Workflow Management Systems Market Size 2024-2028

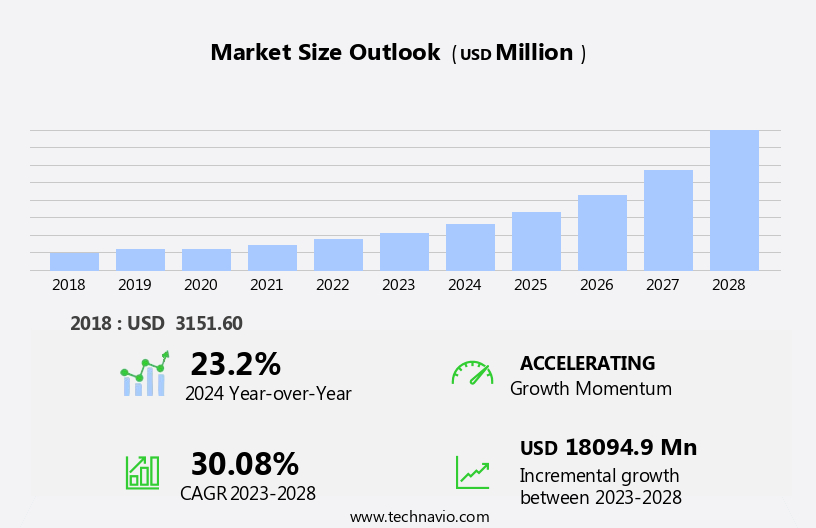

The workflow management systems market size is forecast to increase by USD 18.09 billion at a CAGR of 30.08% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing demand for process automation and digital transformation. Companies are seeking efficient and streamlined methods to manage their business processes, leading to the emergence of these systems. Another trend In the market is the development of mobile solutions, which offer flexibility and convenience for users. However, data security and privacy concerns remain a challenge In the market, as organizations must ensure the protection of sensitive information. As businesses continue to digitalize their operations, the market is expected to grow steadily. The implementation of these systems can lead to increased productivity, improved compliance, and enhanced customer experience. Overall, the market presents numerous opportunities for companies, particularly those offering innovative solutions that address the evolving needs of businesses.

What will be the Size of the Workflow Management Systems Market During the Forecast Period?

- The market is experiencing significant growth due to the increasing adoption of cutting-edge technologies in corporate processes. Industry verticals across the globe are recognizing the value of streamlined business processes, leading to increased demand. Cloud computing and mobile computing have enabled the deployment of cloud-based systems, offering cost efficiency, resources savings, scalability, and flexibility. The software segment of the market is witnessing strong growth, driven by the cost advantages and productivity gains offered by these systems.

- Moreover, cloud technology is revolutionizing business applications, allowing workloads to be processed more efficiently and effectively. Technology start-ups and established players alike are investing in these systems, with the IT, telecom, ERP, and CRM segments being major contributors. The market is expected to continue its growth trajectory, driven by the ongoing digitization of business processes and the increasing adoption of cloud services.

How is this Workflow Management Systems Industry segmented and which is the largest segment?

The workflow management systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Deployment

- On premise

- Cloud

- End-user

- BFSI

- Government

- Healthcare

- Legal

- Education and others

- Geography

- North America

- US

- Europe

- Germany

- APAC

- China

- India

- Japan

- South America

- Middle East and Africa

- North America

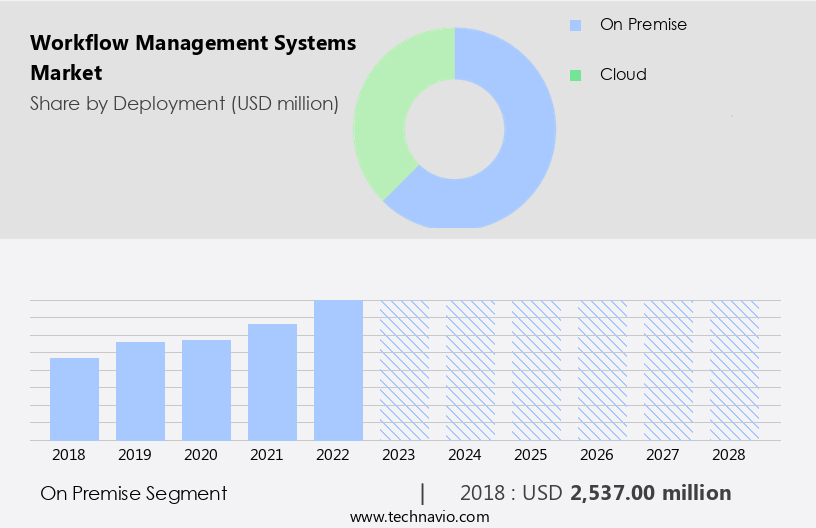

By Deployment Insights

- The on premise segment is estimated to witness significant growth during the forecast period.

Large enterprises with a global presence are the primary drivers, particularly for on-premises solutions. The need for control and ownership over operations, processes, and data is a significant factor In their preference for on-premises WMS. On-premises deployment offers several advantages, including control over IT infrastructure, enhanced data security, and a better understanding of data security needs. This deployment model allows organizations to access their data directly and maintain complete oversight of their systems. The benefits of on-premises WMS extend to various industry verticals, including marketing, supply chain, inventory management, HR, production workflows, and more. Cloud-based systems are also gaining popularity due to their scalability, flexibility, and cost advantages. Cloud technology enables businesses to access workflow applications from anywhere, making it ideal for remote teams and organizations undergoing digital transformation. The WMS market is expected to grow significantly during the forecast period due to the increasing demand for automation, ease of deployment, and integration with other business applications such as HR systems, reporting systems, and CRM.

Additionally, cloud-based solutions offer cost savings, as they eliminate the need for organizations to invest in IT infrastructure and IT support. The software segment is expected to dominate the market due to its flexibility and ability to integrate with various business processes. The consulting and integration segments are also expected to grow rapidly due to the increasing need for expertise in implementing and integrating these solutions. The market is expected to be driven by the manufacturing sector, followed by IT, telecom, and technology start-ups. The implementation cost and digital transformation initiatives are key factors influencing the adoption of WMS.

Get a glance at the Workflow Management Systems Industry report of share of various segments Request Free Sample

The on premise segment was valued at USD 2.54 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

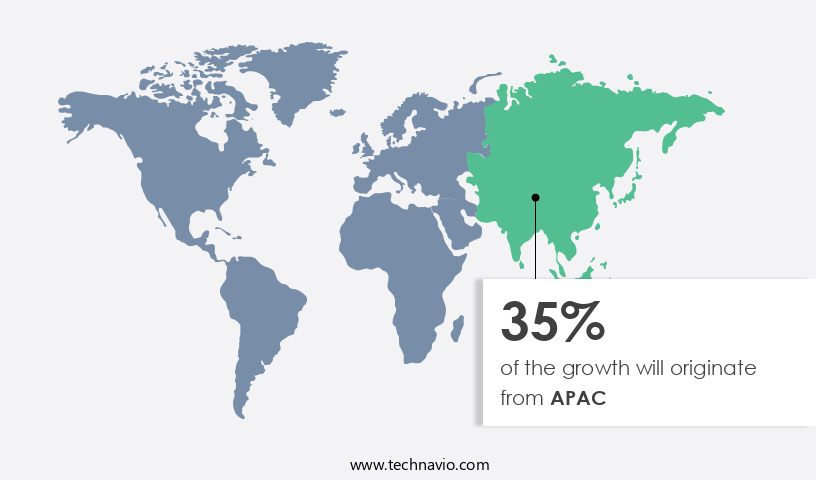

- APAC is estimated to contribute 35% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market is experiencing growth due to the increasing modernization of business processes and the integration of advanced technologies in various industries, such as BFSI, government, healthcare, and legal sectors. Organizations in North America are prioritizing automation solutions to analyze vast amounts of data in real-time, enhancing workflow efficiency and optimizing decision-making processes. The proliferation of data across industries is fueling the demand for WMS solutions and other advanced technologies, such as analytics, to streamline operations.

Moreover, cloud computing, mobile computing, and cloud-based systems are key trends driving the market's growth. These systems offer cost advantages, scalability, flexibility, and ease of deployment, making them attractive to departments such as marketing, supply chain, inventory management, HR, production workflows, and more. The market is segmented into software, service, cloud, on-premise, IT, telecom, and others, with the software segment leading the market due to its productivity benefits. The forecast period is expected to see continued growth as businesses in manufacturing and other sectors embrace digital transformation and seek to improve agility, transparency, and customer satisfaction through WMS solutions.

Market Dynamics

Our workflow management systems market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Workflow Management Systems Industry?

Increasing demand for process automation and digital transformation is the key driver of the market.

- Workflow Management Systems (WMS) have gained significant traction In the corporate world as businesses seek to automate and streamline their processes for increased efficiency, accuracy, and cost savings. The market for WMS is driven by the adoption of cutting-edge technologies such as cloud computing and mobile computing, which enable cloud-based systems and mobile devices for information sharing. The software segment of the WMS market is expected to dominate the industry during the forecast period due to its productivity advantages and ease of deployment. The service segment is also expected to grow at a steady pace as organizations require integration and consulting services to implement and optimize their workflow solutions. Industry verticals such as marketing, supply chain, inventory management, HR, production workflow, and IT departments are adopting WMS to improve agility, transparency, and customer satisfaction. Cloud technology has been a major catalyst for the growth of WMS, offering scalability, flexibility, and cost advantages over traditional on-premise systems. Large organizations across sectors such as manufacturing, telecom, and IT are investing in WMS to digitally transform their operations, reduce lead times, minimize errors, and enhance collaboration and decision-making capabilities.

- Moreover, cloud-based systems, cloud services, and HRM systems are becoming essential business applications for teams working remotely or in different locations. The integration segment of the WMS market is also expected to grow rapidly as organizations seek to connect their IT assets and streamline their workloads across different systems and applications. IT support and infrastructure are critical components of WMS implementation, requiring technical expertise and funding for successful deployment. In summary, the WMS market is poised for growth as businesses continue to seek ways to automate their workflows, improve operational efficiency, and enhance customer experiences. The market demand for WMS is expected to remain strong during the forecast period as organizations embrace digital solutions to meet evolving customer demands and stay competitive.

What are the market trends shaping the Workflow Management Systems Industry?

The emergence of mobile WMS solutions is the upcoming market trend.

- Workflow Management Systems (WMS) have gained significant traction in corporate processes due to the integration of cutting-edge technologies, enabling businesses to streamline their operations and enhance productivity. The industry verticals that have adopted systems include marketing, supply chain, inventory management, HR, production workflows, and more. The shift towards cloud computing and mobile computing has led to the popularity of systems, offering scalability, flexibility, and cost advantages. Cloud technology and business applications have revolutionized workloads, allowing for automation and ease of deployment. These systems offer decision-making capabilities, reporting systems, and webbased workflow, enabling teams to work remotely and collaborate in real-time. The integration segment and consulting segment of the WMS market are expected to grow at a steady pace during the forecast period. Large organizations have recognized the benefits of systems, including cost efficiency, resource optimization, and high-quality work. The adoption of these systems has led to increased agility, transparency, and customer satisfaction.

- Moreover, cloud-based servers and traditional software have become essential IT assets for businesses, with cloud services offering lead time reduction, error minimization, and IT support infrastructure creation. The implementation of workflow management systems requires careful planning and funding, with implementation costs varying depending on the size and complexity of the organization. Digital transformation has become a priority for businesses across sectors, with manufacturing, telecom, and technology start-ups leading the way. The market demand for workflow management systems is expected to continue growing, driven by the need for automation and the ease of integration with ERP, CRM, and other business applications. In summary, workflow management systems have become essential tools for businesses seeking to optimize their operations, increase productivity, and enhance customer satisfaction. The adoption of cloud-based and mobile workflow management systems has enabled teams to work remotely and collaborate in real-time, leading to increased agility and transparency. The future of workflow management systems lies In their ability to integrate with other business applications and provide real-time data-sharing capabilities, making them indispensable tools for businesses In the digital age.

What challenges does the Workflow Management Systems Industry face during its growth?

Data security and privacy issues is a key challenge affecting the industry growth.

- Workflow Management Systems (WMS) have become essential for businesses in various industry verticals, including finance, healthcare, retail, and manufacturing, to streamline corporate processes and enhance productivity. These systems leverage cutting-edge technologies like cloud computing and mobile computing to offer scalability, flexibility, and cost advantages. Cloud-based workflow management systems, in particular, enable organizations to access business applications and manage workloads from anywhere, anytime, using cloud technology. The software segment of the WMS market is expected to witness significant growth during the forecast period due to the ease of deployment and cost effectiveness of cloud-based solutions. Departments such as marketing, supply chain, inventory management, HR, and production workflow can benefit from these systems.

- However, concerns around security, such as malware, data theft, and hacking, could hinder the large-scale adoption of WMS solutions. The integration segment of the WMS market is also expected to grow as businesses look to integrate their IT assets, including ERP, CRM, and cloud services, with their workflow management systems. This can help reduce lead times, minimize errors, and improve customer satisfaction by enabling high-quality work, agility, transparency, and effective interactions between teams and departments. Despite these benefits, the implementation cost and digital transformation efforts required to adopt WMS solutions can be significant for large organizations. However, the potential cost savings and productivity gains make it a worthwhile investment for businesses looking to stay competitive in today's digital economy.

- Cloud-based servers and informationsharing technologies enable real-time collaboration and access to critical business data from mobile devices. This is particularly important for remote teams and organizations looking to streamline their operations and improve decision-making capabilities. In summary, the WMS market is expected to grow significantly In the coming years due to the increasing adoption of digital solutions and the need for automation and ease of deployment. The market demand for WMS solutions is driven by the need to improve business processes, reduce operational complexities, and enhance productivity across various industry sectors.

Exclusive Customer Landscape

The workflow management systems market forecasting report includes the adoption lifecycle of the market, market growth and forecasting, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the workflow management systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, workflow management systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry. The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Appian Corp.

- Automation Anywhere Inc.

- Bizagi Group Ltd.

- Dell Technologies Inc.

- Fortra LLC

- Fujitsu Ltd.

- HP Inc.

- International Business Machines Corp.

- monday.com Ltd.

- Newgen Software Technologies Ltd.

- Nintex Global Ltd.

- Oracle Corp.

- PairSoft

- Pegasystems Inc.

- Robert Bosch GmbH

- SAP SE

- Software AG

- Vista Equity Partners Management LLC

- Xerox Holdings Corp.

- Zoho Corp. Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Workflow management systems have become an essential component of corporate processes in various industry verticals, enabling organizations to streamline business operations and enhance productivity. These systems leverage cutting-edge technologies such as cloud computing and mobile computing to offer flexibility and scalability, making them indispensable for businesses looking to stay competitive. Cloud-based workflow management systems have gained significant traction in recent years due to their cost advantages and ease of deployment. These systems allow organizations to manage their workloads efficiently, ensuring high-quality work and reducing lead times. The cloud segment is expected to dominate the market during the forecast period, driven by the increasing adoption of digital solutions and remote work. The software segment is another significant contributor to the market. Productivity gains and cost efficiency are the primary drivers for businesses investing In these systems. Conventional workflows, which were often manual and time-consuming, have given way to automated processes that offer agility, transparency, and customer satisfaction. The service segment, including consulting and integration, is also expected to grow at a steady pace. Organizations require expertise and guidance to implement these systems effectively, making the services segment an essential part of the market. The IT department is a primary consumer of workflow management systems, with marketing, supply chain, inventory management, HR, production workflows, and IT support being some of the key areas of application.

Moreover, the manufacturing sector is a significant adopter of workflow management systems due to the need for efficient production processes and inventory management. The technology start-ups segment is also expected to contribute to the market growth, driven by their focus on innovation and digital transformation. Cloud technology plays a crucial role In the market, enabling organizations to access these systems from anywhere, at any time, using mobile devices. Information-sharing technologies have further enhanced the value proposition of these systems, allowing for seamless interactions between teams and departments. Large organizations, in particular, stand to benefit significantly from workflow management systems. These systems offer cost advantages, scalability, and the ability to manage complex workflows and IT assets effectively. Cloud-based servers and databases provide the necessary infrastructure for these systems, ensuring reliable and secure operations. The implementation cost of workflow management systems can be a significant barrier to adoption for some organizations. However, the benefits, including increased productivity, cost efficiency, and improved decision-making, often outweigh the initial investment. Funding options, such as IT budgets and external financing, can help organizations overcome this hurdle.

In summary, the market is driven by the need for cost efficiency, productivity gains, and digital transformation. Cloud computing and mobile computing have enabled the development of flexible and scalable solutions that cater to the evolving needs of businesses across various industry verticals. The market is expected to grow steadily during the forecast period, driven by the increasing adoption of digital solutions and the need for automation and integration.

|

Workflow Management Systems Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 30.08% |

|

Market growth 2024-2028 |

USD 18.09 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

23.2 |

|

Key countries |

US, Germany, Japan, China, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Workflow Management Systems Market Research and Growth Report?

- CAGR of the Workflow Management Systems industry during the forecast period

- Detailed information on factors that will drive the Workflow Management Systems growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the workflow management systems market growth of industry companies

We can help! Our analysts can customize this workflow management systems market research report to meet your requirements.

RIA -

RIA -