Water Purifiers Market Size 2024-2028

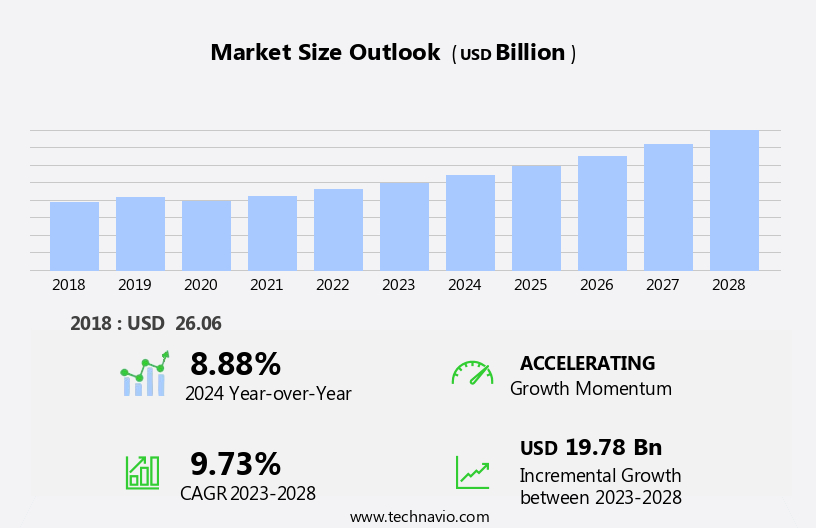

The water purifiers market size is forecast to increase by USD 19.78 billion at a CAGR of 9.73% between 2023 and 2028.

- The market is driven by the rising incidence of waterborne diseases, which underscores the growing need for clean and safe drinking water. According to the World Health Organization, diarrheal diseases caused by contaminated water kill an estimated 502,000 children under five years old each year. This alarming statistic highlights the urgent demand for water purification solutions. Another key driver is the continuous launch of innovative water purifiers, with companies introducing advanced technologies such as reverse osmosis, UV filtration, and ion exchange to cater to consumers' evolving preferences. However, the market faces challenges as well. The low replacement cycle of water purifiers, which is typically every three to five years, limits the growth potential for manufacturers.

- Additionally, the high initial investment required for purchasing water purifiers may deter some consumers from making a purchase, particularly in developing countries. Companies in the market must navigate these challenges by offering affordable financing options, extended warranties, and after-sales services to incentivize repeat purchases. To capitalize on opportunities, market players should also focus on expanding their product portfolios to cater to diverse consumer segments and geographies.

What will be the Size of the Water Purifiers Market during the forecast period?

- The market continues to evolve, driven by the persistent water quality issues and the increasing water crisis in urban areas. Pesticides and water pollution remain significant concerns, leading to the demand for advanced filtration technologies. One such innovation is the Elegant Black Edition RO water purifier, which effectively removes chlorine impurities, minerals, and dissolved solids. However, maintenance costs are a critical factor, with consumers seeking filter media that offer optimal energy levels and extended life. Smart water purifiers, equipped with smart sensors and UV filters, are gaining popularity in both residential and commercial sectors. These feature-rich purifiers enhance skin health and provide pure drinking water for daily activities, including cooking and bathing.

- Urbanization and increased population have led to a rapid development of the market, with emerging countries adopting water filtration systems to address waterborne diseases such as cryptosporidium and giardia. The market dynamics are further influenced by government programs, purchasing power, and consumer health concerns. End-users demand purifiers that decontaminate water from heavy metals, metabolites, and dangerous bacteria. Point-of-entry filters and gravity filters offer cost-effective solutions, while cloud ro and reverse osmosis systems cater to those seeking cutting-edge technology and advanced purification techniques. The market's continuous unfolding is shaped by various factors, including the evolving water crisis, consumer preferences, and technological advancements.The ongoing need for clean water in daily life, from cooking to bathing, ensures the market's dynamic nature will persist.

How is this Water Purifiers Industry segmented?

The water purifiers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Residential

- Commercial

- Technology

- Reverse osmosis (RO)

- Ultraviolet (UV)

- Ultrafiltration (UF)

- Gravity-based

- Others

- Distribution Channel

- Online Retail

- Offline Retail

- Direct Sales

- Product Type

- Countertop

- Wall-Mounted

- Under-Sink

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- Middle East and Africa

- UAE

- APAC

- Australia

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

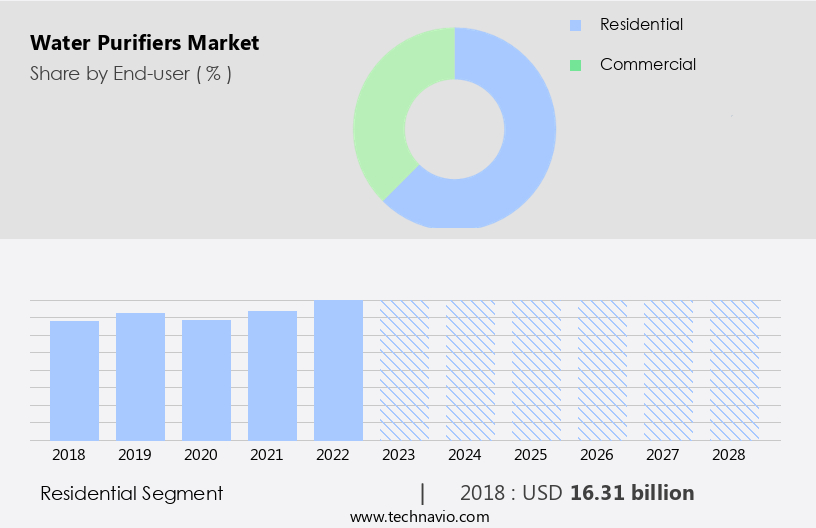

By End-user Insights

The residential segment is estimated to witness significant growth during the forecast period.

In today's world, ensuring access to clean and safe drinking water is a significant concern for both residential and commercial consumers. Waterborne diseases and contaminants, including pollutants, viruses, heavy metals, pesticides, and dissolved solids, have become a major health concern, especially in rapidly developing economies with high population densities, such as China and India. The increasing awareness of these issues has led to a surge in demand for water purifiers. Residential consumers, particularly those in urban areas, are investing in water purifiers to eliminate impurities and enhance their living standards. In India, for instance, the annual economic cost of waterborne diseases is estimated to be USD 600 million.

As a result, consumers are adopting residential water purifiers as a reliable source of pure drinking water. Moreover, the commercial sector is also recognizing the importance of clean water for daily activities, such as cooking and bathing. Commercial customers, including schools, hospitals, and offices, are installing water purifiers to provide clean water for their employees and clients. Water filtration technologies, such as Ultra-violet, Reverse Osmosis, and Gravity filters, have gained popularity due to their effectiveness in removing impurities. Smart water purifiers, equipped with smart sensors and a Cloud app, enable users to transmit findings, adjust settings, and notify them of maintenance needs.

Government programs and initiatives aimed at improving water quality and infrastructure are also driving the market for water purifiers. For example, Point-of-Entry filters are being installed in public buildings and housing complexes to ensure clean water at the water entry point. Urbanization and the resulting challenges in water infrastructure, such as aging pipes and pollution, have further boosted the demand for water purifiers. The maintenance cycle and costs of these devices are also becoming more affordable, making them accessible to a broader consumer base. In conclusion, the market for water purifiers is expected to grow significantly during the forecast period due to increasing health concerns, urbanization, and the need for clean water in daily activities.

Water filtration technologies, smart purifiers, and Point-of-Use filters are expected to be the key product types driving the market. The adoption of cutting-edge technology, such as UV filters and RO water purifiers, is also expected to enhance the overall market growth.

The Residential segment was valued at USD 16.31 billion in 2018 and showed a gradual increase during the forecast period.

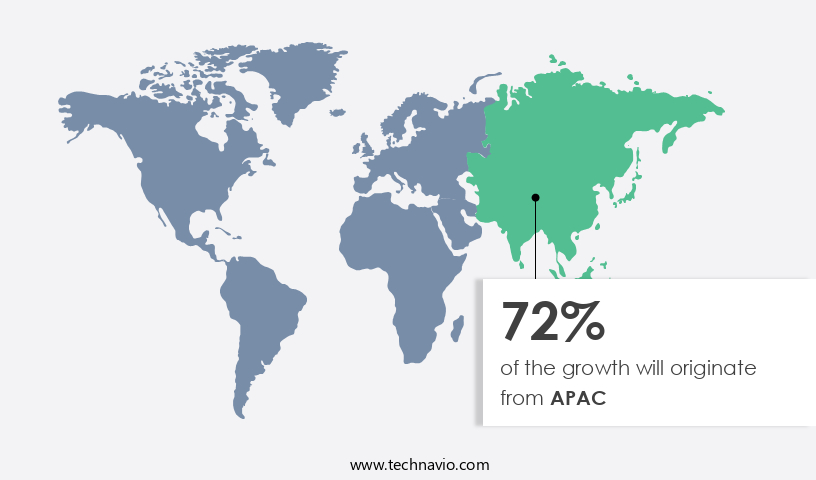

Regional Analysis

APAC is estimated to contribute 72% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in Asia Pacific is projected to expand substantially during the forecast period, driven by the heightened health concerns and increasing living standards in the region. China and India, with their large populations, account for a significant portion of the demand. Waterborne diseases, such as those caused by pollutants like pesticides, heavy metals, and harmful bacteria like Cryptosporidium and Giardia, are prevalent in many parts of Asia Pacific. According to estimates, over 35-37 million Indians fall ill from waterborne diseases each year, and approximately 1-2 million children die from diarrhea. As purchasing power increases in emerging economies like India, the demand for water purifiers has surged.

Water filtration technologies, including Ultra-violet (UV) and Reverse Osmosis (RO), have gained popularity due to their ability to remove dissolved solids, chlorine impurities, and microorganisms like viruses and bacteria. Commercial customers, particularly in the commercial sector, are increasingly investing in water purifying systems to ensure clean water for daily activities like cooking and bathing. Smart water purifiers, equipped with features like smart sensors and cloud apps, allow users to transmit findings, adjust settings, and notify them when maintenance is due. Government programs and initiatives aimed at improving water quality and addressing water crises have also contributed to the market's growth.

Point-of-entry filters, which treat water at the main water entry point, and Point-of-use filters, which treat water at the point of use, are popular options for both residential and commercial customers. Gravity filters and RO filters are commonly used filtration techniques. The market for water purifiers is rapidly developing, with companies like Pentair PLC offering feature-rich, elegant Black Edition RO water purifiers and UV water purifiers for pure drinking water. The market's growth is further fueled by the increasing urbanization and the need for clean water in urban areas. Water recycling and decontamination technologies are also gaining traction as potential solutions to address water scarcity and pollution issues.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Water Purifiers Industry?

- The escalating prevalence of waterborne diseases serves as the primary catalyst for market growth in this sector.

- Access to clean and safe drinking water is a pressing concern as urbanization increases and contaminated sources harbor pathogens, leading to waterborne diseases. The Centers for Disease Control and Prevention (CDC) reports that 17 waterborne pathogens are responsible for 7.2 million cases, 120,000 hospitalizations, and 6,600 deaths, as well as USD3 billion in healthcare costs annually in the US. Globally, the World Health Organization (WHO) estimates that microbiologically contaminated water causes approximately 505,000 diarrheic deaths each year. UV water purifiers and reverse osmosis (RO) filters are effective purification techniques for addressing health concerns.

- UV water purifiers eliminate dangerous bacteria, such as Giardia and cryptosporidium, while RO filters remove heavy metals and chlorine. In the residential sector, point-of-use filters notify users when it's time for replacement, ensuring clean water for daily activities. In emerging countries, these filters offer a solution to waterborne disease risks, enhancing overall health and wellbeing.

What are the market trends shaping the Water Purifiers Industry?

- The market trend mandates the continuous launch of innovative water purifiers. Two-line response: 1. Water purifier manufacturers are expected to persistently introduce new and advanced products to cater to the evolving consumer demands. 2. This trend signifies the growing importance of ensuring access to clean and safe water through technological advancements.

- The market is experiencing significant growth due to technological innovations and increasing consumer awareness of the importance of clean water. Advanced filtration technologies, such as Ultra-violet (UV) and activated carbon filters, effectively remove pollutants like dissolved solids, viruses, and bacteria. Smart water purifiers with features like smart sensors and adjustable settings cater to diverse consumer needs and preferences. Commercial sector growth, driven by government programs and commercial customers, is also contributing to market expansion. The focus on energy efficiency, customization, and eco-friendly designs aligns with modern living standards.

- Recent product launches, like Panasonic's latest water purifiers, showcase these advancements, offering increased tap water purification capacity and user-friendly designs. The market is expected to continue growing during the forecast period, driven by these trends and consumer demand.

What challenges does the Water Purifiers Industry face during its growth?

- The low replacement cycle of water purifiers poses a significant challenge to the industry's growth by requiring frequent replacements and increasing operational costs.

- Water purifiers have become essential appliances in both residential and commercial settings due to growing concerns over water quality. The water crisis, caused by pesticides, water pollution, and other impurities, has led to an increased demand for water filtration systems. The market for water purifiers is driven by the need to protect against waterborne diseases, reduce weight, and ensure optimal energy levels. High-quality RO water purifiers effectively remove Chlorine impurities and minerals, providing clean drinking water. However, the market growth may be hindered by the low replacement cycle of water purifiers. The long lifespan of these appliances, coupled with minimal maintenance costs, results in extended purchase intervals.

- This reduces the frequency of new sales and slows down market expansion. Despite this challenge, manufacturers continue to innovate, introducing elegant designs like the Black Edition, to cater to consumer preferences. Filter media, such as activated carbon and UV technology, are used to remove metabolites and Cryptosporidium, ensuring water remains safe for consumption. As population growth continues, the demand for water purifiers is expected to increase, providing opportunities for market expansion.

Exclusive Customer Landscape

The water purifiers market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the water purifiers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, water purifiers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - This company introduces advanced water purification solutions, including the 3M smart drinking water purifier. Employing impact technology, this device effectively eliminates bacteria without water waste. By prioritizing efficiency and sustainability, it sets a new standard in water purification.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- A. O. Smith Corp.

- Advent International Corp.

- AQUA RO WATER SOLUTIONS

- AquaSafe Water Solutions

- Aquatec Plus

- Axel Johnson Inc

- Blue Star Ltd.

- BRITA SE

- Culligan International Co.

- General Electric Co.

- Havells India Ltd.

- Helen of Troy Ltd.

- Honeywell International Inc.

- ispring water system LLC

- KENT RO Systems Ltd.

- LG Electronics Inc.

- Panasonic Holdings Corp.

- Tata Sons Pvt. Ltd.

- Unilever PLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Water Purifiers Market

- In February 2024, Bluewater, a leading water purification technology company, introduced the new "Bluewater Pro" series, integrating advanced UV-C technology to eliminate bacteria and viruses, marking a significant advancement in residential water purification systems (Bluewater Press Release, 2024).

- In August 2025, Veolia Water Technologies, a global water solutions provider, announced a strategic partnership with Microsoft to develop intelligent water management systems, leveraging Microsoft's Azure IoT and AI technologies, aiming to optimize water treatment processes and improve operational efficiency (Veolia Water Technologies Press Release, 2025).

- In November 2024, Evoqua Water Technologies completed the acquisition of GE Water & Process Technologies, significantly expanding its portfolio and strengthening its position as a global leader in water and wastewater treatment solutions (Evoqua Water Technologies Press Release, 2024).

- In March 2025, the Indian government launched the "Jal Shakti Abhiyan: Catch the Rain" campaign, focusing on rainwater harvesting and water conservation, creating new opportunities for water purification companies to expand their presence in the Indian market (Ministry of Jal Shakti Press Release, 2025).

Research Analyst Overview

In the dynamic the market, maintenance cycles for flagship products are gaining importance as emerging economies rapidly develop and notify users of potential filter replacements. Reverse osmosis filtration, a cutting-edge technology, is increasingly preferred due to its effectiveness against waterborne diseases. Smart purifiers, with cloud apps and adjustable settings, cater to the growing demand for easy-to-use, feature-rich solutions. Increased population and living standards drive market development potential.

Government programs aiming to provide clean water further fuel the demand. Smart sensors ensure efficient operation and enhance user experience. With purchasing power on the rise, this sector presents significant opportunities for businesses.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Water Purifiers Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

179 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.73% |

|

Market growth 2024-2028 |

USD 19.78 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.88 |

|

Key countries |

US, China, Germany, Japan, UK, Australia, India, France, Brazil, Canada, Brazil, UAE, Australia, Rest of World (ROW), and Saudi Arabia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Water Purifiers Market Research and Growth Report?

- CAGR of the Water Purifiers industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the water purifiers market growth of industry companies

We can help! Our analysts can customize this water purifiers market research report to meet your requirements.

RIA -

RIA -