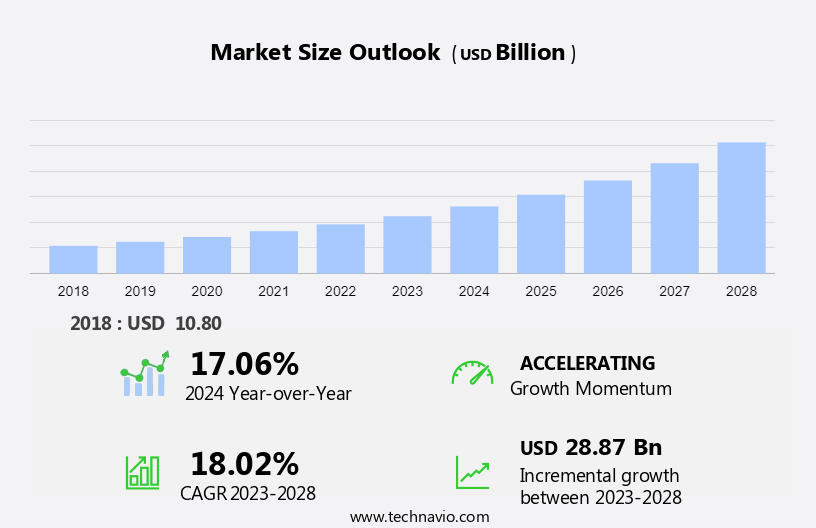

Wireless Sensors Market Size 2024-2028

The wireless sensors market size is forecast to increase by USD 28.87 billion at a CAGR of 18.02% between 2023 and 2028. The market is experiencing significant growth, driven by the increasing adoption of Industry 4.0 and the Internet of Things (IoT) in various industries. The integration of wireless sensors in manufacturing processes enables real-time monitoring, predictive maintenance, and improved efficiency, making it a crucial component of Industry 4.0. Additionally, emerging wearable technologies are fueling the demand for wireless sensors in healthcare, fitness, and wellness applications. Moreover, technological advancements in telemedicine and telehealth platforms enable continuous monitoring of hypopnea-related events, respiratory rate, and snoring in patients with sleep apnea using wireless devices like smartwatches and smartphones. However, delivering high-quality wireless sensor networks at low costs remains a significant challenge. The market trends include the development of long-range, low-power wireless technologies, the integration of advanced analytics and machine learning algorithms, and the increasing use of cloud-based platforms for data processing and storage.

The market is witnessing significant growth due to the increasing adoption of IoT technology and the proliferation of connected devices. These sensors, which include battery-operated motes and sensor nodes, use wireless networks to transmit data. They find applications in various sectors such as Industrial automation, Smart grids, Smart homes, and Smart cities. Zero-power wireless sensors are gaining popularity due to their extended battery life and low power consumption. The market is also driven by the growing demand for data monitoring in various industries, including Energy sources and Renewable energy. Wireless sensors are used in RFID and Bluetooth applications for data monitoring and remote monitoring.

Furthermore, the market for wireless sensors is vast and diverse, with applications ranging from PC peripherals and remote controls to Self-driving cars and Electric cars. The market is expected to grow at a rapid pace in the coming years, driven by the increasing demand for wireless sensors in IoT applications, Smart homes, and Smart cities. Wireless sensors are used in various industries, including Industrial automation, Smart grids, and Building automation, to monitor and control various processes. They are also used in Hydraulic brakes and connected devices for data monitoring and remote monitoring. The market for wireless sensors in the automotive industry is expected to grow rapidly due to the increasing demand for safety and efficiency in electric cars and Self-driving cars.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Building automation

- Wearable devices

- Healthcare

- Automotive and transportation

- Others

- Component

- Hardware

- Software

- Services

- Geography

- North America

- US

- APAC

- China

- Japan

- Europe

- Germany

- UK

- South America

- Middle East and Africa

- North America

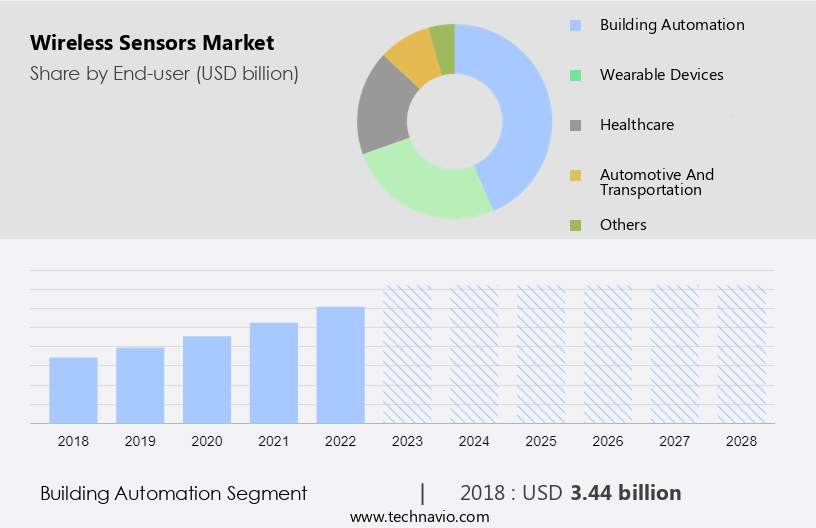

By End-user Insights

The building automation segment is estimated to witness significant growth during the forecast period. Wireless sensors play a pivotal role in various industries, including workforce safety in mining and oil & gas, energy transmission, and facility management. In the energy sector, these sensors enable condition monitoring of machinery and equipment, reducing carbon footprint and enhancing energy efficiency. Wireless sensors are deployed in stationary weather conditions for energy processing and in portable weather conditions for wind energy systems, weather stations, and building design aerodynamics. Vicotee, a Norwegian startup, and Everactive are among the wireless sensor manufacturers providing battery-free wireless sensors for applications such as cold chain refrigerator monitoring, asset tracking, and smart agriculture. Vicotee Cloud offers IoT solutions for smokestack mercury sampling, automotive emissions, and water pollution devices.

Moreover, the collaborations have led to advancements in low-power management and wired electrical infrastructure. In the context of building automation systems (BASs), wireless sensors are essential for monitoring and controlling heating, ventilation, and air conditioning (HVAC), managing facilities (lighting, security, and access), and automating electric meter readings. Companies like Honeywell International Inc. And Philips Hue (Koninklijke Philips N.V.) provide wireless thermostats and sensors for precise HVAC system monitoring and optimization. Motion sensors from Philips Hue and Lutron (Lutron Electronics Co.) enable real-time HVAC and lighting adjustments, ensuring energy conservation and enhancing overall efficiency.

Get a glance at the market share of various segments Request Free Sample

The building automation segment was valued at USD 3.44 billion in 2018 and showed a gradual increase during the forecast period.

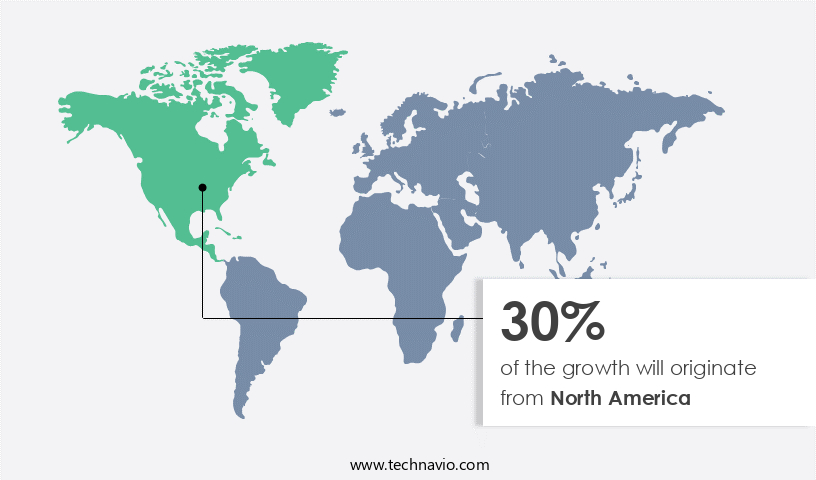

Regional Insights

North America is estimated to contribute 30% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In the market, North America led with a significant share in 2023, primarily driven by the US, which is a major manufacturing hub with a strong presence in industries such as energy transmission, mining, oil & gas, and manufacturing. The region's focus on Industrial Internet of Things (IoT) adoption has resulted in the integration of wireless sensor technologies in various sectors like healthcare, agriculture, and smart cities for enhanced efficiency and data-driven decision-making. The US, in particular, is known for its advancements in IoT, making it a significant contributor to the market's growth. Wireless sensors play a crucial role in various industries, including energy processing, where they are used for condition monitoring and low power management in wind energy systems, weather stations, and building design aerodynamics.

Furthermore, in the energy sector, these sensors help minimize carbon footprint and optimize energy usage. In the manufacturing sector, they are used for machinery and equipment monitoring, asset tracking, and smart agriculture. Key wireless sensor manufacturers are leading the market with innovative solutions. Everactive's battery-free wireless sensors and Vicotee's Cloud-based monitoring system are notable examples. These solutions are being implemented in diverse applications, such as cold chain refrigerator monitoring, smokestack mercury sampling, and smart waste management. The Caribbean region is also witnessing growth in the market, with applications in weather conditions monitoring for hurricane warnings and asset tracking for logistics management.

Overall, the market is expected to continue its growth trajectory, driven by the increasing demand for real-time data and automation in various industries.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Increasing adoption of Industry 4.0 is the key driver of the market. The market is experiencing significant growth due to the implementation of Industry 4.0, which integrates digital technologies into manufacturing processes. This revolution aims to create smart factories where machines, systems, and processes collaborate in real-time, leading to increased efficiency, productivity, and data-driven decision-making. NOVELDA's wireless sensors play a pivotal role in this transformation, offering connectivity and real-time data for smart manufacturing.

Furthermore, these sensors are utilized extensively throughout the manufacturing process to monitor and collect data on various parameters such as temperature, humidity, pressure, and equipment status. By enabling predictive maintenance, optimizing energy usage, increasing overall equipment efficiency (OEE), and facilitating quick responses to production changes, wireless sensors contribute significantly to the smart factory concept. The power-saving mechanism integrated into these sensors further enhances their appeal, ensuring extended battery life and reduced maintenance costs.

Market Trends

Emerging wearable technologies is the upcoming trend in the market. The market is witnessing significant growth due to the increasing popularity of wearable devices that enhance people's daily lives worldwide. These devices, which include smartwatches, Google Glass-like smart glasses, smart fabrics, heart rate monitors, and fitness trackers are essentially mobile communication technologies that can be attached to a body part.

Furthermore, magnetic sensor manufacturers are innovating by developing micro-electromechanical systems (MEMS) sensors to support these wearable technologies. In the medical field, the adoption of novel sensors has led to advancements in disease detection, such as breast cancer.

Market Challenge

The growing challenge of delivering high-quality wireless sensor networks at low cost is a key challenge affecting the market growth. The market encounters hurdles in providing top-tier networks at economical prices, thereby impeding their extensive utilization. One of the major obstacles is the expense of manufacturing elements for sophisticated wireless sensors, including accurate sensors, reliable communication modules, and power-efficient processors, which influences the affordability of implementing sensor networks.

Furthermore, another challenge lies in achieving a fine equilibrium between energy conservation and strong functionality, as numerous wireless sensors operate on battery power, necessitating prolonged battery life for applications in secluded or inaccessible environments. Furthermore, security becomes a paramount concern as wireless sensor networks expand, necessitating strong security measures to safeguard data transmission without incurring excessive costs, which market participants are continually addressing through innovative solutions.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Analog Devices Inc.: The company offers wireless sensor solutions that consist of spatially distributed autonomous sensors to monitor physical or environmental conditions, such as temperature, sound, vibration, pressure, humidity, motion, or pollutants.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- ADT Inc.

- Advantech Co. Ltd.

- Emerson Electric Co.

- General Electric Co.

- Honeywell International Inc.

- Infineon Technologies AG

- Koninklijke Philips N.V.

- Laird Connectivity

- Legrand SA

- Libelium Comunicaciones Distribuidas SL

- Lutron Electronics Co. Inc.

- Microchip Technology Inc.

- NXP Semiconductors NV

- Renesas Electronics Corp.

- Robert Bosch GmbH

- Schneider Electric SE

- Sensata Technologies Inc.

- Siemens AG

- Somfy SA

- STMicroelectronics International NV

- TE Connectivity Ltd.

- Texas Instruments Inc.

- Yokogawa Electric Corp.

- Broadcom Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Wireless sensors have revolutionized various industries by enabling real-time data monitoring and management. These sensors, which include battery-operated motes and sensor nodes, communicate wirelessly through networks such as Bluetooth, Wireless Fidelity (Wi-Fi), Cellular Network, and RFID. The IoT era has significantly increased the demand for wireless sensors in sectors like smart transportation, military surveillance, machine monitoring, patient monitoring, smart grids, industrial automation, smart homes, smart cities, and more. Hardware components play a crucial role in the functionality and efficiency of wireless sensors. Technologies like MEMS sensors, LED sensors, flow sensors, and RFID are integral to specific applications.

Furthermore, zero-power wireless sensors are gaining popularity due to their energy efficiency, with applications in various sectors like renewable energy, building automation, and power lines. The integration of wireless sensors in electric cars and self-driving cars is another significant development, enhancing safety and performance. Wireless sensors are transforming industries, from manufacturing and healthcare to transportation and energy, by providing data monitoring capabilities for connected devices, transformers, power lines, and IoT-connected devices. The future of wireless sensors looks promising, with advancements in technology and increasing demand for smart solutions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

177 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 18.02% |

|

Market growth 2024-2028 |

USD 28.87 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

17.06 |

|

Regional analysis |

North America, APAC, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

North America at 30% |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ABB Ltd., ADT Inc., Advantech Co. Ltd., Analog Devices Inc., Emerson Electric Co., General Electric Co., Honeywell International Inc., Infineon Technologies AG, Koninklijke Philips N.V., Laird Connectivity, Legrand SA, Libelium Comunicaciones Distribuidas SL, Lutron Electronics Co. Inc., Microchip Technology Inc., NXP Semiconductors NV, Renesas Electronics Corp., Robert Bosch GmbH, Schneider Electric SE, Sensata Technologies Inc., Siemens AG, Somfy SA, STMicroelectronics International NV, TE Connectivity Ltd., Texas Instruments Inc., Yokogawa Electric Corp., and Broadcom Inc. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -