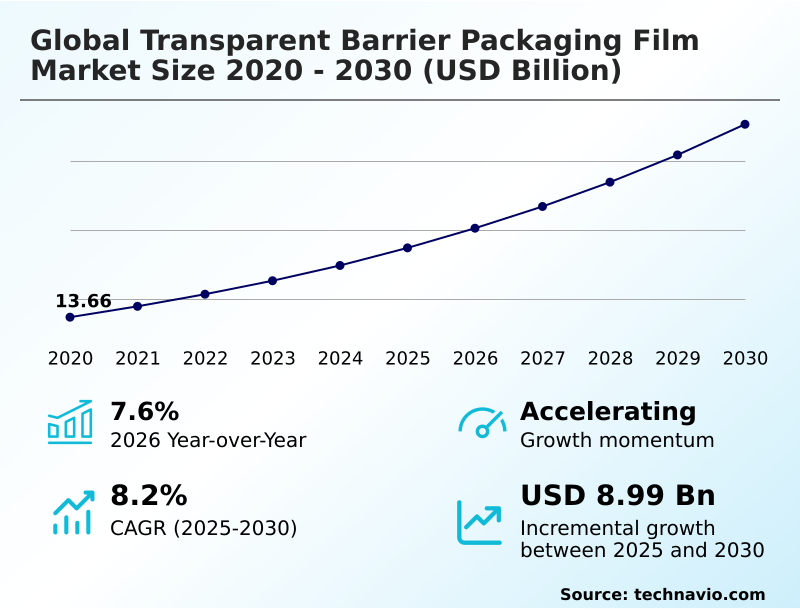

The transparent barrier packaging film market size is valued to increase by USD 8.99 billion, at a CAGR of 8.2% from 2025 to 2030. High demand for transparent barrier packaging film in food industry will drive the transparent barrier packaging film market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 40.9% growth during the forecast period.

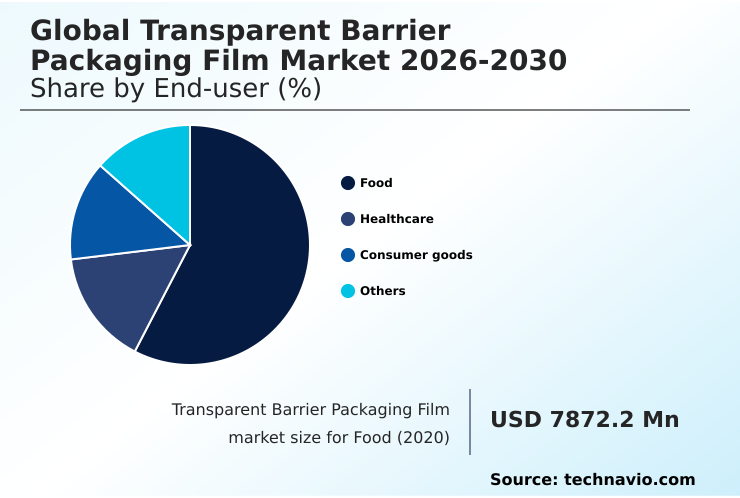

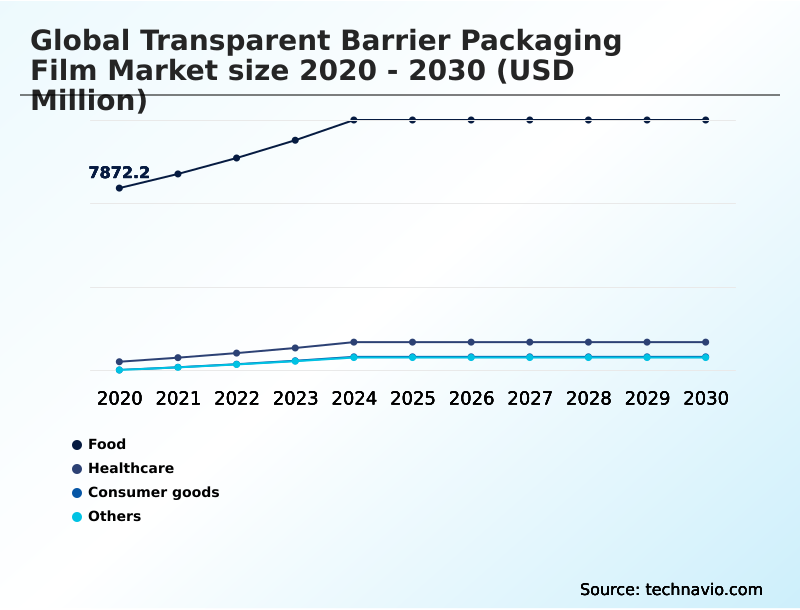

- By End-user - Food segment was valued at USD 10.13 billion in 2024

- By Material - Polyethylene segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 14.03 billion

