US Data Center Construction Market Size 2025-2029

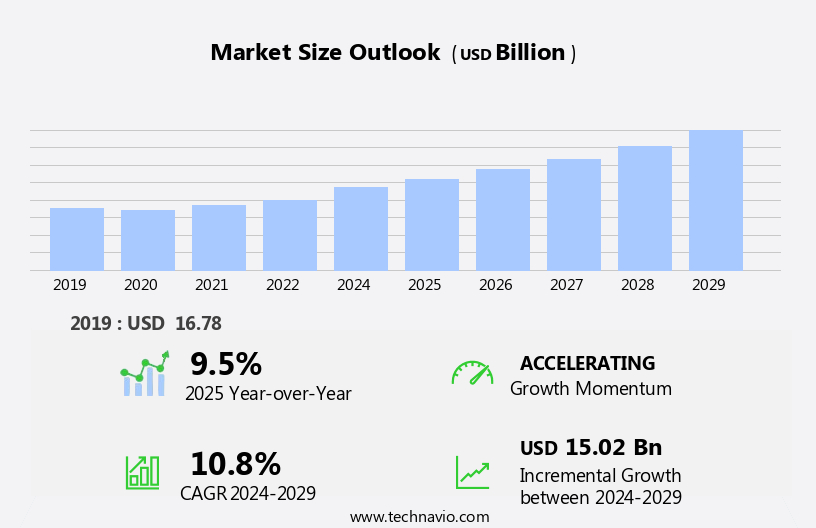

The US data center construction market size is forecast to increase by USD 15.02 billion at a CAGR of 10.8% between 2024 and 2029.

- US Data Center Construction Market is experiencing significant growth due to the increasing number of data centers being constructed to meet the surging demand for digital services and cloud computing. This trend is driven by the shift towards remote work and learning, as well as the increasing adoption of Internet of Things (IoT) devices and advanced technologies such as artificial intelligence and machine learning. Another key trend in the market is the focus on constructing eco-friendly data centers. With growing concerns over energy consumption and carbon footprint, data center operators are investing in renewable energy sources and energy-efficient designs to reduce their environmental impact.

- However, the market is not without challenges. Cybersecurity issues remain a major concern, with data centers being prime targets for cyber attacks due to the sensitive information they house. As such, data center operators must invest in robust security systems and implement strict access controls to mitigate these risks. However, cybersecurity challenges must be addressed to ensure the secure operation of these facilities. Companies seeking to capitalize on market opportunities should focus on energy efficiency, cybersecurity, and sustainability to stay competitive.

What will be the size of the US Data Center Construction Market during the forecast period?

- US data center construction market is experiencing robust growth, driven by the increasing demand for advanced telecommunications infrastructure to support IT and telecommunications industries, government and defense sectors, 5G networks, cloud-based services, and edge data centers. This growth is reflected in the significant expansion of data center capacity, with a focus on electrical infrastructure, including UPS systems, and mechanical infrastructure, such as cooling systems. Edge data centers and edge computing are also gaining traction due to the need for real-time data processing and data-driven decision-making.

- The market's size is substantial, with billions of dollars being invested annually. Physical damage from natural disasters and the increasing importance of advanced technology solutions are additional factors contributing to the market's momentum. Overall, the data center construction market is a dynamic and evolving sector, underpinned by the ongoing digital transformation and the growing importance of technology in various industries.

How is this market segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Enterprise

- Cloud

- Colocation

- Hyperscale

- End-user

- IT and telecom

- BFSI

- Government and defense

- Others

- Infrastructure

- Electrical Infrastructure

- Mechanical Infrastructure

- Networking Infrastructure

- Power Distribution & Cooling Infrastructure

- Geography

- US

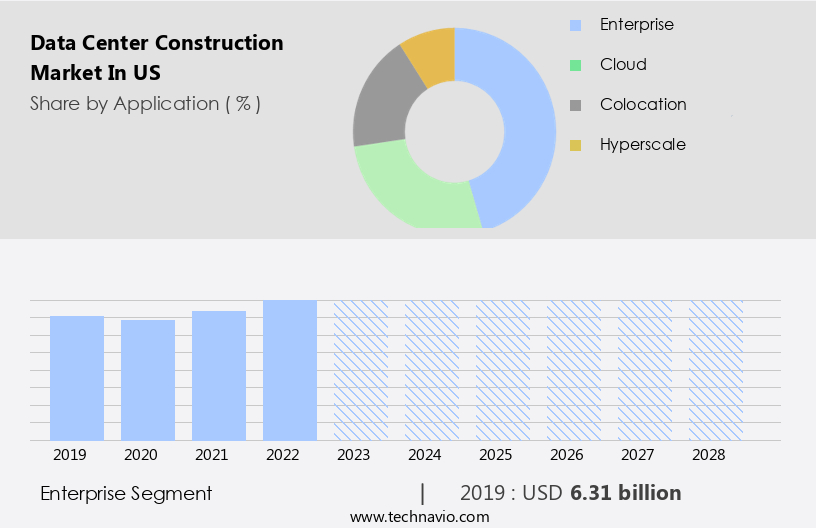

By Application Insights

The enterprise segment is estimated to witness significant growth during the forecast period.

In today's digital economy, businesses across sectors including healthcare, finance, and IT are undergoing transformation through the adoption of cloud computing, big data analytics, IoT devices, and artificial intelligence (AI). The resulting surge in digital data from various sources necessitates the need for advanced data center infrastructure. Enterprise data centers must provide high-capacity storage and processing capabilities to manage and analyze vast volumes of data efficiently. This data is generated from sources such as social media, mobile devices, IoT sensors, and business applications. By deriving actionable insights from this data, businesses can support decision-making processes and optimize operations.

The electrical infrastructure of data centers includes UPS systems and other electrical infrastructure, while mechanical infrastructure comprises cooling systems. IT and telecommunications sectors are significant consumers of data center services, including cloud-based data storage, cloud applications, and AI algorithms. Government and defense sectors also utilize data centers for cloud-based healthcare solutions, smart devices, and disaster recovery protocols. The adoption of cloud computing and edge computing, 5G networks, and telecommunication providers' cloud-based services is driving the demand for data centers. However, data security and cyber threats, including data breaches, remain critical concerns. Innovative designs, modular power infrastructure, and OPEX savings through real-time monitoring software and free cooling techniques are essential considerations for data center construction. Macroeconomic factors such as inflation rates, a strong economy, and a stable political environment influence domestic and international investments in data centers. Technological innovation, including district heating and innovative designs, is also shaping the data center landscape.

Get a glance at the market share of various segments Request Free Sample

The Enterprise segment was valued at USD 6.31 billion in 2019 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of US Data Center Construction Market?

- Increasing number of data centers is the key driver of the market. The digital transformation driving businesses and consumers towards cloud computing, streaming media, e-commerce, and IoT devices has resulted in an increased demand for data centers to support the underlying infrastructure. Edge computing, which processes data closer to the source or end-users, necessitates the deployment of smaller data centers or micro data centers at the network's edge, leading to a construction boom in various locations.

- Some notable upcoming data center projects include Microsoft's plans for new data centers, underlining the market's dynamic growth. As digital services continue to expand, the demand for data centers will persistently increase, making this an opportune time for businesses to invest in this sector.

What are the market trends shaping the US Data Center Construction Market?

- Increased focus on constructing eco-friendly data centers in US is the upcoming trend in the market. Data centers have emerged as a critical focus area for businesses seeking to reduce their environmental footprint, particularly in relation to energy consumption and carbon emissions. With growing awareness and prioritization of sustainability, companies are setting ambitious goals, such as carbon neutrality and the use of 100% renewable energy. Data centers, as significant energy consumers, play a pivotal role in helping organizations meet these objectives.

- For instance, in August 2023, Bitcoin mining company Genesis Digital Assets expanded into South Carolina with new eco-friendly data centers. This trend reflects the increasing alignment of data centers with corporate sustainability strategies and the importance of environmental considerations in business operations.

What challenges does US Data Center Construction Market face during the growth?

- Cybersecurity issues associated with data centers is a key challenge affecting the market growth. Data centers play a crucial role in supporting online services and businesses by storing vast amounts of valuable information. However, they face significant threats from cyber-attacks, which can compromise the security, integrity, and availability of critical infrastructure and sensitive data. Two common types of cyber-attacks on data centers are distributed denial-of-service (DDoS) attacks and data breaches. DDoS attacks involve overwhelming a data center's network infrastructure with a massive volume of traffic, making it inaccessible to legitimate users. This disrupts service availability and can result in downtime and financial losses for businesses relying on the affected data center.

- Data breaches, on the other hand, involve unauthorized access to confidential or sensitive information stored within data center environments. Both types of attacks can cause significant damage to businesses and require robust security measures to prevent them. Data centers must prioritize cybersecurity to protect against these threats and ensure the confidentiality, integrity, and availability of critical data. Implementing advanced security technologies, such as firewalls, intrusion detection systems, and encryption, can help mitigate the risks of cyber-attacks. Regularly updating software and patches, conducting security audits, and educating employees on security best practices are also essential steps in securing data centers against cyber threats.

How can Technavio assist you in making critical decisions?

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- AECOM

- AMETEK Inc.

- Delta Electronics Inc.

- DPR Construction

- Eaton Corp.

- Emerson Electric Co.

- FORTIS CONSTRUCTION Inc.

- Gilbane Inc.

- HDR Inc.

- Hensel Phelps

- HITT Contracting Inc.

- International Business Machines Corp.

- Iron Mountain Inc.

- J.E. Dunn Construction Co.

- Nippon Telegraph and Telephone Corp.

- SAS Institute Inc.

- Schneider Electric SE

- Siemens AG

- Turner Construction Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developmet in US Data Center Construction Market

- In May, 2025, Arizton reported that the U.S. data center construction market was valued at an estimated USD48.18 billion in 2024 and is projected to reach USD112.33 billion by 2030, growing at a CAGR of 15.15%. This significant growth is primarily driven by the increasing demand for artificial intelligence (AI) and hyperscale cloud services, with AI workloads contributing over 50% of the market's expansion in 2024.

- Throughout late 2024 and early 2025, Northern Virginia continued to solidify its position as the leading data center market in the U.S., with projections indicating over 9 GW of new capacity expected to be added between 2025 and 2030. Other key regions experiencing significant construction activity include Texas (Dallas, Austin, Houston), Georgia (Atlanta), and Arizona (Phoenix, Mesa), as developers seek locations with robust infrastructure and favorable business environments.

- In 2024 and continuing into 2025, there has been a notable acceleration in the adoption of advanced cooling technologies and sustainable practices in U.S. data center construction. This includes a growing shift towards liquid cooling solutions to manage the high heat loads from AI and high-performance computing (HPC) workloads, alongside an increased focus on utilizing renewable energy sources and constructing "green" data centers to reduce environmental impact.

Research Analyst Overview

The data center construction market continues to experience significant growth, driven by the increasing demand for IT and telecommunications infrastructure. This sector encompasses various components, including electrical infrastructure and UPS systems, as well as mechanical infrastructure and cooling systems. The expansion of cloud computing, artificial intelligence (AI), and big data applications has been a major catalyst for this growth. Hyperscale data centers, which are designed to support large-scale cloud services, are increasingly popular due to their ability to offer scalable solutions and OPEX savings. The supply chain for data center construction is complex, involving numerous stakeholders, from equipment manufacturers to construction firms and IT services providers.

Cloud adoption and the shift towards remote working environments have further complicated the supply chain, requiring real-time monitoring software and innovative designs to ensure optimal performance and data security. The IT and telecommunications sector, cloud sector, and retail sector are among the key industries driving demand for data center construction. Macroeconomic factors, such as a strong economy and stable political environment, have also contributed to the growth of this market. However, the data center construction market faces several challenges. Inflation rates and commodity prices can impact the general construction cost, while the skilled workforce required for construction and maintenance can be a limiting factor.

Data security and cyber threats are also major concerns for data center operators. Data breaches and cyber attacks can result in significant financial and reputational damage. Therefore, data centers must employ advanced security measures, such as AI algorithms and artificial intelligence accelerators, to protect against these threats. The healthcare sector is another area where data centers are playing an increasingly important role. Cloud-based healthcare solutions, digital health, and IoT in healthcare are driving demand for data center infrastructure. Remote monitoring, medical device integration, and electronic health records are just a few of the applications where data centers are being used to improve patient care and streamline operations.

Disaster recovery protocols are also a critical consideration for data center operators. Free cooling techniques, such as evaporative/adiabatic coolers, and modular power infrastructure are being used to minimize the impact of physical damage on data center operations. Innovative designs, such as district heating and edge data centers, are also gaining popularity in the data center construction market. Telecommunication providers and edge centres are collaborating to offer edge computing solutions, which enable real-time data processing and reduce latency. The data center construction market is experiencing significant growth, driven by the increasing demand for IT and telecommunications infrastructure.

The market is complex, with numerous stakeholders and challenges, but also offers opportunities for technological innovation and cost savings. Data security and cyber threats are major concerns, but can be addressed through advanced security measures and innovative designs. The healthcare sector is a key area where data centers are playing an increasingly important role, and the market is expected to continue growing in the coming years.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.8% |

|

Market growth 2025-2029 |

USD 15.02 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.5 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -