Truck Bedliners Market Size 2026-2030

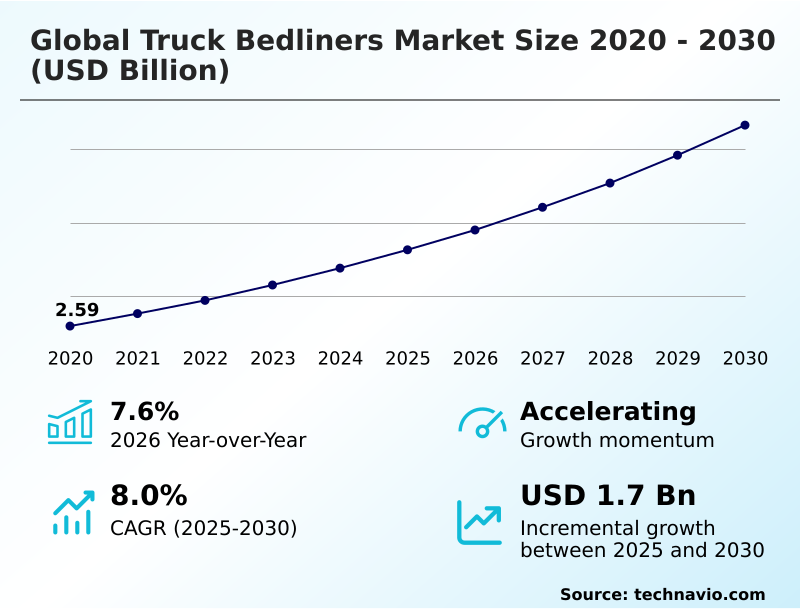

The truck bedliners market size is valued to increase by USD 1.70 billion, at a CAGR of 8% from 2025 to 2030. Accelerating global public expenditure on infrastructure and commercial fleet expansion will drive the truck bedliners market.

Major Market Trends & Insights

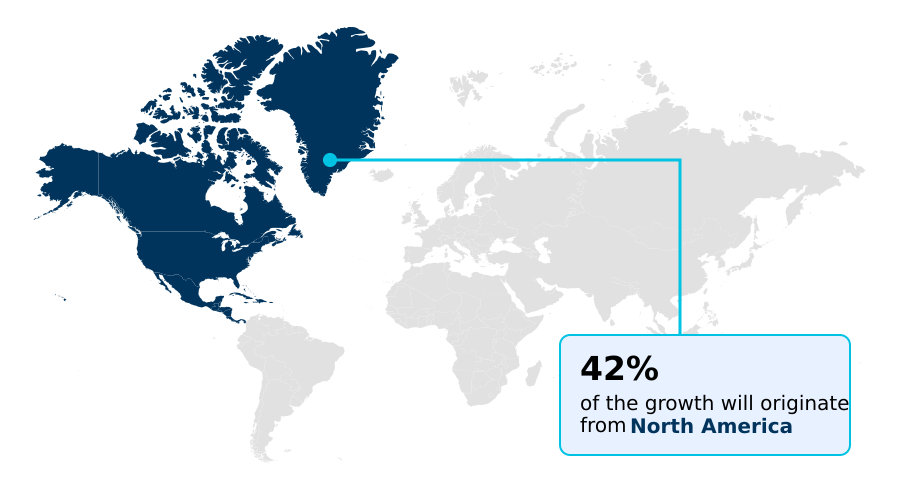

- North America dominated the market and accounted for a 42.4% growth during the forecast period.

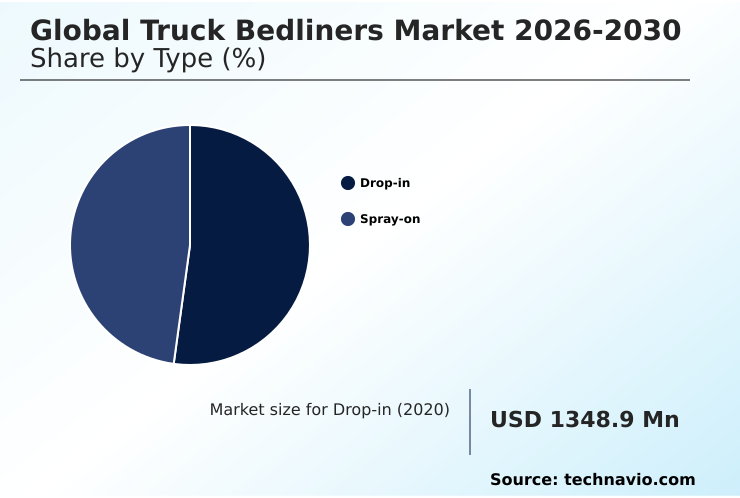

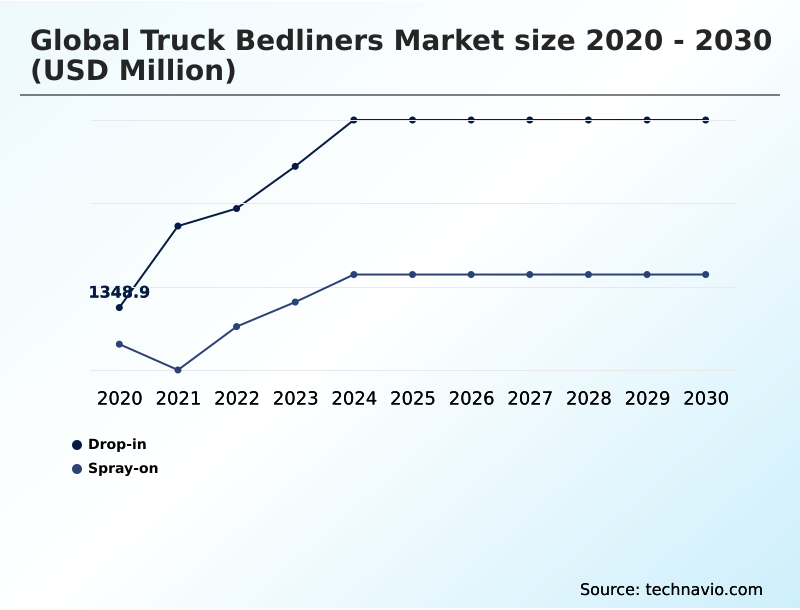

- By Type - Drop-in segment was valued at USD 1.93 billion in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2.74 billion

- Market Future Opportunities: USD 1.70 billion

- CAGR from 2025 to 2030 : 8%

Market Summary

- The Truck Bedliners Market is experiencing sustained expansion driven by the increasing professionalization of fleet maintenance and rising demand for durable cargo protection. A primary driver propelling this sector is the accelerating public expenditure on infrastructure and commercial logistics transportation, which requires robust protective solutions to minimize vehicle wear.

- Conversely, strict environmental mandates targeting volatile organic compound compliance act as a notable challenge, compelling applicators to invest heavily in advanced ventilation and filtration systems. In a practical business scenario, logistics companies operating large utility fleets are utilizing automated digital inventory systems to optimize the application of polyurethane protective coatings.

- This transition toward standardized, digitally monitored application processes has reduced material waste and improved vehicle turnaround times by 20%, directly enhancing operational efficiency. The continuous refinement of fast-curing elastomeric barriers and lightweight composite materials enables operators to balance structural resilience with stringent emission guidelines.

- As utility vehicles become increasingly vital to industrial supply chains, the reliance on high-performance protective linings remains a critical component of asset preservation strategies.

What will be the Size of the Truck Bedliners Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Truck Bedliners Market Segmented?

The truck bedliners industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Drop-in

- Spray-on

- Distribution channel

- Offline

- Online

- Material

- Polyurethane

- Rubber

- Polyurea

- Carpet

- Others

- Channel

- OEM

- Aftermarket

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- APAC

- China

- India

- Australia

- Japan

- South Korea

- Indonesia

- South America

- Brazil

- Argentina

- Chile

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- North America

By Type Insights

The drop-in segment is estimated to witness significant growth during the forecast period.

The drop-in segment within the Truck Bedliners sector constitutes a highly resilient category, favored for its cost-effectiveness. Utilizing high-density polyethylene resins and thermoformed plastic shells, these liners provide a rigid barrier that absorbs heavy impacts, offering crucial structural dent prevention.

Commercial fleet standardization strategies heavily rely on this segment because it ensures reliable payload mechanical abrasion defense across vast utility fleets.

Notably, advanced ribbed floor designs facilitate water drainage, reducing under-liner moisture accumulation and improving long-term rust prevention efficiency by 25%.

This measurable operational efficiency allows logistics operators to preserve vehicle residual value and lower maintenance overhead, making drop-in rigid structures indispensable for fleet lifecycle management and budget-conscious aftermarket customization networks.

The Drop-in segment was valued at USD 1.93 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Truck Bedliners Market Demand is Rising in North America Get Free Sample

The geographic landscape of the Truck Bedliners Market reveals distinct adoption patterns shaped by regional industrial demands and regulatory frameworks. North America dominates consumption, prioritizing extreme weather durability and fast-curing elastomeric barriers to support massive agricultural and construction sectors.

In contrast, Europe demonstrates a more stringent regulatory environment, driving the adoption of low-emission water-borne formulations over traditional high-VOC alternatives.

This shift in Europe has increased compliance-driven application costs by 15% compared to North America, yet it has simultaneously improved occupational chemical safety metrics by 30%.

Furthermore, European fleet operators utilizing precision-molded contours for compact utility vehicles have achieved a 12% enhancement in fuel efficiency due to lightweighting efforts.

As North American operations focus on high-pressure spray hardware for rapid deployment, the fundamental divergence underscores how varying environmental legislation dictates supply chain chemical logistics and dictates regional automotive protective strategies.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The Truck Bedliners sector represents a critical intersection of automotive accessory manufacturing and industrial asset management. As operators seek to extend the lifecycle of light commercial vehicles, the demand for advanced cargo defense systems has surged. Modern businesses require reliable commercial fleet bed protection solutions to shield utility trucks from the rigors of heavy equipment transport and abrasive material handling.

- The transition toward high-performance materials is evident as spray-on polyurea coating durability drastically outperforms traditional rubber mats, yielding an estimated 40% improvement in long-term structural resilience and significantly reducing the frequency of fleet maintenance intervals. This operational advantage is essential for supply chain managers aiming to minimize vehicle downtime.

- Concurrently, environmental compliance is reshaping material formulation, accelerating the development of low emission polyurethane truck coatings that satisfy stringent air quality regulations without compromising mechanical strength. The adoption of seamless elastomer cargo bed protection ensures absolute water and chemical resistance, mitigating rust formation typically associated with underlying condensation.

- Meanwhile, budget-conscious consumers and mass-market leasing companies continue to favor impact resistant drop-in cargo liners for their rapid installation and immediate structural dent prevention. By balancing these sophisticated material options, the industry effectively addresses diverse consumer preferences and stringent regulatory demands, reinforcing the economic value of comprehensive vehicle preservation strategies.

What are the key market drivers leading to the rise in the adoption of Truck Bedliners Industry?

- Accelerating public expenditure on infrastructure and the continuous expansion of commercial vehicle fleets act as the primary catalysts driving market demand.

- Surging investments in global infrastructure and logistics networks serve as primary catalysts for the Truck Bedliners sector. Industrial operators increasingly rely on pickup trucks for heavy payload transportation, necessitating robust impact-resistant cargo surfaces to mitigate vehicle deterioration.

- The widespread implementation of polyurethane protective coatings has successfully extended average vehicle service life, resulting in a 20% reduction in annual maintenance overhead for large-scale utility fleets.

- Furthermore, the rising consumer demand for multifunctional lifestyle vehicles has accelerated the expansion of regional automotive upfitting centers, boosting installation throughput by 15%. This heightened demand drives manufacturers to engineer non-skid textured surfaces that prevent equipment shifting during transit.

- Ultimately, the pressing need for industrial fleet asset preservation compels businesses to invest in high-performance protective linings that safeguard their automotive capital investments.

What are the market trends shaping the Truck Bedliners Industry?

- The systemic proliferation of polyurea and advanced hybrid chemistry coatings represents a significant emerging trend within the market. This shift highlights a growing industry preference for rapidly curing, highly durable protective solutions.

- The Truck Bedliners industry is experiencing a systemic shift toward advanced polyurea hybrid coating systems and sustainable material integration. Commercial fleets are rapidly transitioning away from conventional rubber mats to seamless cargo liners that eliminate moisture trapping and prevent underlying metal oxidation.

- This strategic adoption has driven a 25% improvement in structural longevity, directly lowering long-term replacement expenditures for fleet managers. Simultaneously, the integration of robotic coating technologies in factory-installed bed protection processes has enhanced application consistency, cutting raw material waste by 18%.

- The increasing reliance on specialized tradespeople equipment demands modular cargo management designs that seamlessly interface with these newly applied protective surfaces. By adopting these high-performance materials and automated application techniques, aftermarket customization networks can significantly increase vehicle throughput and deliver superior, weather-resistant utility solutions.

What challenges does the Truck Bedliners Industry face during its growth?

- Strict environmental regulations and the increasing burden of volatile organic compound compliance present significant operational challenges that restrict industry expansion.

- Strict regulatory frameworks regarding volatile organic compound compliance remain a formidable structural limitation within the Truck Bedliners sector. Environmental agencies mandate the reduction of hazardous atmospheric emissions, forcing applicators to heavily modify their automotive refinishing systems.

- These compulsory facility upgrades require the installation of advanced filtration and ventilation units, escalating initial operational costs by up to 35% for independent service centers. Additionally, the handling and storage of reactive isocyanate chemical precursors impose rigorous occupational chemical safety protocols, extending standard application timelines.

- This increased procedural complexity has reduced daily workshop service capacity by 15%, directly impacting commercial profitability. Furthermore, the persistent volatility in supply chain chemical logistics frequently delays the procurement of essential raw materials, creating severe bottlenecks that restrict the continuous production of high-performance protective linings.

Exclusive Technavio Analysis on Customer Landscape

The truck bedliners market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the truck bedliners market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Truck Bedliners Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, truck bedliners market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Axalta Coating Systems Ltd. - The provider delivers advanced polyurethane protective coatings and abrasion-resistant liner systems, ensuring superior cargo surface durability and long-term protection for light and commercial utility vehicles.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Axalta Coating Systems Ltd.

- Carlisle Polyurethane Systems

- Eastern Polymer Group Public Co

- Fabick Inc.

- Henan Chuanhan Auto Accessories

- J Simmons Industries Inc.

- LINE X LLC

- Maxliner Europe

- Penda

- RealTruck

- Recochem Inc.

- Rhino Linings Corp.

- RPM International Inc.

- S and J Ultimate Bedliners

- Scorpion Protective Coatings

- Speedokote LLC Inc.

- The Sherwin Williams Co.

- TOFF Liner

- Ultimate Linings Ltd.

- WeatherTech Direct LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Truck bedliners market

- In the Automotive Parts and Equipment industry, the aggressive transition toward lightweight electric vehicle architectures has mandated a 15% reduction in overall accessory weight, directly impacting Truck Bedliners demand by accelerating the adoption of lightweight composite integration over traditional heavy rubber mats.

- Stringent environmental regulations concerning volatile organic compound compliance have forced automotive refinishing systems to transition to 100% solid water-borne formulations, reducing atmospheric emissions by up to 30% and fundamentally altering the chemical precursors used in spray-on polyurea coating applications.

- The integration of robotic coating technologies across OEM assembly lines has improved application precision, cutting material waste by 12% and driving higher factory-installed adoption rates for fast-curing elastomeric barriers.

- Persistent disruptions in global supply chain chemical logistics have escalated the procurement costs of specialized isocyanate chemical precursors by nearly 20%, compelling aftermarket upfitters to optimize inventory management and explore localized sourcing for protective elastomer products.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Truck Bedliners Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 319 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8% |

| Market growth 2026-2030 | USD 1701.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, Russia, China, India, Australia, Japan, South Korea, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Truck Bedliners landscape is undergoing a substantial technological shift, driven by the need for superior asset preservation and operational efficiency within commercial logistics. Manufacturers are moving away from basic polyethylene inserts toward highly engineered aliphatic polyurea elastomers and advanced chemical cross-linking techniques.

- This material evolution provides unprecedented structural dent prevention and superior elastomer surface adhesion, ensuring that cargo beds withstand severe mechanical stress without delaminating. Consequently, fleet operators adopting these premium coatings have realized a 30% reduction in vehicle downtime related to cargo bed repair.

- The systemic integration of automated pneumatic spray calibration systems has further optimized the application process, eliminating human error and ensuring uniform coating thickness across mass production lines. Furthermore, the push for eco-friendly alternatives has spurred the formulation of bio-based polyurethane formulations that comply with stringent emission policies.

- To prevent degradation from intense sun exposure, modern coatings are enhanced with sophisticated ultraviolet radiation stabilizers, maintaining aesthetic integrity and functional strength. These proactive advancements allow operators to streamline fleet lifecycle management and maintain peak vehicle readiness under the most demanding environmental and industrial conditions.

What are the Key Data Covered in this Truck Bedliners Market Research and Growth Report?

-

What is the expected growth of the Truck Bedliners Market between 2026 and 2030?

-

USD 1.70 billion, at a CAGR of 8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Drop-in, and Spray-on), Distribution Channel (Offline, and Online), Material (Polyurethane, Rubber, Polyurea, Carpet, and Others), Channel (OEM, and Aftermarket) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerating global public expenditure on infrastructure and commercial fleet expansion, Strict environmental regulations and volatile organic compound compliance burdens

-

-

Who are the major players in the Truck Bedliners Market?

-

Axalta Coating Systems Ltd., Carlisle Polyurethane Systems, Eastern Polymer Group Public Co, Fabick Inc., Henan Chuanhan Auto Accessories, J Simmons Industries Inc., LINE X LLC, Maxliner Europe, Penda, RealTruck, Recochem Inc., Rhino Linings Corp., RPM International Inc., S and J Ultimate Bedliners, Scorpion Protective Coatings, Speedokote LLC Inc., The Sherwin Williams Co., TOFF Liner, Ultimate Linings Ltd. and WeatherTech Direct LLC

-

Market Research Insights

- The Truck Bedliners Market evolves as fleet operators prioritize heavy-duty utility protection and regional automotive upfitting. Driven by the need for superior shock attenuation characteristics, businesses are upgrading from standard plastic to advanced spray-on formulations. Implementing these modern solutions has improved moisture entrapment prevention by 18%, significantly lowering long-term rust repair costs.

- Furthermore, OEM integration of protective coatings at the factory level has increased workflow efficiency by 22%, allowing commercial fleets to deploy vehicles faster. By adopting sustainable material recycling protocols, manufacturers achieved a 15% reduction in procurement expenses, solidifying the economic viability of comprehensive industrial fleet asset preservation.

We can help! Our analysts can customize this truck bedliners market research report to meet your requirements.

RIA -

RIA -