- Market Future Opportunities: USD 8.99 billion

- CAGR from 2025 to 2030 : 8.2%

Market Summary

- The transparent barrier packaging film market is evolving amidst strong demand from the food, pharmaceutical, and consumer goods sectors, which require advanced materials to ensure product safety and extend shelf life. Key drivers include the need for packaging with a low oxygen transmission rate and excellent moisture vapor transmission rate to preserve freshness.

- A central business scenario involves supply chain optimization, where the adoption of lightweight, high-performance films reduces transportation costs and minimizes spoilage-related losses. However, the industry faces challenges from stringent food contact materials regulations and the high price volatility of raw materials like polymer resins.

- In response, a significant trend is the shift toward sustainable solutions, including bio-based polymer films and designs aligned with circular economy principles. Innovations in the co-extrusion process and the development of films with superior puncture resistance strength are enabling thinner, more durable packaging.

- This transition addresses both environmental mandates and consumer preferences for eco-friendly products without compromising the critical barrier properties necessary for product integrity.

What will be the Size of the Transparent Barrier Packaging Film Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Transparent Barrier Packaging Film Market Segmented?

The transparent barrier packaging film industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Food

- Healthcare

- Consumer goods

- Others

- Material

- Polyethylene

- Polypropylene

- Polyethylene terephthalate

- Ethylene vinyl alcohol

- Others

- Type

- Pouches

- Wraps and shrink films

- Flow wraps

- Lidding films

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By End-user Insights

The food segment is estimated to witness significant growth during the forecast period.

The food segment remains a principal consumer, driven by the demand for effective food preservation films.

Solutions leveraging modified atmosphere packaging and superior aroma barrier properties are critical for extending the usability of fresh produce packaging and complex ready-to-eat meal packaging.

Materials like ethylene vinyl alcohol copolymer, biaxially oriented polyethylene terephthalate, and biaxially oriented polypropylene are instrumental in achieving shelf-life extension technology goals.

As consumer habits evolve, the need for films with high puncture resistance strength and reliable heat sealable films for meat and poultry packaging and dairy product packaging is intensifying.

This segment's expansion is a major factor in market dynamics, contributing over 40% of the industry's incremental growth, particularly in developing economies.

The Food segment was valued at USD 10.13 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 40.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Transparent Barrier Packaging Film Market Demand is Rising in APAC Get Free Sample

The geographic landscape is led by APAC, which accounts for 40.88% of the market's growth opportunities, driven by rapid urbanization and expanding manufacturing capabilities in countries like China and India.

North America follows, representing 25.54% of the opportunity, with a mature market focused on high-performance applications and sustainability. In Europe, stringent regulations are accelerating the adoption of high-barrier mono-material solutions and bio-based polymer films.

The use of polyvinylidene chloride coating is declining due to environmental concerns, creating opportunities for alternatives. Innovations in the chemical recycling process and smart packaging integration with digital watermarking for sorting are prominent.

Across regions, demand for aseptic packaging material and films from polylactic acid films is growing, especially for cosmetic product protection and aseptic liquid packaging, reflecting a global trend toward sustainable and functional packaging.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the transition to sustainable packaging requires a deep understanding of material performance and regulatory compliance. A key consideration is the impact of EVOH concentration on recyclability, which directly influences the viability of circular economy models for flexible packaging.

- For brand owners, selecting the right high barrier films for fresh produce shelf-life is critical for packaging solutions to reduce food waste. This involves evaluating options from transparent barrier films vs metallized films, each offering different benefits.

- The goal is to achieve downgauging films without losing barrier properties, a technical challenge that advancements in silicon oxide coated films are helping to solve. In the food sector, the focus is on recyclable mono-material for snack food packaging and developing retortable pouches for long shelf-life foods.

- For meat and cheese, oxygen barrier films are essential, often used with lidding films for modified atmosphere packaging. Improving shelf life with EVOH barrier films is a proven strategy. For other sectors, effective pharmaceutical packaging with high moisture barrier and transparent packaging for premium cosmetic products are top priorities.

- As companies transition to recyclable high-barrier materials, they must also ensure compliance with food contact material regulations and manage post-consumer recycled content in food packaging. The use of PCR content integration in non-food packaging and finding cost-effective barrier films for consumer goods are also key parts of this strategic shift.

- This holistic approach ensures barrier film solutions for e-commerce shipping are both effective and sustainable.

What are the key market drivers leading to the rise in the adoption of Transparent Barrier Packaging Film Industry?

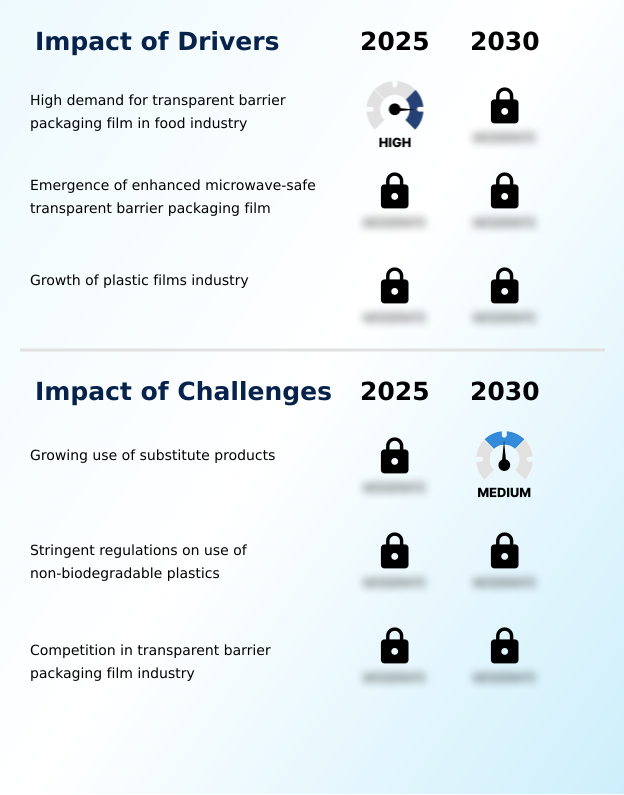

- High demand for transparent barrier packaging film from the food industry is a key driver propelling market growth.

- The market's expansion is fueled by the increasing demand for convenience and product protection across multiple sectors.

- The development of microwaveable food packaging, which can reduce consumer preparation time by over 60%, relies on advanced flexible packaging laminates and cold seal adhesives. Innovations like anti-fog additives and UV protection films enhance product visibility and integrity.

- The co-extrusion process and plasma enhanced chemical vapor deposition techniques are enabling lightweighting packaging design, reducing material usage by up to 25% without compromising barrier performance.

- Furthermore, the growth of e-commerce necessitates tamper-evident packaging features and child-resistant packaging solutions for safety. This drive for functional, user-friendly formats, including single-serve portion packs, supports the broader adoption of advanced films offering superior shelf-life extension technology.

What are the market trends shaping the Transparent Barrier Packaging Film Industry?

- A significant market trend is the rising demand for high-performance specialty barrier films, driven by the need for advanced packaging solutions offering superior protective properties.

- A dominant trend is the industry's pivot toward sustainable barrier solutions, driven by stringent regulations and consumer demand. The implementation of the extended producer responsibility scheme is compelling manufacturers to design for circular economy principles, significantly boosting demand for materials with high mechanical recycling compatibility.

- Innovations in advanced recycling are now enabling the recovery of over 90% of polymers from post-consumer recycled content, making it a viable feedstock for pharmaceutical grade films. Furthermore, the development of bio-based materials is advancing, with compostable packaging films and those using biodegradable polymer technology achieving barrier performance within 15% of their traditional counterparts.

- This transition is crucial for supply chain waste reduction and improving the overall product-to-package ratio optimization through sustainable material sourcing and compliance with food contact materials regulation.

What challenges does the Transparent Barrier Packaging Film Industry face during its growth?

- The growing adoption of alternative materials and substitute products presents a key challenge to the industry's growth.

- The market confronts notable challenges, including intense competition from substitute materials and price volatility. Non-transparent options like aluminum foil, which boast recycling rates exceeding 70% in some regions, present a significant challenge to plastic-based recyclable flexible packaging.

- Moreover, fluctuations in polymer resin prices can impact manufacturer profit margins by over 10% in a single quarter, complicating cost structures for products like retortable pouch technology and lidding film applications. The push for downgauging film thickness to create more sustainable mono-material pouch construction faces technical hurdles in maintaining a low moisture vapor transmission rate and adequate puncture resistance.

- The industry must also contend with the perception of fiber-based barrier packaging as a more eco-friendly alternative, affecting demand for films used in vacuum skin packaging and medical device sterile packaging.

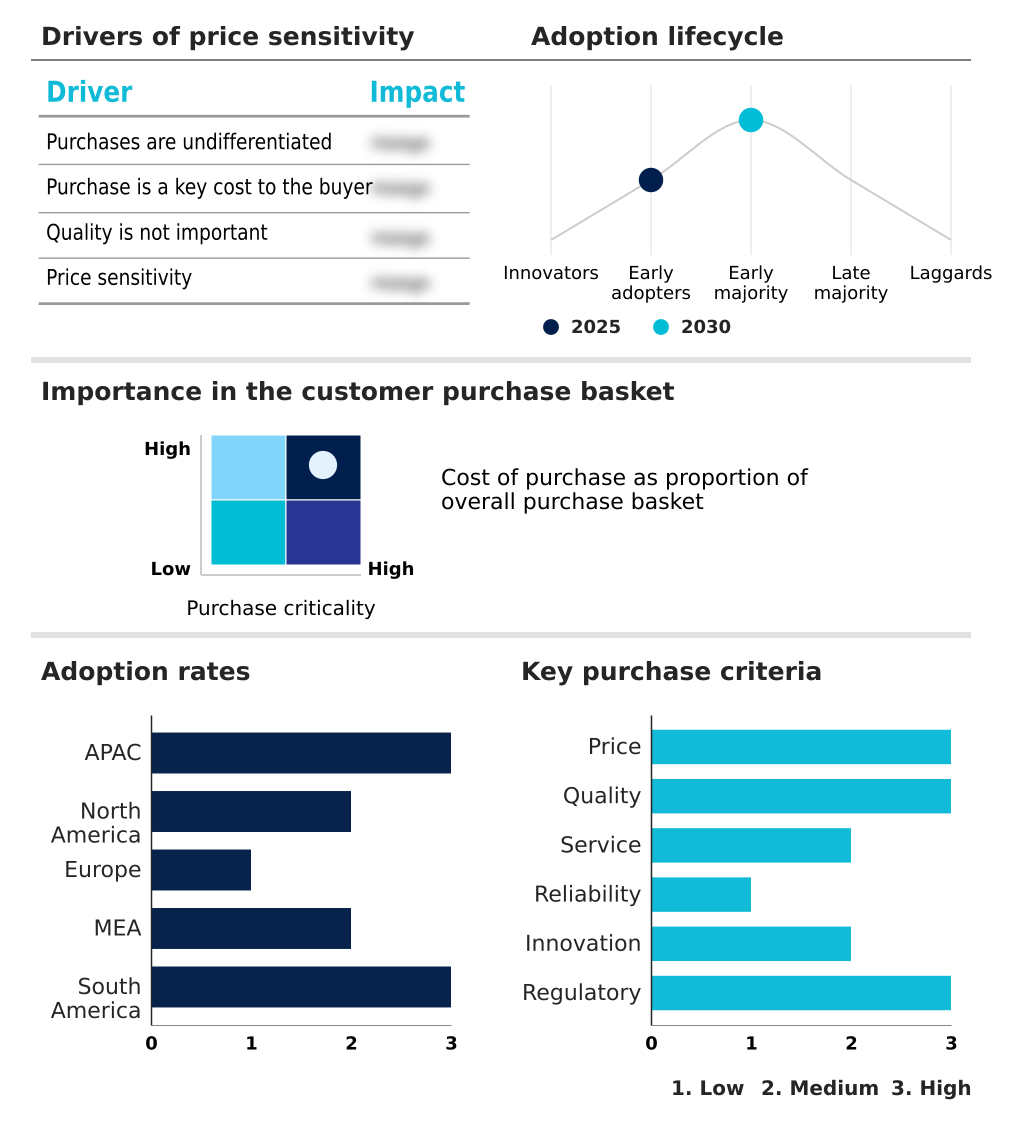

Exclusive Technavio Analysis on Customer Landscape

The transparent barrier packaging film market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the transparent barrier packaging film market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Transparent Barrier Packaging Film Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, transparent barrier packaging film market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - Analysis indicates a focus on metal-free laminates, delivering high-barrier protection and enhanced recyclability for product integrity and sustainability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Amcor Plc

- CCL Industries Inc.

- Celplast Metallized Products

- Cosmo Films Ltd.

- DUO PLAST AG

- DuPont de Nemours Inc.

- Glenroy Inc.

- Huhtamaki Oyj

- KP Holding GmbH and Co. KG

- Mitsubishi Chemical Grp.

- Mondi Plc

- Sealed Air Corp.

- Sonoco Products Co.

- Sumilon Polyester Ltd.

- Taghleef Industries SpA

- Toppan Inc.

- UFlex Ltd.

- Winpak Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Transparent barrier packaging film market

- In May 2025, Mitsubishi Chemical Group received recognition from the Association of Plastic Recyclers for its SoarnoL EVOH resins, confirming their compatibility with polyethylene film recycling streams when used at specified concentrations.

- In April 2025, Amcor is expected to finalize its acquisition of Berry Global, a strategic move anticipated to fortify its leadership in high-barrier lidding films and accelerate innovation in sustainable packaging solutions.

- In February 2025, TIPA launched an advanced home-compostable metallized high-barrier film, providing a sustainable packaging alternative for products like snack foods that traditionally rely on hard-to-recycle flexible packaging.

- In October 2024, Indorama Ventures, in partnership with other firms, announced the upcoming commercial launch of the world's first bio-polyethylene terephthalate bottle produced from post-consumer feedstock, specifically used cooking oil.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Transparent Barrier Packaging Film Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 316 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.2% |

| Market growth 2026-2030 | USD 8986.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.6% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is defined by a continuous push for material innovation to meet dual demands for performance and sustainability. Core technologies such as ethylene vinyl alcohol copolymer, biaxially oriented polyethylene terephthalate, and biaxially oriented polypropylene remain foundational, but the focus is shifting. Developments in coatings, including silicon oxide coating, aluminum oxide coating, and polyvinylidene chloride coating, are enhancing barrier properties.

- Processes like the co-extrusion process and plasma enhanced chemical vapor deposition are enabling thinner, more complex flexible packaging laminates. A key boardroom consideration is aligning product strategy with evolving regulations like the extended producer responsibility scheme and mandates requiring 30% post-consumer recycled content. This directly impacts material choices, favoring high-barrier mono-material designs with mechanical recycling compatibility.

- Applications such as lidding film application, retortable pouch technology, and vacuum skin packaging are being re-engineered based on circular economy principles. The objective is to maintain critical performance metrics like a low oxygen transmission rate and moisture vapor transmission rate while satisfying new sustainability benchmarks set by food contact materials regulation and other governing bodies.

What are the Key Data Covered in this Transparent Barrier Packaging Film Market Research and Growth Report?

-

What is the expected growth of the Transparent Barrier Packaging Film Market between 2026 and 2030?

-

USD 8.99 billion, at a CAGR of 8.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Food, Healthcare, Consumer goods, and Others), Material (Polyethylene, Polypropylene, Polyethylene terephthalate, Ethylene vinyl alcohol, and Others), Type (Pouches, Wraps and shrink films, Flow wraps, and Lidding films) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

High demand for transparent barrier packaging film in food industry, Growing use of substitute products

-

-

Who are the major players in the Transparent Barrier Packaging Film Market?

-

3M Co., Amcor Plc, CCL Industries Inc., Celplast Metallized Products, Cosmo Films Ltd., DUO PLAST AG, DuPont de Nemours Inc., Glenroy Inc., Huhtamaki Oyj, KP Holding GmbH and Co. KG, Mitsubishi Chemical Grp., Mondi Plc, Sealed Air Corp., Sonoco Products Co., Sumilon Polyester Ltd., Taghleef Industries SpA, Toppan Inc., UFlex Ltd. and Winpak Ltd.

-

Market Research Insights

- The market's momentum is increasingly shaped by sustainable material sourcing and the push for recyclable flexible packaging. Regulatory shifts, such as mandates requiring over 30% recycled content in some jurisdictions, are fundamentally altering procurement strategies. In response, innovations in smart packaging integration, including digital watermarking for sorting, are improving recycling efficiency by over 40% in pilot programs.

- There is also a strong focus on lightweighting packaging design and tamper-evident packaging features to meet the demands of e-commerce protective packaging. These dynamics create a landscape where product-to-package ratio optimization is not just a cost-saving measure but a strategic necessity for compliance and brand positioning.

We can help! Our analysts can customize this transparent barrier packaging film market research report to meet your requirements.

RIA -

RIA -